Answered step by step

Verified Expert Solution

Question

1 Approved Answer

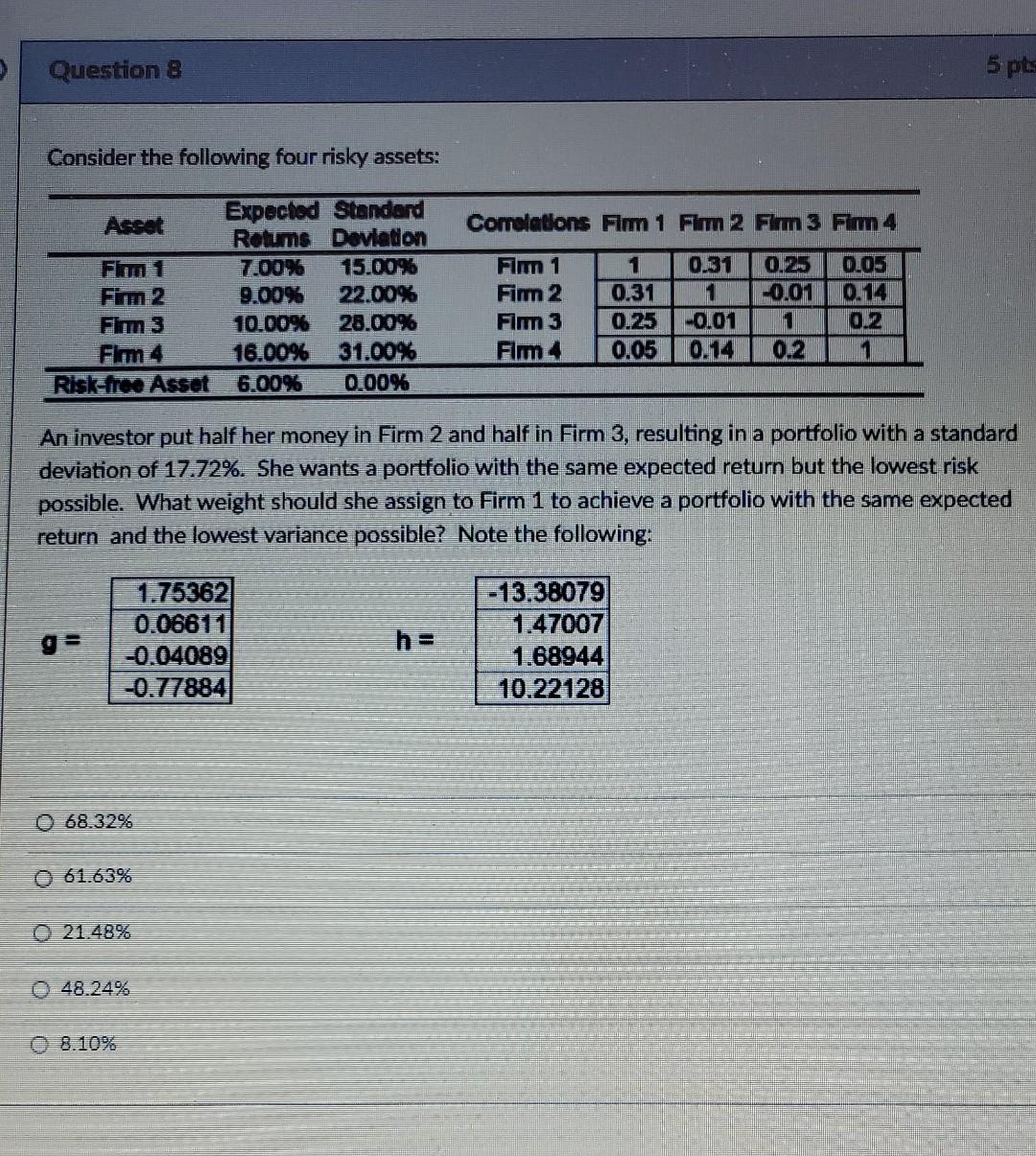

Question 8 5 pts Consider the following four risky assets: Comolations Firm 1 Firm 2 Firm 3 Fimm 4 0.31 Expected Standard Asset Rolums Davlation

Question 8 5 pts Consider the following four risky assets: Comolations Firm 1 Firm 2 Firm 3 Fimm 4 0.31 Expected Standard Asset Rolums Davlation 7.00146 15.00% Fimm 2 9.00% 22.00% Fimm 3 10.00% 28.00% 16.00% 31.00% Risk-free Asset 6.00% 0.00% 0.25 -0.01 Fim 1 Fimm 2 Fim 3 Flm24 1 0.31 0.25 0.05 0.05 0.14 012 1 -0.01 0.14 0.2 An investor put half her money in Firm 2 and half in Firm 3, resulting in a portfolio with a standard deviation of 17.72%. She wants a portfolio with the same expected return but the lowest risk possible. What weight should she assign to Firm 1 to achieve a portfolio with the same expected return and the lowest variance possible? Note the following: 1.75362 0.06611 -0.04089 -0.77884 h = -13.38079 1.47007 1.68944 10.22128 0 68.32% 061.63% O 21.48% 48.24% 08.10% Question 8 5 pts Consider the following four risky assets: Comolations Firm 1 Firm 2 Firm 3 Fimm 4 0.31 Expected Standard Asset Rolums Davlation 7.00146 15.00% Fimm 2 9.00% 22.00% Fimm 3 10.00% 28.00% 16.00% 31.00% Risk-free Asset 6.00% 0.00% 0.25 -0.01 Fim 1 Fimm 2 Fim 3 Flm24 1 0.31 0.25 0.05 0.05 0.14 012 1 -0.01 0.14 0.2 An investor put half her money in Firm 2 and half in Firm 3, resulting in a portfolio with a standard deviation of 17.72%. She wants a portfolio with the same expected return but the lowest risk possible. What weight should she assign to Firm 1 to achieve a portfolio with the same expected return and the lowest variance possible? Note the following: 1.75362 0.06611 -0.04089 -0.77884 h = -13.38079 1.47007 1.68944 10.22128 0 68.32% 061.63% O 21.48% 48.24% 08.10%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Healthcare Financial Management

Authors: Louis C. Gapenski, George H. Pink

6th Edition

1567933629, 9781567933628