Answered step by step

Verified Expert Solution

Question

1 Approved Answer

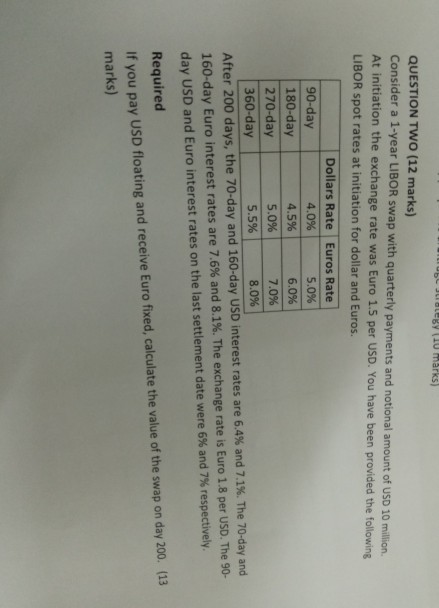

QUESTION TWO (12 marks) Consider a 1-year LIBOR swap with quarterly payments and notional amount of USD 10 milin At initiation the exchange rate was

QUESTION TWO (12 marks) Consider a 1-year LIBOR swap with quarterly payments and notional amount of USD 10 milin At initiation the exchange rate was Euro 1.5 per USD. You have been provided the following LIBOR spot rates at initiation for dollar and Euros. 90-day 180-day 270-day 360-day Dollars Rate Euros Rate 5.0% 6.0% 7.0% 8.0% 4.0% 4.5% 5.0% 5.5% After 200 days, the 70-day and 160-day USD interest rates are 6.4% and 7.1%. The 70-day and 160-day Euro interest rates are 7.6% and 8.1%. The exchange rate is Euro 1.8 per USD. The 90- day USD and Euro interest rates on the last settlement date were 6% and 7% respectively. Required If you pay USD floating and receive Euro fixed, calculate the value of the swap on day 200. (13 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Financial Theory

Authors: Jean-Pierre Danthine, John B. Donaldson

2nd Edition

0123693802, 978-0123693808