Answered step by step

Verified Expert Solution

Question

1 Approved Answer

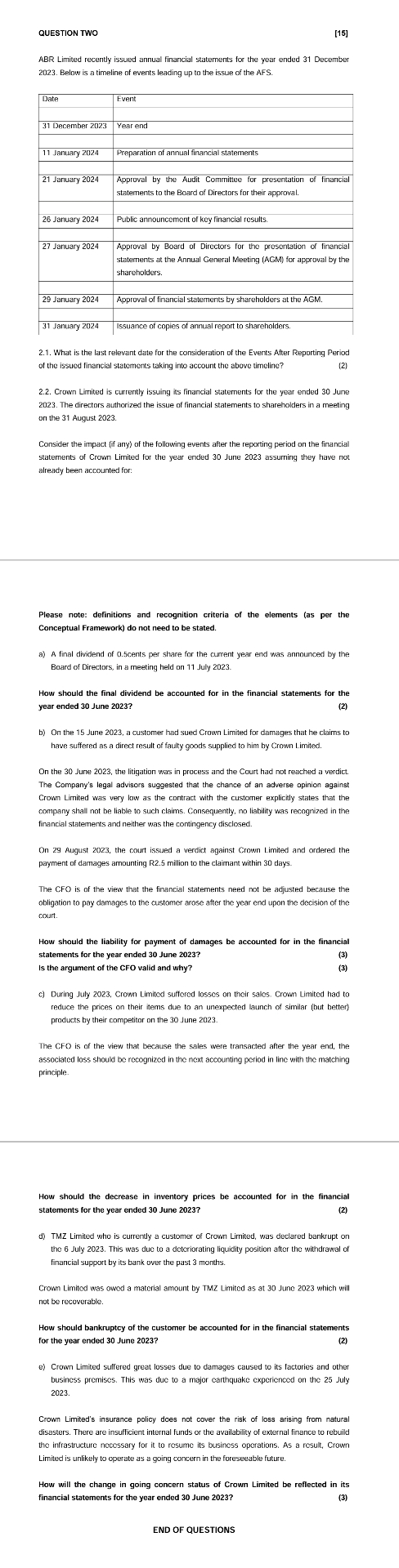

QUESTION TWO [ 1 5 ] ABR Limited recently issued anriual financial statements for the year ended 3 1 December 2 0 2 3 .

QUESTION TWO

ABR Limited recently issued anriual financial statements for the year ended December Below is a timeline of events leading up to the issue of the AFS.

table December Year end January January tableAppproval by the Audit Comrrittee for presentation of financialstatements to the Board of Directors for their approval. January Public announcement of key financial results. January tableApproval by Board of Directors for the presentation of financialstatements at the Annual General Meeting AGM for approval by theshareholders January Approval of financial statements by shareholders at the AGM.tableJanuary Issuance of copies of annual report to shareholders.

What is the last relevant date for the consideration of the Everts After Reporting Period of the issued financial statements taking into account the above timeline?

Crown Limited is currently issuing iss firancial statements for the year ended June The directors authorized the issue of financial statements to shareholders in a meeting on the August

Consider the impact f any of the following events after the repocting period on the financial statements of Crown Limited for the year ended June assurning they have not already been accounted for:

Please note: definitions and recognition criteria of the elements as per the Conceptual Framework do not need to be stated.

a A final dividend of cents per share for the current year end was announced by the Board of Dire:tors, in a meeting held on July

How should the final dividend be accounted for in the financial statements for the year ended June

b On the June a customer had sued Crown Limited for damages that he claims to have suffered as a direct result of faulty goods supplied to him by Crown Limited.

On the June the litigation was in process and the Court had not reached a verdict. The Company's legal advisors suggested that the chance of an adverse opinion against Crown Limited was very low as the contract with the custormer explicitly states that the company shall not be liable to such claims. Consequently, no liability was recognized in the financial statements and neither was the contingency disclosed.

On August the court issued a verdict against Crown Limited and ordered the payment of damages amounting R million to the claimant within days.

The CFO is of the view that the financial statements need not be adjusted berause the obligation to pay damages to the customer arose after the year end upon the decision of the court.

How should the liability for payment of damages be accounted for in the financial statements for the year ended June

is the argument of the CFO valid and why?

c During July Crown Limited suffered losses on their sales. Crown Limited had to reduce the prices on their items due to an unexpected launch of similar but hetter products by their competitor on the June

The CFO is of the viem that because the sales were transacted after the year end, the associated loss should be recognized in the next accounting period in line with the matching principle.

How should the decrease in inventory prices be accounted for in the financial statements for the year ended June

d TMZ Limited who is currently a customer of Crown Lirnited, was declared bankrupt on the July This was due to a deteriorating liquidity position after the withdrawal of financial support by its bank over the past months.

Crown Limited was owed a material amount by TMZ Limited as at June which will not be recoverable.

How should bankruptcy of the customer be accounted for in the financial statements for the year ended June

e Crown Limited suffered great losses due to damages caused to its factories and other business premises. This was due to a major carthquake experienced on the July

Crown Limited's insurance policy does not cover the risk of loss arising from natural disasters. There are insufficient internal funds or the availability of external finance to rebuild the infrastructure necessary for it to resume its business operations. As a result, Crown Limited is unlikely to operate as a going concern in the foreseeable future.

How will the change in going concern status of Crown Limited be reflected in its financial statements for the year ended June

END OF QUESTIONS

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Budgeting Auditing And Evaluation Functions And Integration In Seven Governments

Authors: Andrew Gray

1st Edition

0765807246, 9780765807243