Answered step by step

Verified Expert Solution

Question

1 Approved Answer

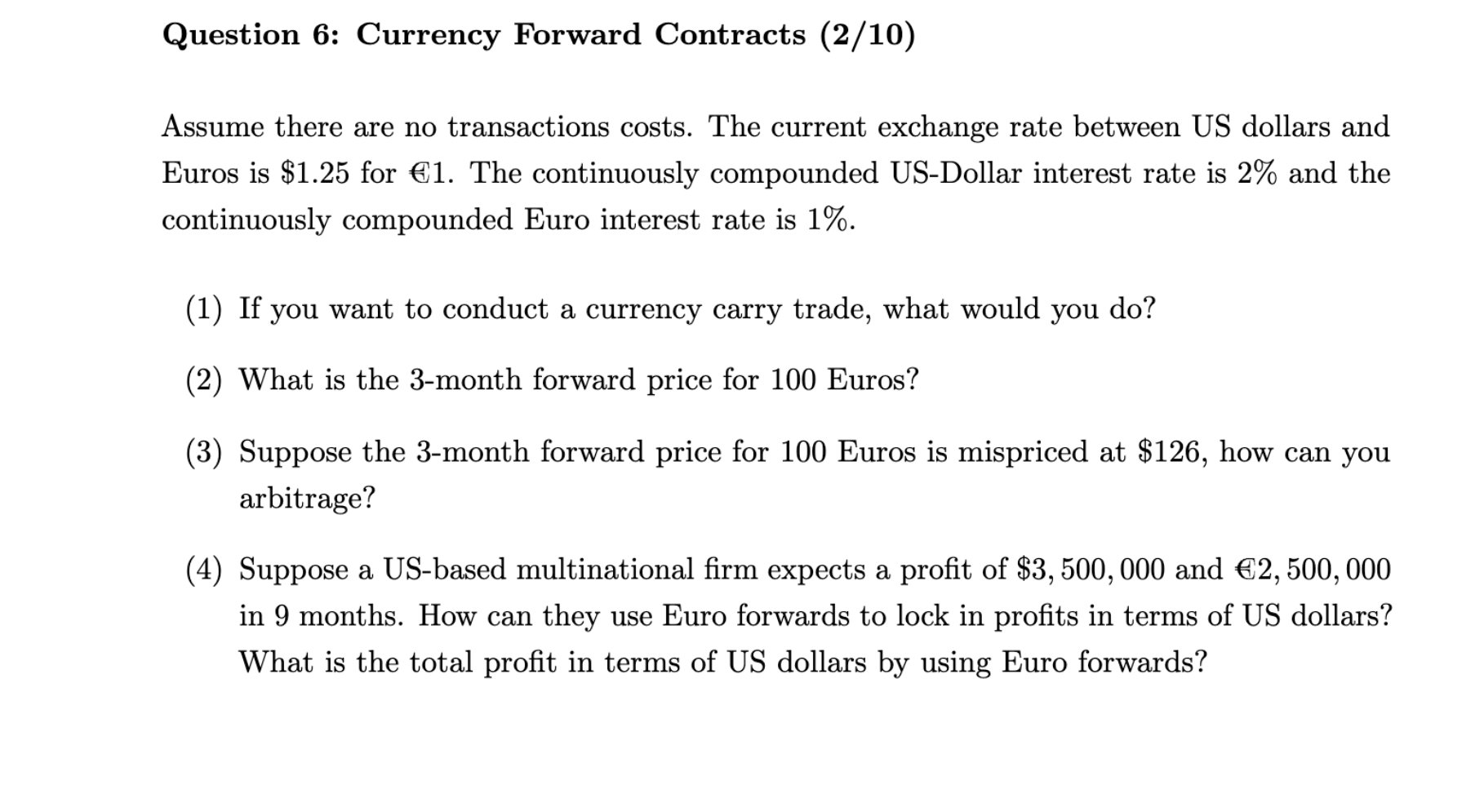

Question 6 : Currency Forward Contracts ( 2 / 1 0 ) Assume there are no transactions costs. The current exchange rate between US dollars

Question : Currency Forward Contracts

Assume there are no transactions costs. The current exchange rate between US dollars and

Euros is $ for The continuously compounded USDollar interest rate is and the

continuously compounded Euro interest rate is

If you want to conduct a currency carry trade, what would you do

What is the month forward price for Euros?

Suppose the month forward price for Euros is mispriced at $ how can you

arbitrage?

Suppose a USbased multinational firm expects a profit of $ and

in months. How can they use Euro forwards to lock in profits in terms of US dollars?

What is the total profit in terms of US dollars by using Euro forwards?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essentials Of Corporate Finance

Authors: Stephen A. Ross, Randolph W. Westerfield, Bradford D. Jordan

9th International Edition

1259254801, 9781259254802