Answered step by step

Verified Expert Solution

Question

1 Approved Answer

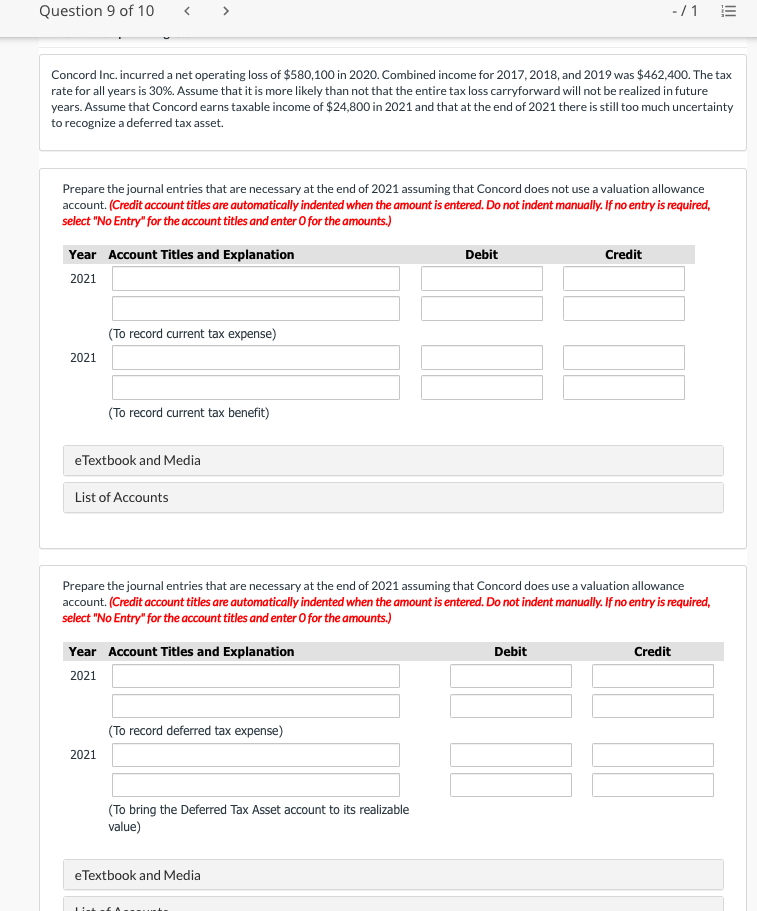

Question 9 of 10 - /1 E Concord Inc. incurred a net operating loss of $580,100 in 2020. Combined income for 2017, 2018, and 2019

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

QS 9000 Handbook A Guide To Registration And Audit

Authors: Jayanta Bandyopadhyay

1st Edition

157444011X, 978-1574440119