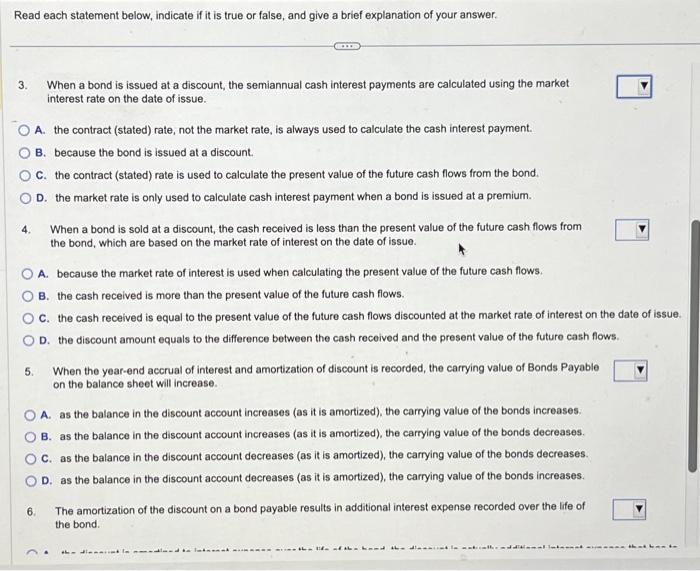

Read each statement below, indicate if it is true or false, and give a brief explanation of your answer. 3. 4. 5. When a bond is issued at a discount, the semiannual cash interest payments are calculated using the market interest rate on the date of issue. A. the contract (stated) rate, not the market rate, is always used to calculate the cash interest payment. B. because the bond is issued at a discount. C. the contract (stated) rate is used to calculate the present value of the future cash flows from the bond. D. the market rate is only used to calculate cash interest payment when a bond is issued at a premium. A. because the market rate of interest is used when calculating the present value of the future cash flows. B. the cash received is more than the present value of the future cash flows. OC. the cash received is equal to the present value of the future cash flows discounted at the market rate of interest on the date of issue. D. the discount amount equals to the difference between the cash received and the present value of the future cash flows. When a bond is sold at a discount, the cash received is less than the present value of the future cash flows from the bond, which are based on the market rate of interest on the date of issue. 6. When the year-end accrual of interest and amortization of discount is recorded, the carrying value of Bonds Payable on the balance sheet will increase. A. as the balance in the discount account increases (as it is amortized), the carrying value of the bonds increases. B. as the balance in the discount account increases (as it is amortized), the carrying value of the bonds decreases. C. as the balance in the discount account decreases (as it is amortized), the carrying value of the bonds decreases. OD. as the balance in the discount account decreases (as it is amortized), the carrying value of the bonds increases. The amortization of the discount on a bond payable results in additional interest expense recorded over the life of the bond. the diamant in maimed to intrunat mint life of the hand the di La

