Answered step by step

Verified Expert Solution

Question

1 Approved Answer

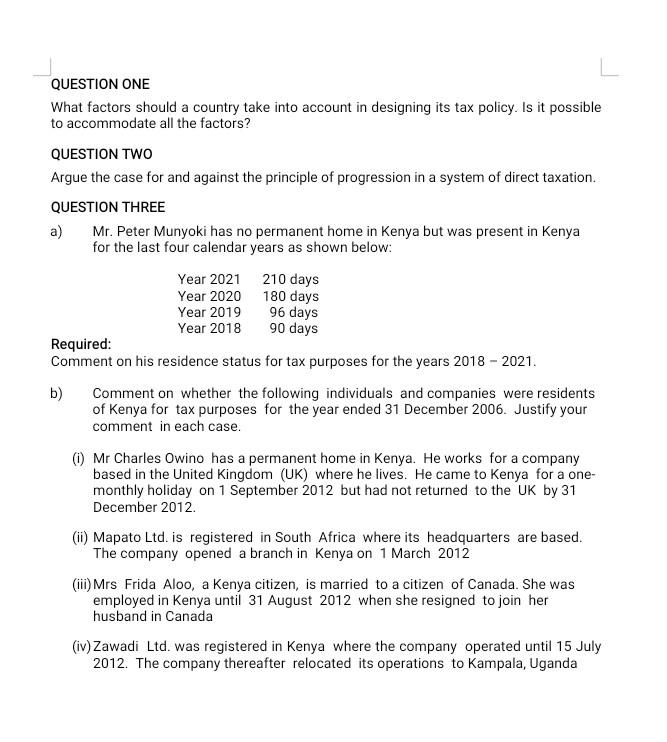

QUESTION ONE What factors should a country take into account in designing its tax policy. Is it possible to accommodate all the factors? QUESTION TWO

