Answered step by step

Verified Expert Solution

Question

1 Approved Answer

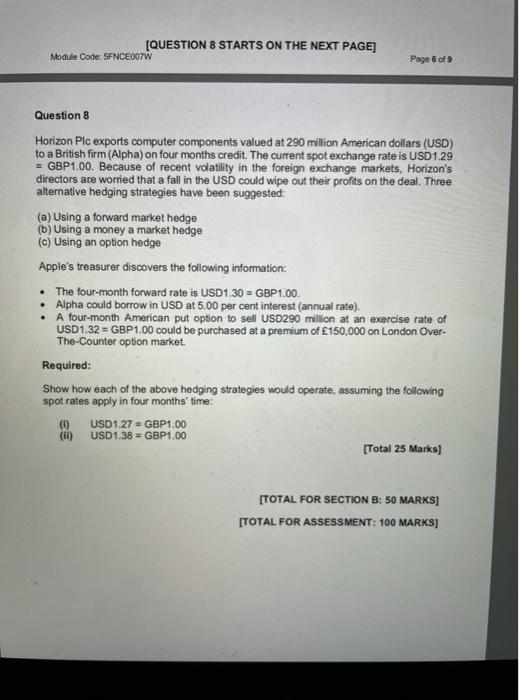

[QUESTION 8 STARTS ON THE NEXT PAGE) Module Code: 5FNCEDOTW Page 6 of 9 Question 8 Horizon Plc exports computer components valued at 290 million

[QUESTION 8 STARTS ON THE NEXT PAGE) Module Code: 5FNCEDOTW Page 6 of 9 Question 8 Horizon Plc exports computer components valued at 290 million American dollars (USD) to a British firm (Alpha) on four months credit . The current spot exchange rate is USD1.29 = GBP1.00. Because of recent volatility in the foreign exchange markets, Horizon's directors are worried that a fall in the USD could wipe out their profits on the deal. Three alternative hedging strategies have been suggested: (a) Using a forward market hedge (b) Using a money a market hedge (c) Using an option hedge Apple's treasurer discovers the following information: The four-month forward rate is USD1.30 GBP1.00. Alpha could borrow in USD at 5.00 per cent interest (annual rate) A four-month American put option to sell USD290 million at an exercise rate of USD1.32 = GBP 1.00 could be purchased at a premium of 150,000 on London Over- The-Counter option market Required: Show how each of the above hedging strategies would operate, assuming the following spot rates apply in four months' time: USD1.27 = GBP1.00 (11) USD1.38 = GBP1.00 [Total 25 Marks) . [TOTAL FOR SECTION B: 50 MARKS] [TOTAL FOR ASSESSMENT: 100 MARKS]

[QUESTION 8 STARTS ON THE NEXT PAGE) Module Code: 5FNCEDOTW Page 6 of 9 Question 8 Horizon Plc exports computer components valued at 290 million American dollars (USD) to a British firm (Alpha) on four months credit . The current spot exchange rate is USD1.29 = GBP1.00. Because of recent volatility in the foreign exchange markets, Horizon's directors are worried that a fall in the USD could wipe out their profits on the deal. Three alternative hedging strategies have been suggested: (a) Using a forward market hedge (b) Using a money a market hedge (c) Using an option hedge Apple's treasurer discovers the following information: The four-month forward rate is USD1.30 GBP1.00. Alpha could borrow in USD at 5.00 per cent interest (annual rate) A four-month American put option to sell USD290 million at an exercise rate of USD1.32 = GBP 1.00 could be purchased at a premium of 150,000 on London Over- The-Counter option market Required: Show how each of the above hedging strategies would operate, assuming the following spot rates apply in four months' time: USD1.27 = GBP1.00 (11) USD1.38 = GBP1.00 [Total 25 Marks) . [TOTAL FOR SECTION B: 50 MARKS] [TOTAL FOR ASSESSMENT: 100 MARKS]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Risk Management In Forex How To Minimize Losses And Maximize Returns

Authors: Eunice Loar

1st Edition

979-8388778864