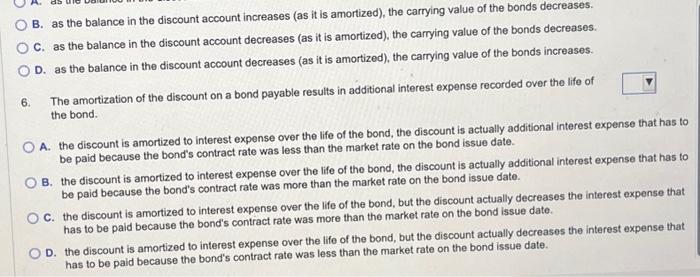

Read each statement below, indicate if it is true or false, and give a brief explanation of your answer. 3. When a bond is issued at a discount, the semiannual cash interest payments are calculated using the market interest rate on the date of issue. A. the contract (stated) rate, not the market rate, is always used to calculate the cash interest payment. B. because the bond is issued at a discount. C. the contract (stated) rate is used to calculate the present value of the future cash flows from the bond. D. the market rate is only used to calculate cash interest payment when a bond is issued at a premium. 4. When a bond is sold at a discount, the cash received is less than the present value of the future cash flows from the bond, which are based on the market rate of interest on the date of issue. A. because the market rate of interest is used when calculating the present value of the future cash flows. B. the cash received is more than the present value of the future cash flows. C. the cash received is equal to the present value of the future cash flows discounted at the market rate of interest on the date of issue. D. the discount amount equals to the difference between the cash recoived and the present value of the future cash flows. 5. When the year-end accrual of interest and amortization of discount is recorded, the carrying value of Bonds Payable on the balance sheet will increase. A. as the balance in the discount account increases (as it is amortized), the carrying value of the bonds increases. B. as the balance in the discount account increases (as it is amortized), the carrying value of the bonds decreases. C. as the balance in the discount account decreases (as it is amortized), the carrying value of the bonds decreases. D. as the balance in the discount account decreases (as it is amortized), the carrying value of the bonds increases. 6. The amortization of the discount on a bond payable results in additional interest expense recorded over the life of the bond. B. as the balance in the discount account increases (as it is amortized), the carrying value of the bonds decreases. C. as the balance in the discount account decreases (as it is amortized), the carrying value of the bonds decreases. D. as the balance in the discount account decreases (as it is amortized), the carrying value of the bonds increases. 6. The amortization of the discount on a bond payable results in additional interest expense recorded over the life of the bond. A. the discount is amortized to interest expense over the life of the bond, the discount is actually additional interest expense that has to be paid because the bond's contract rate was less than the market rate on the bond issue date. B. the discount is amortized to interest expense over the life of the bond, the discount is actually additional interest expense that has to be paid because the bond's contract rate was more than the market rate on the bond issue date. C. the discount is amortized to interest expense over the life of the bond, but the discount actually decreases the interest expense that has to be paid because the bond's contract rate was more than the market rate on the bond issue date. D. the discount is amortized to interest expense over the life of the bond, but the discount actually decreases the interest expense that has to be paid because the bond's contract rate was less than the market rate on the bond issue date. Read each statement below, indicate if it is true or false, and give a brief explanation of your answer. 3. When a bond is issued at a discount, the semiannual cash interest payments are calculated using the market interest rate on the date of issue. A. the contract (stated) rate, not the market rate, is always used to calculate the cash interest payment. B. because the bond is issued at a discount. C. the contract (stated) rate is used to calculate the present value of the future cash flows from the bond. D. the market rate is only used to calculate cash interest payment when a bond is issued at a premium. 4. When a bond is sold at a discount, the cash received is less than the present value of the future cash flows from the bond, which are based on the market rate of interest on the date of issue. A. because the market rate of interest is used when calculating the present value of the future cash flows. B. the cash received is more than the present value of the future cash flows. C. the cash received is equal to the present value of the future cash flows discounted at the market rate of interest on the date of issue. D. the discount amount equals to the difference between the cash recoived and the present value of the future cash flows. 5. When the year-end accrual of interest and amortization of discount is recorded, the carrying value of Bonds Payable on the balance sheet will increase. A. as the balance in the discount account increases (as it is amortized), the carrying value of the bonds increases. B. as the balance in the discount account increases (as it is amortized), the carrying value of the bonds decreases. C. as the balance in the discount account decreases (as it is amortized), the carrying value of the bonds decreases. D. as the balance in the discount account decreases (as it is amortized), the carrying value of the bonds increases. 6. The amortization of the discount on a bond payable results in additional interest expense recorded over the life of the bond. B. as the balance in the discount account increases (as it is amortized), the carrying value of the bonds decreases. C. as the balance in the discount account decreases (as it is amortized), the carrying value of the bonds decreases. D. as the balance in the discount account decreases (as it is amortized), the carrying value of the bonds increases. 6. The amortization of the discount on a bond payable results in additional interest expense recorded over the life of the bond. A. the discount is amortized to interest expense over the life of the bond, the discount is actually additional interest expense that has to be paid because the bond's contract rate was less than the market rate on the bond issue date. B. the discount is amortized to interest expense over the life of the bond, the discount is actually additional interest expense that has to be paid because the bond's contract rate was more than the market rate on the bond issue date. C. the discount is amortized to interest expense over the life of the bond, but the discount actually decreases the interest expense that has to be paid because the bond's contract rate was more than the market rate on the bond issue date. D. the discount is amortized to interest expense over the life of the bond, but the discount actually decreases the interest expense that has to be paid because the bond's contract rate was less than the market rate on the bond issue date