Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Question B2: (22 marks) The table below shows the information for exchange rates, interest rates and inflation rates in the US and Germany. Answer

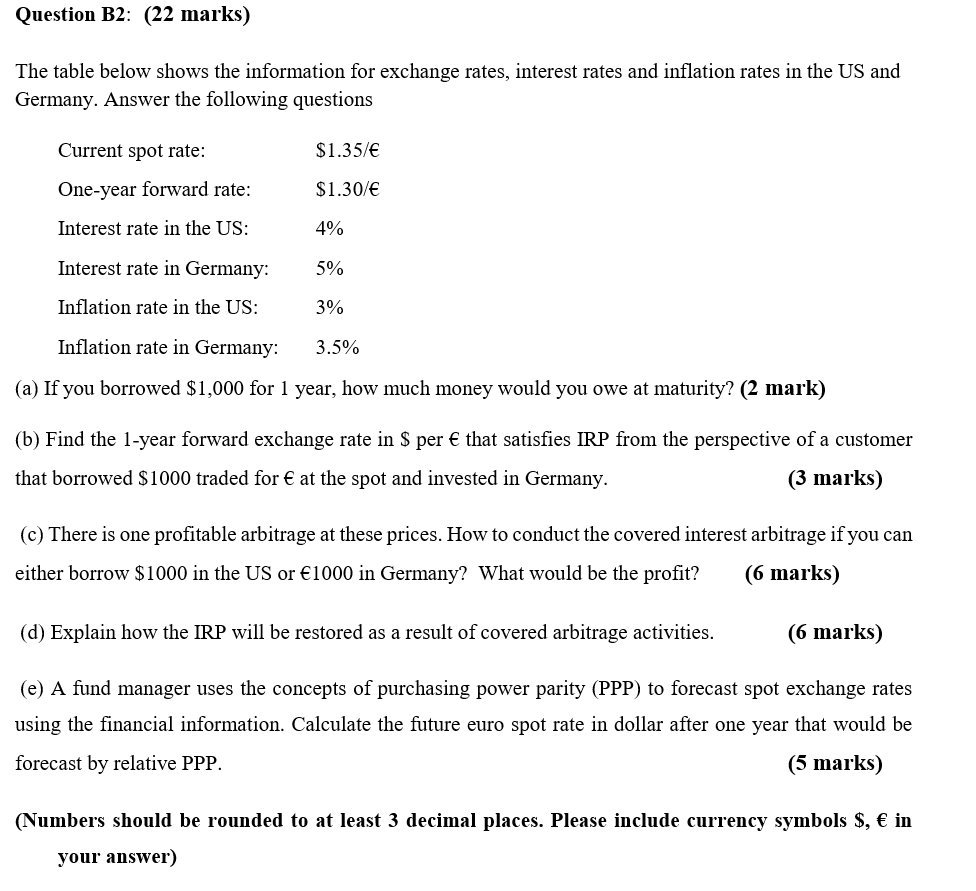

Question B2: (22 marks) The table below shows the information for exchange rates, interest rates and inflation rates in the US and Germany. Answer the following questions Current spot rate: $1.35/ One-year forward rate: $1.30/ Interest rate in the US: 4% Interest rate in Germany: 5% Inflation rate in the US: Inflation rate in Germany: 3% 3.5% (a) If you borrowed $1,000 for 1 year, how much money would you owe at maturity? (2 mark) (b) Find the 1-year forward exchange rate in $ per that satisfies IRP from the perspective of a customer that borrowed $1000 traded for at the spot and invested in Germany. (3 marks) (c) There is one profitable arbitrage at these prices. How to conduct the covered interest arbitrage if you can either borrow $1000 in the US or 1000 in Germany? What would be the profit? (6 marks) (d) Explain how the IRP will be restored as a result of covered arbitrage activities. (6 marks) (e) A fund manager uses the concepts of purchasing power parity (PPP) to forecast spot exchange rates using the financial information. Calculate the future euro spot rate in dollar after one year that would be forecast by relative PPP. (5 marks) (Numbers should be rounded to at least 3 decimal places. Please include currency symbols $, in your answer)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International financial management

Authors: Jeff Madura

9th Edition

978-0324593495, 324568207, 324568193, 032459349X, 9780324568202, 9780324568196, 978-0324593471