Question

Question The closing inventory at 5 April 2023 is valued at 4,974. On 5 December 2022, Gloria sold a motor vehicle for 4,820. The customer

Question

- The closing inventory at 5 April 2023 is valued at £4,974.

- On 5 December 2022, Gloria sold a motor vehicle for £4,820. The customer was due to pay Gloria on 5 April 2023 but only paid half of the amount due by cheque on the last day of the accounting year. Nothing regarding the disposal transaction, including any cash received, has been recorded in the accounts. This motor vehicle had been bought on 6 October 2021 for £6,572.

- On 5 February 2023, Gloria bought a new motor vehicle for £12,000 on credit terms. The credit entry was correctly dealt with but Gloria mistakenly debited Fixtures and Fitting at cost.

- Depreciation on motor vehicles is provided at 25% per annum using the reducing balance basis on a monthly pro-rata basis. Depreciation on fixtures, fittings and equipment is provided at 15% per annum on the straight line basis, assuming no residual value. There were no purchases or disposals of fixtures, fittings, and equipment during the year.

- Gloria estimates that £1,864 due from customers will be irrecoverable and must be written off.

- The allowance for receivables is to be set at 4% of net receivables at 5 April 2023.

- Rent includes a prepayment of £580.

- The heating bill will arrive on 5 May 2023 and £390 is expected to relate to the period ended 5 April 2023.

- An accrual of £474 is needed for insurance.

- The long-term loan is repayable in 10 years' time. Interest payable on the loan is 5% and will be paid once per year.

Required:

a.Prepare the income statement for Gloria's Greengrocers for the period ended 5 April 2023. Your answer should only be in round pounds. Show your workings, including a full non-current assets note.

b. Prepare the balance sheet for Gloria's Greengrocers as at 5 April 2023. Show your workings. Your answer should only be in round pounds. Show your workings, including a full non-current assets note.

i. Explain the difference between accrued and prepaid expenses.

ii. Briefly explain the adjustments needed at the period-end for accrued expenses and prepaid expenses to prepare 'true and fair' financial statements. You must illustrate/support your explanation with examples using dates and figures. (Your answer should not involve double-entries nor T-accounts but should indicate the effect of the adjustments on the income statement and the balance sheet at the period-end. Your answer should also not include any discussion on the meaning of 'true and fair' financial statements.)

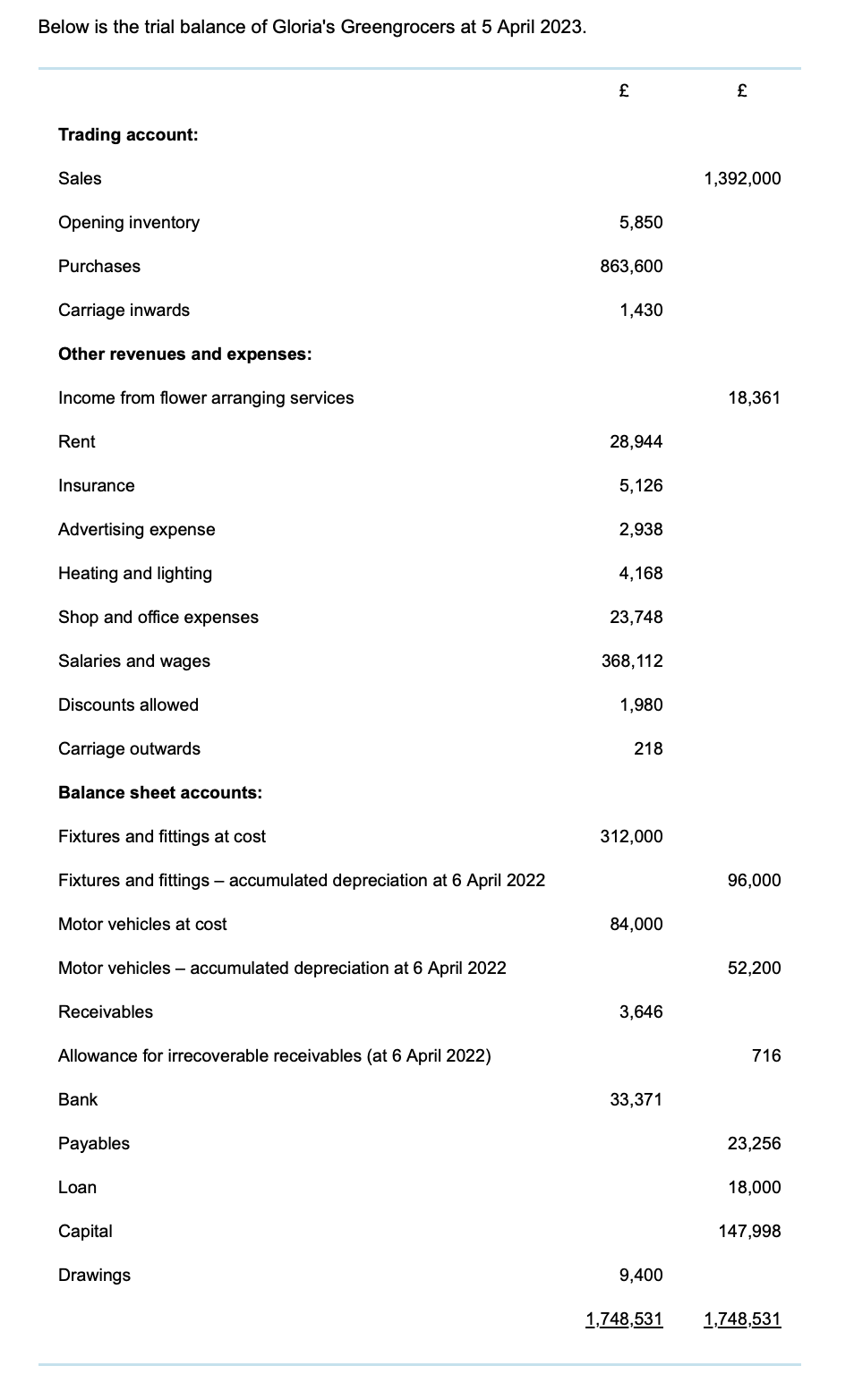

Below is the trial balance of Gloria's Greengrocers at 5 April 2023. Trading account: Sales Opening inventory Purchases Carriage inwards 1,392,000 5,850 863,600 1,430 Other revenues and expenses: Income from flower arranging services Rent 18,361 28,944 Insurance 5,126 Advertising expense 2,938 Heating and lighting 4,168 Shop and office expenses 23,748 Salaries and wages 368,112 Discounts allowed 1,980 Carriage outwards 218 Balance sheet accounts: Fixtures and fittings at cost 312,000 Fixtures and fittings - accumulated depreciation at 6 April 2022 96,000 Motor vehicles at cost 84,000 Motor vehicles - accumulated depreciation at 6 April 2022 52,200 Receivables Allowance for irrecoverable receivables (at 6 April 2022) 3,646 716 Bank Payables 33,371 23,256 Loan Capital 18,000 147,998 Drawings 9,400 1,748,531 1,748,531

Step by Step Solution

There are 3 Steps involved in it

Step: 1

a Income Statement for Glorias Greengrocers for the period ended 5 April 2023 Sales 1392000 Cost of Sales Opening Inventory 5850 Purchases 863600 Carriage Inwards 1430 Less Closing Inventory 4974 Cost ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamental Accounting

Authors: David Flynn, Carolina Koornhof, Ronald Arendse, Anna C. E. Coetzee, Edwardo Muriro, Louise Christel Posthumus, Louise Mancy Smit

7th Edition

1485112117, 9781485112112