Answered step by step

Verified Expert Solution

Question

1 Approved Answer

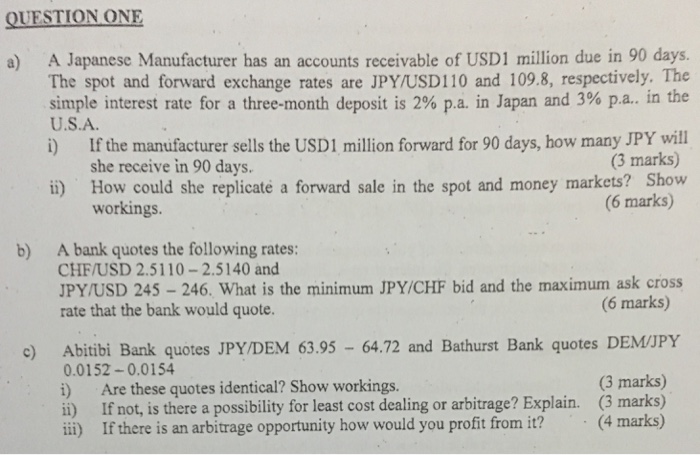

QUESTION ONE a) A Japanese Manufacturer has an accounts receivable of USD1 million due in 90 days The spot and forward exchange rates are JPY/USD110

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Doctrine Of Equivalents Or An Explanation Of The Nature Value And Power Of Money

Authors: George Craufurd

1st Edition

054833952X, 9780548339527