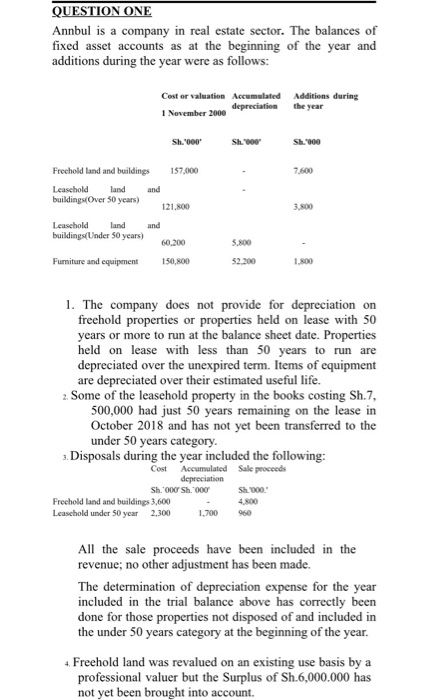

QUESTION ONE Annbul is a company in real estate sector. The balances of fixed asset accounts as at the beginning of the year and additions during the year were as follows: Cost or valuation Accumulated Additions during depreciation November 2000 the year Sh."000 Sh. Sh.000 7.600 Freehold land and buildings 157.000 Leasehold land and buildings(Over 50 years) 121,800 Leasehold land and buildings Under 50 years) 60.200 3800 5.00 Furniture and equipment 150.800 52.200 1.800 1. The company does not provide for depreciation on freehold properties or properties held on lease with 50 years or more to run at the balance sheet date. Properties held on lease with less than 50 years to run are depreciated over the unexpired term. Items of equipment are depreciated over their estimated useful life. 2. Some of the leasehold property in the books costing Sh.7, 500,000 had just 50 years remaining on the lease in October 2018 and has not yet been transferred to the under 50 years category. 3. Disposals during the year included the following: Cost Accumulated Sale proceeds depreciation Sh.'000 Sh. 000 Sh 1000 Freehold land and buildings 3,600 Leasehold under 50 year 2,300 1.700 All the sale proceeds have been included in the revenue; no other adjustment has been made. The determination of depreciation expense for the year included in the trial balance above has correctly been done for those properties not disposed of and included in the under 50 years category at the beginning of the year. 4. Freehold land was revalued on an existing use basis by a professional valuer but the Surplus of Sh.6,000.000 has not yet been brought into account. QUESTION ONE Annbul is a company in real estate sector. The balances of fixed asset accounts as at the beginning of the year and additions during the year were as follows: Cost or valuation Accumulated Additions during depreciation November 2000 the year Sh."000 Sh. Sh.000 7.600 Freehold land and buildings 157.000 Leasehold land and buildings(Over 50 years) 121,800 Leasehold land and buildings Under 50 years) 60.200 3800 5.00 Furniture and equipment 150.800 52.200 1.800 1. The company does not provide for depreciation on freehold properties or properties held on lease with 50 years or more to run at the balance sheet date. Properties held on lease with less than 50 years to run are depreciated over the unexpired term. Items of equipment are depreciated over their estimated useful life. 2. Some of the leasehold property in the books costing Sh.7, 500,000 had just 50 years remaining on the lease in October 2018 and has not yet been transferred to the under 50 years category. 3. Disposals during the year included the following: Cost Accumulated Sale proceeds depreciation Sh.'000 Sh. 000 Sh 1000 Freehold land and buildings 3,600 Leasehold under 50 year 2,300 1.700 All the sale proceeds have been included in the revenue; no other adjustment has been made. The determination of depreciation expense for the year included in the trial balance above has correctly been done for those properties not disposed of and included in the under 50 years category at the beginning of the year. 4. Freehold land was revalued on an existing use basis by a professional valuer but the Surplus of Sh.6,000.000 has not yet been brought into account