Answered step by step

Verified Expert Solution

Question

1 Approved Answer

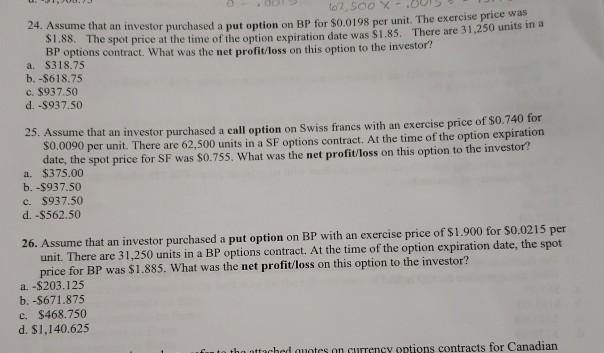

questions 24-26. will give upvote if all is worked out!!! thank you!! at an investor purchased a put option on BP for $0.0198 per unit.

questions 24-26. will give upvote if all is worked out!!! thank you!!

at an investor purchased a put option on BP for $0.0198 per unit. The exercise price was e spot price at the time of the option expiration date was $1.85. There are 31,250 units in a 24. Assume th $1.88. Th BP options contract. What was the net profit/loss on this option to the investor? a. $318.75 b. -$618.75 c. $937.50 d.-$937.50 e that an investor purchased a call option on Swiss francs with an exercise price of $0.740 for 0 per unit. There are 62.500 units in a SF options contract. At the time of the option expiration S0.009 date, the spot price for SF was S0.755. What was the net profitloss on this option to the investor? a. $375.00 b. -$937.50 C. $937.50 d. -$562.50 26. Assume that an investor purchased a put option on BP with an exercise price of $1.900 for $0.0215 per unit. There are 31,250 units in a BP options contract. At the time of the option expiration date, the spot price for BP was $1.885. What was the net profit/loss on this option to the investor? a. -$203.125 b.-$671.875 0 c. $468.75 d. $1,140.625 fu to tho nttached untes on currency ontions contracts for CanadianStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Investment Management

Authors: Geoffrey Hirt, Stanley Block

10th edition

0078034620, 978-0078034626