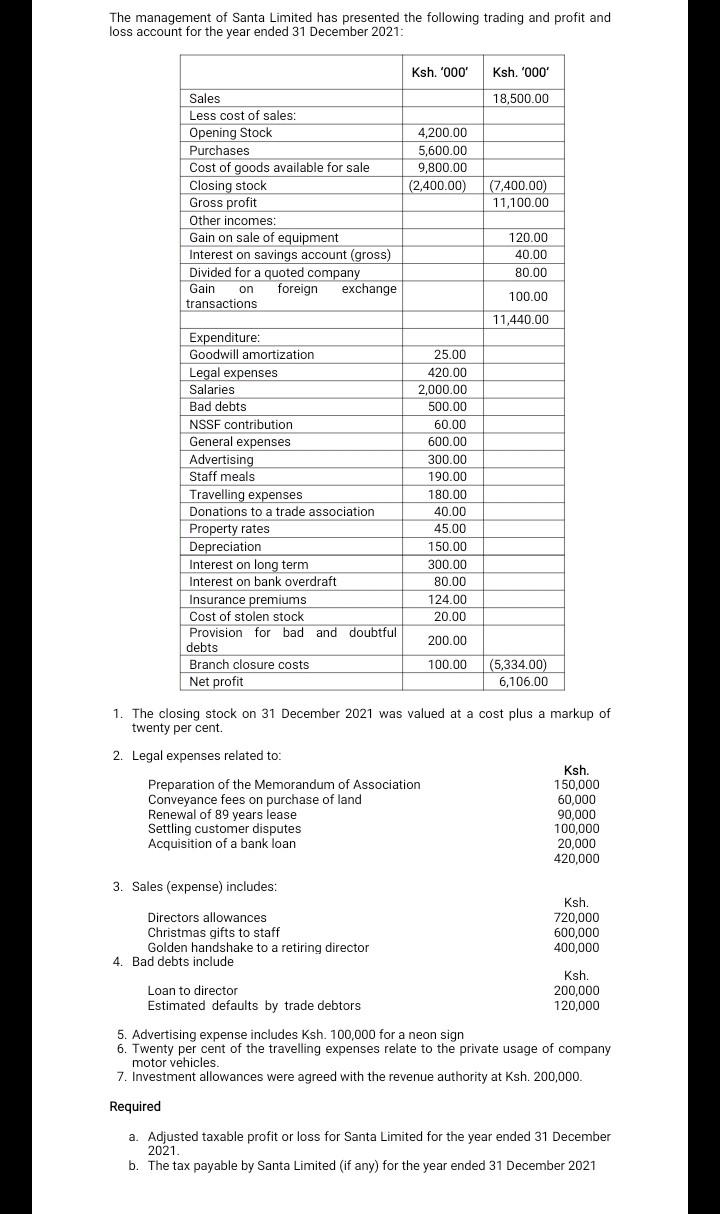

QUESTION ONE What factors should a country take into account in designing its tax policy. Is it possible to accommodate all the factors? QUESTION TWO Argue the case for and against the principle of progression in a system of direct taxation. QUESTION THREE a) Mr. Peter Munyoki has no permanent home in Kenya but was present in Kenya for the last four calendar years as shown below: Year 2021 Year 2020 Year 2019 Year 2018 210 days 180 days 96 days 90 days Required: Comment on his residence status for tax purposes for the years 2018 - 2021. b) Comment on whether the following individuals and companies were residents of Kenya for tax purposes for the year ended 31 December 2006. Justify your comment in each case. (i) Mr Charles Owino has a permanent home in Kenya. He works for a company based in the United Kingdom (UK) where he lives. He came to Kenya for a one- monthly holiday on 1 September 2012 but had not returned to the UK by 31 December 2012. (ii) Mapato Ltd. is registered in South Africa where its headquarters are based. The company opened a branch in Kenya on 1 March 2012 (iii) Mrs Frida Aloo, a Kenya citizen, is married to a citizen of Canada. She was employed in Kenya until 31 August 2012 when she resigned to join her husband in Canada (iv) Zawadi Ltd. was registered in Kenya where the company operated until 15 July 2012. The company thereafter relocated its operations to Kampala, Uganda The management of Santa Limited has presented the following trading and profit and loss account for the year ended 31 December 2021: Sales Less cost of sales: Opening Stock Purchases Cost of goods available for sale Closing stock Gross profit Other incomes: Gain on sale of equipment Interest on savings account (gross) Divided for a quoted company Gain on transactions foreign exchange Expenditure: Goodwill amortization Legal expenses Salaries Bad debts NSSF contribution. General expenses Advertising Staff meals Travelling expenses Donations to a trade association Property rates Depreciation Interest on long term Interest on bank overdraft Insurance premiums Cost of stolen stock Provision for bad and doubtful debts Branch closure costs Net profit 3. Sales (expense) includes: Directors allowances Christmas gifts to staff Preparation of the Memorandum of Association Conveyance fees on purchase of land Renewal of 89 years lease Settling customer disputes Acquisition of a bank loan Golden handshake to a retiring director 4. Bad debts include Ksh. '000' 4,200.00 5,600.00 9,800.00 (2,400.00) Loan to director Estimated defaults by trade debtors 25.00 420.00 2,000.00 500.00 60.00 600.00 300.00 190.00 180.00 40.00 45.00 150.00 300.00 80.00 124.00 20.00 200.00 100.00 1. The closing stock on 31 December 2021 was valued at a cost plus a markup of twenty per cent. 2. Legal expenses related to: Ksh. '000' 18,500.00 (7,400.00) 11,100.00 120.00 40.00 80.00 100.00 11,440.00 (5,334.00) 6,106.00 Ksh. 150,000 60,000 90,000 100,000 20,000 420,000 Ksh. 720,000 600,000 400,000 Ksh. 200,000 120,000 5. Advertising expense includes Ksh. 100,000 for a neon sign 6. Twenty per cent of the travelling expenses relate to the private usage of company motor vehicles. 7. Investment allowances were agreed with the revenue authority at Ksh. 200,000. Required a. Adjusted taxable profit or loss for Santa Limited for the year ended 31 December 2021. b. The tax payable by Santa Limited (if any) for the year ended 31 December 2021

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Complete FinOps Handbook Essential Tools And Techniques For Financial Operations

Authors: Peter Bates

1st Edition

1922435546, 978-1922435545