Answered step by step

Verified Expert Solution

Question

1 Approved Answer

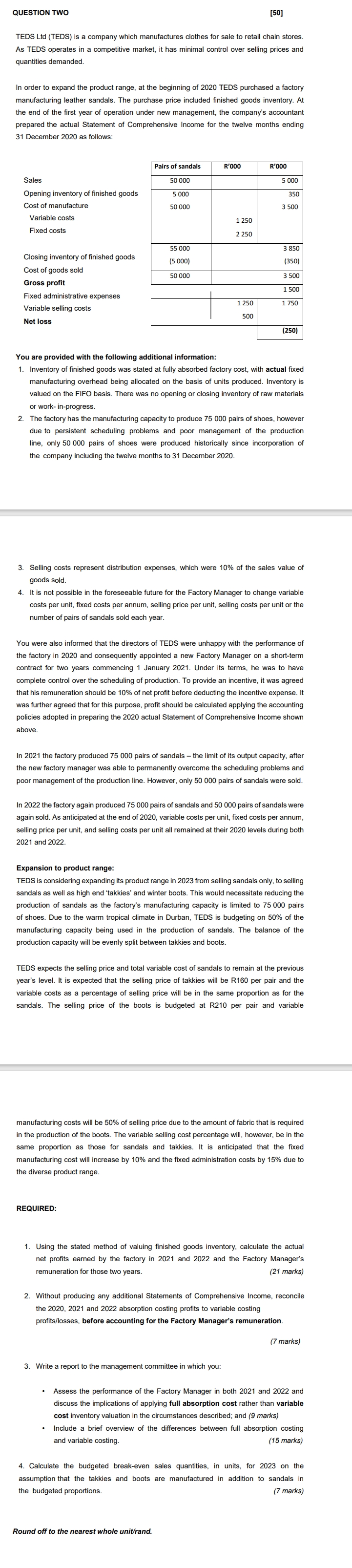

QUESTION TWO TEDS Ltd ( TEDS ) is a company which manufactures clothes for sale to retail chain stores As TEDS operates in a competitive

QUESTION TWO

TEDS Ltd TEDS is a company which manufactures clothes for sale to retail chain stores

As TEDS operates in a competitive market, it has minimal control over selling prices and

quantities demanded.

In order to expand the product range, at the beginning of TEDS purchased a factory

manufacturing leather sandals. The purchase price included finished goods inventory. At

prepared the actual Statement of Comprehensive Income for the twelve months ending

December as follows:

You are provided with the following additional information:

Inventory of finished goods was stated at fully absorbed factory cost, with actual fixed

manufacturing overhead being allocated on the basis of units produced. Inventory is

valued on the FIFO basis. There was no opening or closing inventory of raw materials

or work inprogress

he factory has the manufacturing capacity to produce pairs of shoes, howeve

due to persistent scheduling problems and poor management of the production

line, only pairs of shoes were produced historically since incorporation of

the company including the twelve months to December

Selling costs represent distribution expenses, which were of the sales value of

goods sold.

It is not possible in the foreseeable future for the Factory Manager to change variable

costs per unit, fixed costs per annum, selling price per unit, selling costs per unit or the

number of pairs of sandals sold each year.

You were also informed that the directors of TEDS were unhappy with the performance of

he factory in and consequently appointed a new Factory Manager on a shorterm

contract for two years commencing January Under its terms, he was to have

complete control over the scheduling of production. To provide an incentive, it was agreed

was further agreed that for this purpose, profit should deding the incentive expense. It

was further agreed that for this purpose, profit should be calculated applying the accounting

the acted in preparing the actual Statement of Comprehensive Income shown

In the factory produced pairs of sandals the limit of its output capacity, after

the new factory manager was able to permanently overcome the scheduling problems and

poor management of the production line. However, only pairs of sandals were sold.

In the factory again produced pairs of sandals and pairs of sandals were

gain sold. As anticipated at the end of variable costs per unit, fixed costs per annum,

and selling costs per unit all remained at their levels during both

Expansion to product range:

TEDS is considering expanding its product range in from selling sandals only, to selling

production of sandals as the factory's manufacturing capacity is limited to pair

f shoes. Due to the warm tropical climate in Durban, TEDS is budgeting pair

manufacturing capacity being used in the production of sandals. The balance of the

production capacity will be evenly split between takkies and boots.

TEDS expects the selling price and total variable cost of sandals to remain at the previous

year's level. It is expected that the selling price of takkies will be R per pair and the

variable costs as a percentage of selling price will be in the same proportion as for the

sandals. The selling price of the boots is budgeted at R per pair and variable

manufacturing costs will be of selling price due to the amount of fabric that is required

in the production of the boots. The variable selling cost percentage will, however, be in the

same proportion as those for sandals and takkies. It is anticipated that the fixed

the divacturing cost will increase by and the fixed administration costs by due to

he diverse product range.

REQUIRED:

Using the stated method of valuing finished goods inventory, calculate the actua

net profits earned by the factory in and and the Factory Manager's

remuneration for those two years. marks

Without producing any additional Statements of Comprehensive Income, reconcile

the and absorption costing profits to variable costing

profitslosses before accounting for the Factory Manager's remuneration.

marks

Write a report to the management committee in which you:

Assess the performance of the Factory Manager in both and and

discuss the implications of applying full absorption cost rather than variable

cost inventory valuation in the circumstances described; and marks

Include a brief overview of the differences between full absorption costing

and variable costing

Calculate the budgeted breakeven sales quantities, in units, for on the

assumption that the takkies and boots are manufactured in addition to sandals in

the budgeted proportions.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting An Introduction to Concepts Methods and Uses

Authors: Michael W. Maher, Clyde P. Stickney, Roman L. Weil

10th Edition

1111822239, 324639767, 9781111822231, 978-0324639766