Answered step by step

Verified Expert Solution

Question

1 Approved Answer

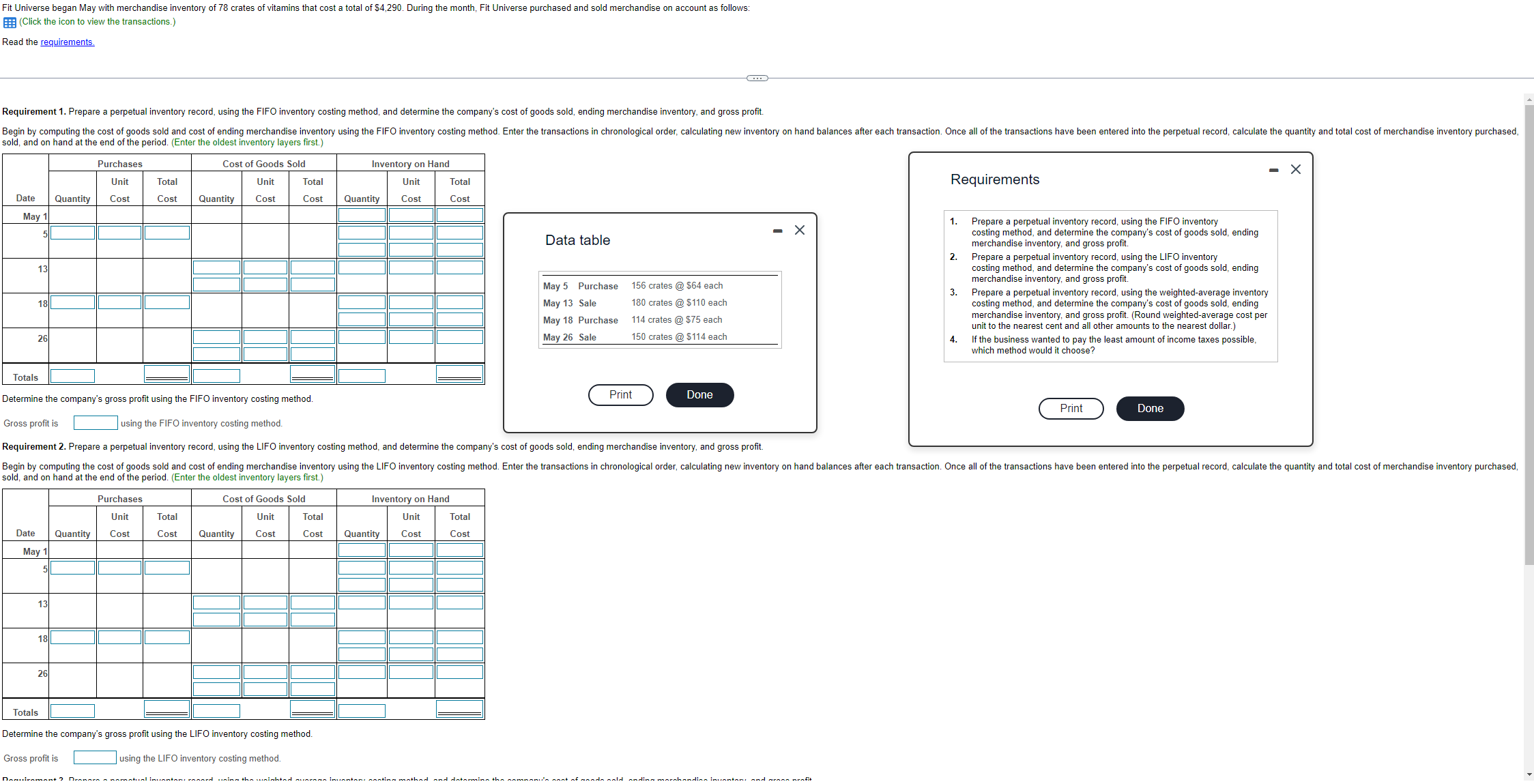

Question 6 11 Answer all the requirements please thank you E8 (Click the icon to view the transactions.) Read the requirements. sold, and on hand

Question 6 11

Answer all the requirements please thank you

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essentials Of Internal Auditing CIA Part 1 2021

Authors: Muhammad Zain

1st Edition

B09B36MRH2, 979-8542949130