Answered step by step

Verified Expert Solution

Question

1 Approved Answer

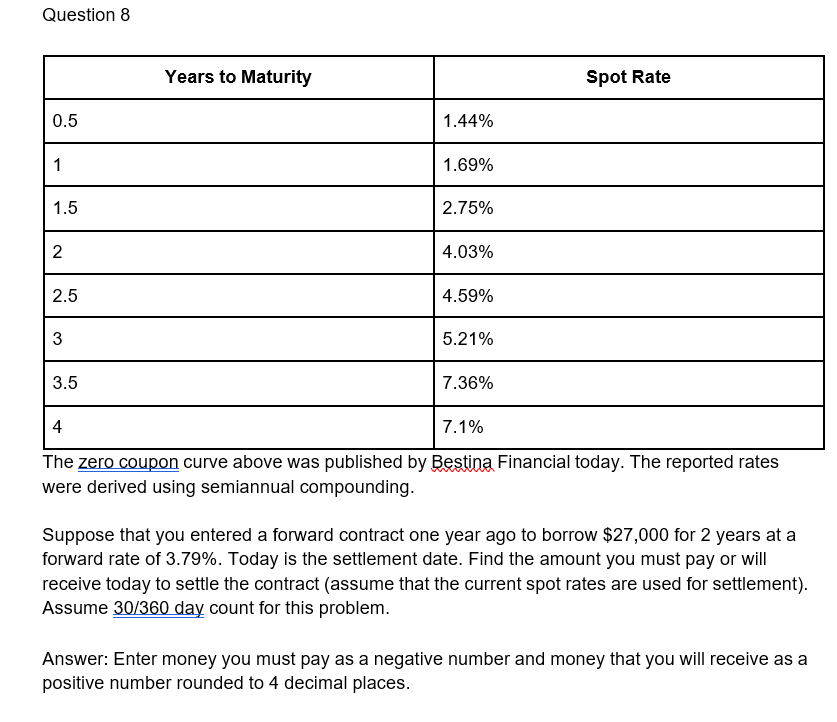

Question 8 The zero coupon curve above was published by Bestina Financial today. The reported rates were derived using semiannual compounding. Suppose that you entered

Question

The zero coupon curve above was published by Bestina Financial today. The reported rates

were derived using semiannual compounding.

Suppose that you entered a forward contract one year ago to borrow $ for years at a

forward rate of Today is the settlement date. Find the amount you must pay or will

receive today to settle the contract assume that the current spot rates are used for settlement

Assume

Answer: Enter money you must pay as a negative number and money that you will receive as a

positive number rounded to decimal places.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Global Financial Markets

Authors: Sabri Boubaker, Duc Khuong Nguyen

1st Edition

9813236647, 978-9813236646