Answered step by step

Verified Expert Solution

Question

1 Approved Answer

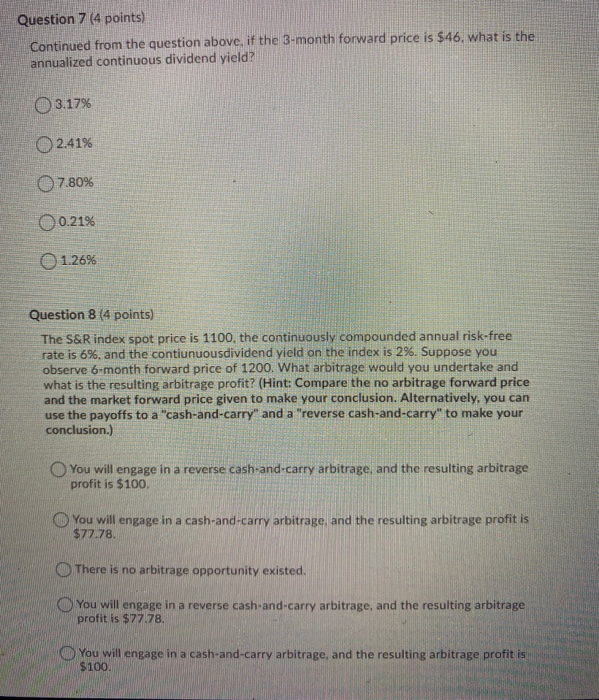

Question 7 (4 points) Continued from the question above, if the 3-month forward price is $46. what is the annualized continuous dividend yield? 3.17% 2.41%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Corporate Finance

Authors: Richard A. Brealey, Marcus, Alan J, Myers, Stewart C.

2nd Edition

0070074860, 9780070074866