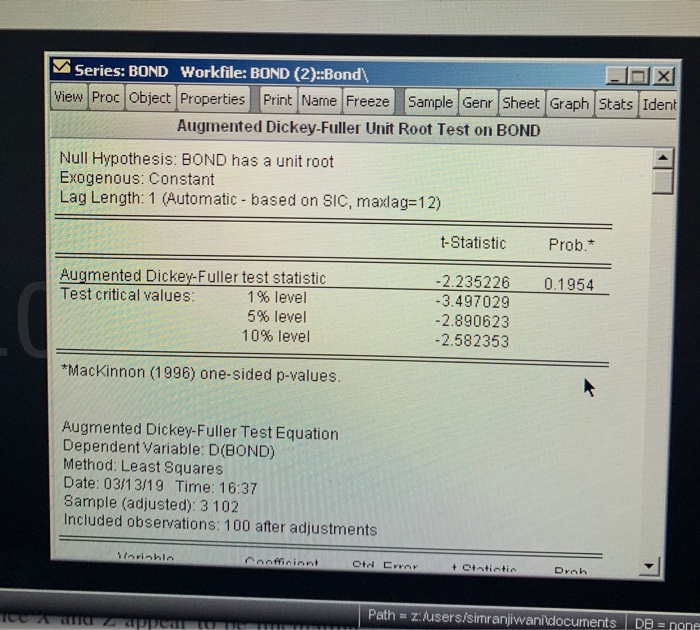

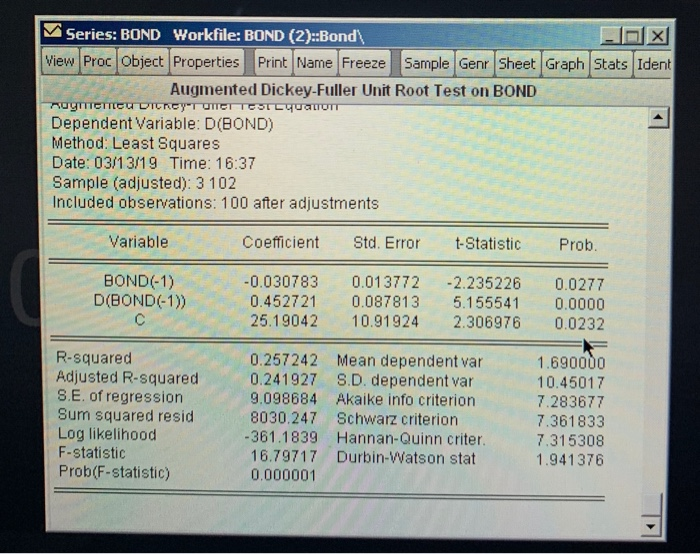

questions b-d using the given results from unit root test

12.5 The data file bond.dat contains 102 monthly observations on AA railroad bond yields for the period January 1968 to June 1976. (a) Plot the data. Do railroad bond yields appear stationary, or nonstationary? (b) Use a unit root test to demonstrate that the series is nonstationary (c) Find the first difference of the bond yield series and test for stationarity. (d) What do you conclude about the order of integration of this series? Series: BOND Workfile: BOND (2):Bond View Proc object Properties Print Name Freeze Sample Genr Sheet Graph Stats Ident Augmented Dickey-Fuller Unit Root Test on BOND Null Hypothesis: BOND has a unit root Exogenous: Constant Lag Length: 1 (Automatic - based on SIC, maxlag-12) t-Statistic Prob.* Augmented Dickey-Fuller test statistic Test critical values: 1 % level 5% level 10% level -2.235226 0.1954 -3.497029 2.890623 -2.582353 "MacKinnon (1996) one-sided p-values. Augmented Dickey-Fuller Test Equation Dependent Variable: D(BOND) Method: Least Squares Date: 03/13/19 Time: 16:37 Sample (adjusted): 3 102 Included observations: 100 after adjustments Path zusers/simranjiwanidocuments DB none Series: BOND Workfile: BOND (2):Bond View Proc object Properties Print Name Freeze Sample Genr Sheet Graph Stats Ident Augmented Dickey-Fuller Unit Root Test on BOND ugTnerne Dependent Variable: D(BOND) Method: Least Squares Date: 03/13/19 Time: 16:37 Sample (adjusted): 3 102 Included observations: 100 after adjustments Variable Coefficient Std. Error t-Statistic Prob BOND(-1) D(BOND-1)) -0.030783 0.013772 -2.235226 0.0277 0.452721 0.087813 5.155541 0.0000 25.19042 10.91924 2.306976 0.0232 R-squared Adjusted R-squared S.E. of regression Sum squared resid Log likelihood F-statistic Prob(F-statistic) 0.257242 Mean dependent var 0.241927 S.D. dependent var 9.098684 Akaike info criterion 8030.247 Schwarz criterion 361.1839 Hannan-Quinn criter 16.79717 Durbin-Watson stat 0.000001 1.690000 10.45017 7.283677 7.361833 7.315308 1.941376 12.5 The data file bond.dat contains 102 monthly observations on AA railroad bond yields for the period January 1968 to June 1976. (a) Plot the data. Do railroad bond yields appear stationary, or nonstationary? (b) Use a unit root test to demonstrate that the series is nonstationary (c) Find the first difference of the bond yield series and test for stationarity. (d) What do you conclude about the order of integration of this series? Series: BOND Workfile: BOND (2):Bond View Proc object Properties Print Name Freeze Sample Genr Sheet Graph Stats Ident Augmented Dickey-Fuller Unit Root Test on BOND Null Hypothesis: BOND has a unit root Exogenous: Constant Lag Length: 1 (Automatic - based on SIC, maxlag-12) t-Statistic Prob.* Augmented Dickey-Fuller test statistic Test critical values: 1 % level 5% level 10% level -2.235226 0.1954 -3.497029 2.890623 -2.582353 "MacKinnon (1996) one-sided p-values. Augmented Dickey-Fuller Test Equation Dependent Variable: D(BOND) Method: Least Squares Date: 03/13/19 Time: 16:37 Sample (adjusted): 3 102 Included observations: 100 after adjustments Path zusers/simranjiwanidocuments DB none Series: BOND Workfile: BOND (2):Bond View Proc object Properties Print Name Freeze Sample Genr Sheet Graph Stats Ident Augmented Dickey-Fuller Unit Root Test on BOND ugTnerne Dependent Variable: D(BOND) Method: Least Squares Date: 03/13/19 Time: 16:37 Sample (adjusted): 3 102 Included observations: 100 after adjustments Variable Coefficient Std. Error t-Statistic Prob BOND(-1) D(BOND-1)) -0.030783 0.013772 -2.235226 0.0277 0.452721 0.087813 5.155541 0.0000 25.19042 10.91924 2.306976 0.0232 R-squared Adjusted R-squared S.E. of regression Sum squared resid Log likelihood F-statistic Prob(F-statistic) 0.257242 Mean dependent var 0.241927 S.D. dependent var 9.098684 Akaike info criterion 8030.247 Schwarz criterion 361.1839 Hannan-Quinn criter 16.79717 Durbin-Watson stat 0.000001 1.690000 10.45017 7.283677 7.361833 7.315308 1.941376