Answered step by step

Verified Expert Solution

Question

1 Approved Answer

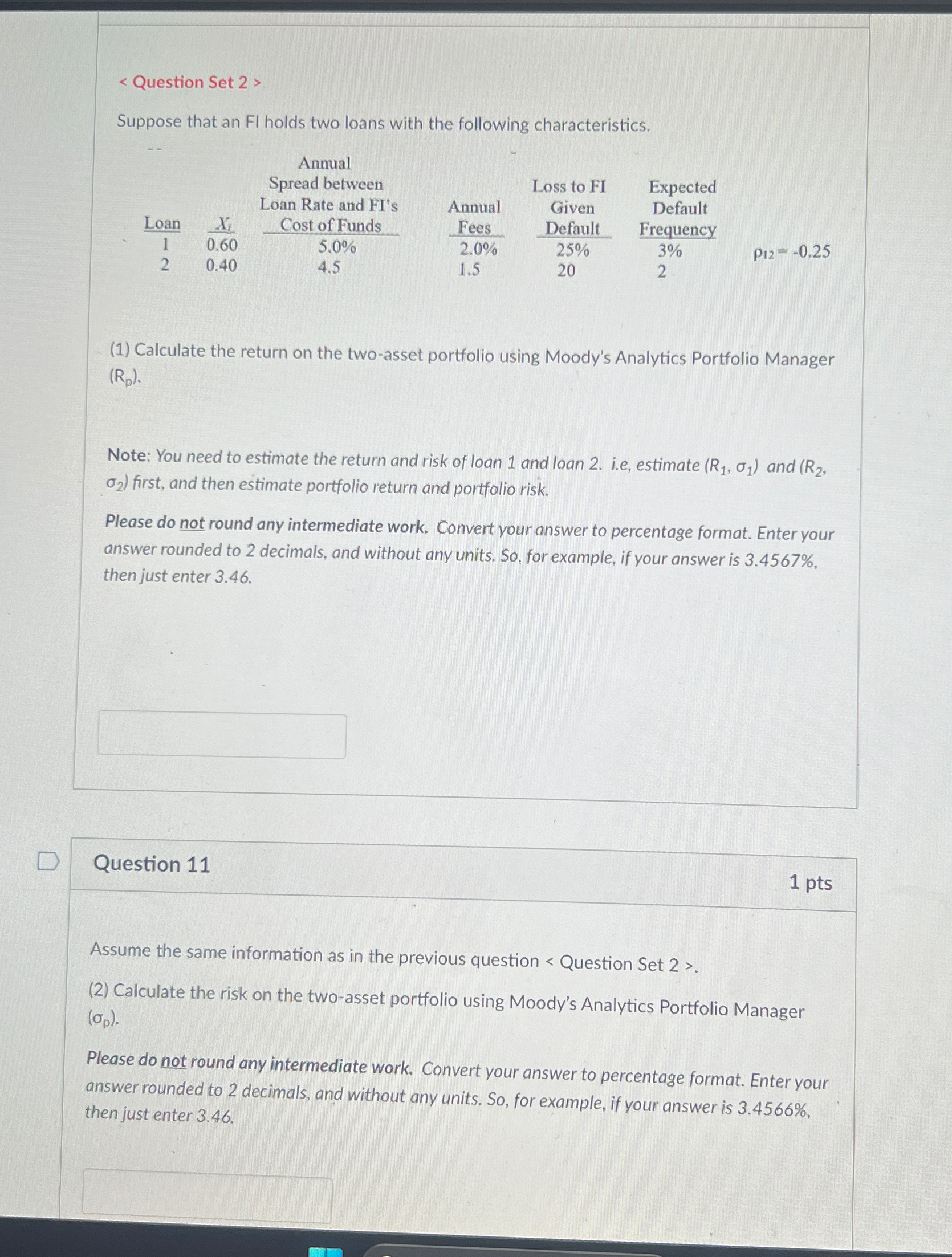

< Question Set 2 > Suppose that an Fl holds two loans with the following characteristics. Annual Spread between Loss to FI Expected Loan

< Question Set 2 > Suppose that an Fl holds two loans with the following characteristics. Annual Spread between Loss to FI Expected Loan Rate and FI's Annual Given Default Loan X 1 0.60 0.40 Cost of Funds 5.0% 4.5 Fees Default Frequency 2.0% 25% 3% P12=-0.25 1.5 20 2 (1) Calculate the return on the two-asset portfolio using Moody's Analytics Portfolio Manager (Rp). Note: You need to estimate the return and risk of loan 1 and loan 2. i.e, estimate (R1, 01) and (R2, 02) first, and then estimate portfolio return and portfolio risk. Please do not round any intermediate work. Convert your answer to percentage format. Enter your answer rounded to 2 decimals, and without any units. So, for example, if your answer is 3.4567%, then just enter 3.46. Question 11 1 pts Assume the same information as in the previous question < Question Set 2 > (2) Calculate the risk on the two-asset portfolio using Moody's Analytics Portfolio Manager (op). Please do not round any intermediate work. Convert your answer to percentage format. Enter your answer rounded to 2 decimals, and without any units. So, for example, if your answer is 3.4566%, then just enter 3.46.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance

Authors: Thomas Garman, Raymond Forgue

12th edition

9781305176409, 1133595839, 1305176405, 978-1133595830