Answered step by step

Verified Expert Solution

Question

1 Approved Answer

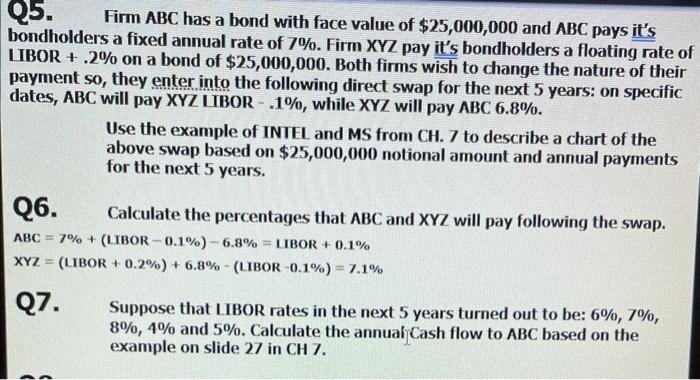

question 7 please Firm ABC has a bond with face value of $25,000,000 and ABC pays it's bondholders a fixed annual rate of 7%. Firm

question 7 please

Firm ABC has a bond with face value of $25,000,000 and ABC pays it's bondholders a fixed annual rate of 7%. Firm XYZ pay it's bondholders a floating rate IBOR +.2% on a bond of $25,000,000. Both firms wish to change the nature of their payment so, they enter into the following direct swap for the next 5 years: on specific dates, ABC will pay XYZ IIBOR - .1\%, while XYZ will pay ABC6.8%. Use the example of INIEL and MS from CH. 7 to describe a chart of the above swap based on $25,000,000 notional amount and annual payments for the next 5 years. Q6. Calculate the percentages that ABC and XYZ will pay following the swap. ABC=7%+(1IBOR0.1%)6.8%=1IBOR+0.1% XYZ=(LIBOR+0.2%)+6.8%(LIBOR0.1%)=7.1% Q7. Suppose that IIBOR rates in the next 5 years turned out to be: 6%,7%, 8%,4% and 5%. Calculate the annual Cash flow to ABC based on the example on slide 27 in CH7 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost Of Capital In Managerial Finance

Authors: Dennis Schlegel

2015th Edition

3319151347, 978-3319151342