Answered step by step

Verified Expert Solution

Question

1 Approved Answer

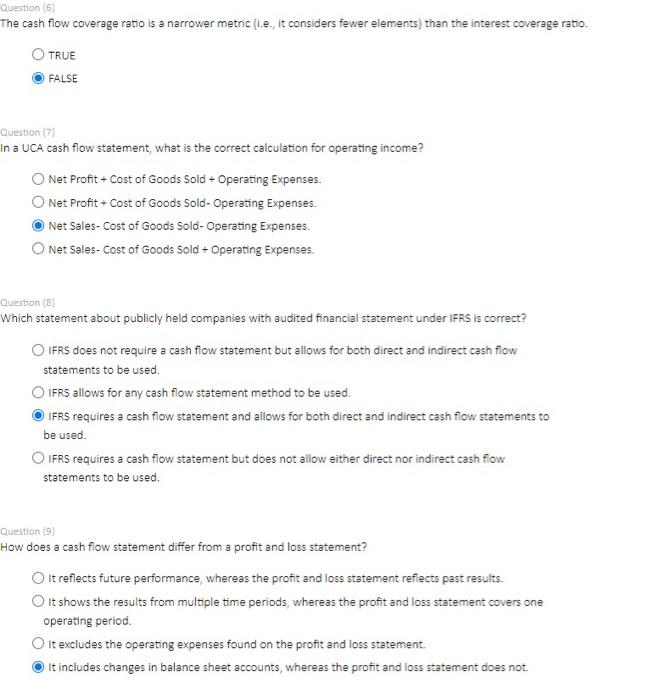

Question (6) The cash flow coverage ratio is a narrower metric (i.e., it considers fewer elements) than the interest coverage ratio. TRUE FALSE In a

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Quick Master Guide 2023 For Financial Business Growth A Comprehensive Beginners To Expert Guide To Financial And Managerial Accounting And Finance Professionals With Helpful Tips

Authors: Glorified Kathryn

1st Edition

979-8387518461