Answered step by step

Verified Expert Solution

Question

1 Approved Answer

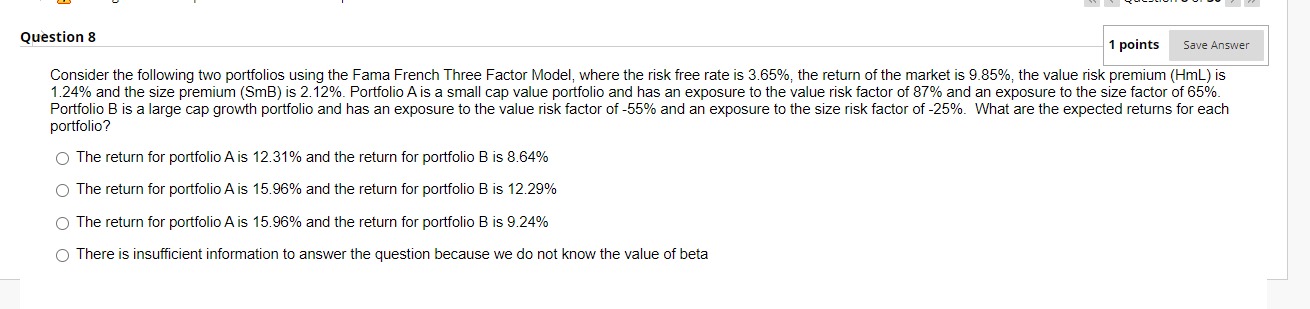

Question 8 1 points Save Answer Consider the following two portfolios using the Fama French Three Factor Model, where the risk free rate is

Question 8 1 points Save Answer Consider the following two portfolios using the Fama French Three Factor Model, where the risk free rate is 3.65%, the return of the market is 9.85%, the value risk premium (HmL) is 1.24% and the size premium (SMB) is 2.12%. Portfolio A is a small cap value portfolio and has an exposure to the value risk factor of 87% and an exposure to the size factor of 65%. Portfolio B is a large cap growth portfolio and has an exposure to the value risk factor of -55% and an exposure to the size risk factor of -25%. What are the expected returns for each portfolio? The return for portfolio A is 12.31% and the return for portfolio B is 8.64% The return for portfolio A is 15.96% and the return for portfolio B is 12.29% The return for portfolio A is 15.96% and the return for portfolio B is 9.24% There is insufficient information to answer the question because we do not know the value of beta

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Financial Management

Authors: James R Mcguigan, R Charles Moyer, William J Kretlow

10th Edition

978-0324289114, 0324289111