Question

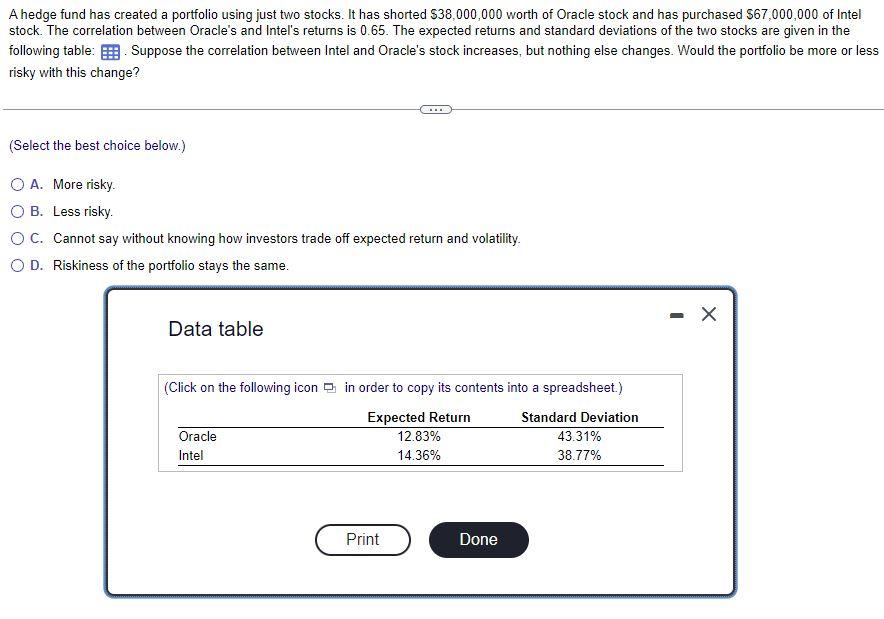

Question 6: A hedge fund has created a portfolio using just two stocks. It has shorted $38,000,000 worth of Oracle stock and has purchased $67,000,000

Question 6: A hedge fund has created a portfolio using just two stocks. It has shorted

$38,000,000

worth of Oracle stock and has purchased

$67,000,000

of Intel stock. The correlation between Oracle's and Intel's returns is

0.65.

The expected returns and standard deviations of the two stocks are given in the following table below.

Suppose the correlation between Intel and Oracle's stock increases, but nothing else changes. Would the portfolio be more or less risky with this change?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Futures And Options Markets

Authors: John C. Hull

4th Edition

0130176028, 9780130176028