Answered step by step

Verified Expert Solution

Question

1 Approved Answer

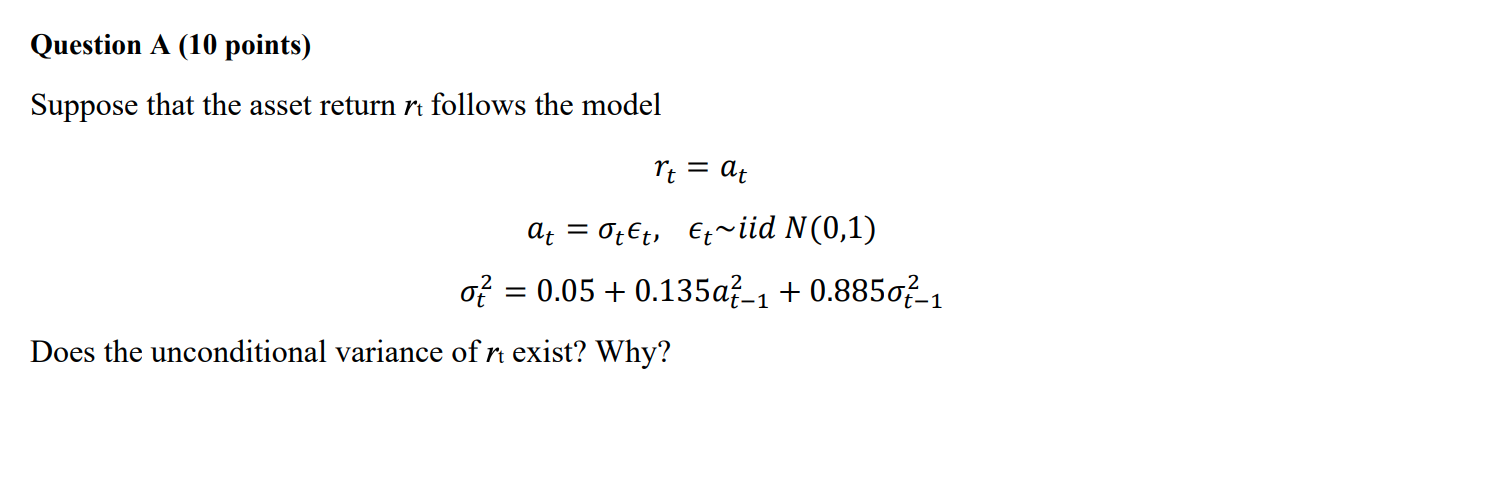

Question A (10 points) Suppose that the asset return rt follows the model rt = at = At = 0tet, Et~iid N(0,1) of = 0.05

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Gapenskis Fundamentals Of Healthcare Finance

Authors: Paula H. Song, Kristin L. Reiter

3rd Edition

1567939759, 978-1567939750