Question

Read the case Budgeting and Performance Evaluation at the Berkshire Toy Company. Please read the Class Preparation section of this homework before you start working

Read the case Budgeting and Performance Evaluation at the Berkshire Toy Company.

Please read the Class Preparation section of this homework before you start working on the homework.

Prepare and submit the answers to questions 1 and 2 below:

1.

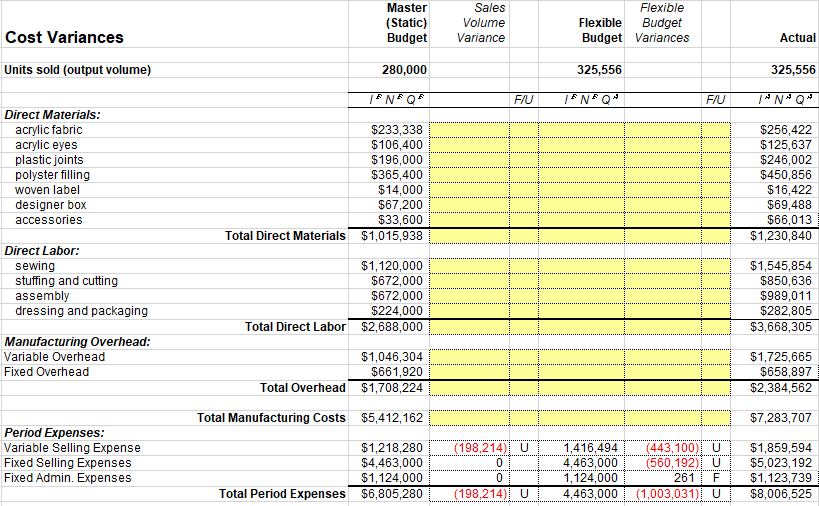

- (To facilitate this question I provide an excel table) Using the information in the case and Tables 15, prepare a flexible budget for the Berkshire Toy Company for the year ended June 30, 1998. Analyze the companys total master (static) budget variance for the year. Compare the flexible and master (static) budgets and prepare a schedule showing the sales volume variance. Compare the actual results and the flexible budget, and prepare a schedule showing the flexible budget variance. Subdivide the flexible budget variances into the appropriate price (also called rate or spending) variances and efficiency (also called usage or quantity) variances for materials, labor, and variable overhead.

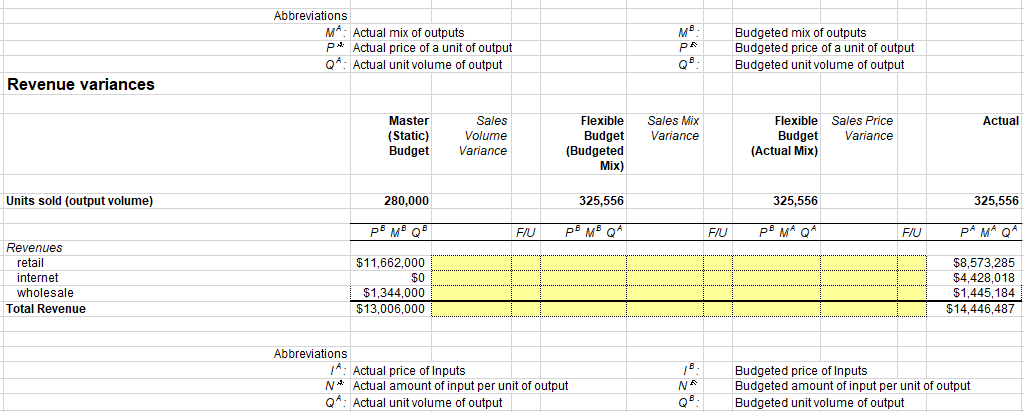

(Hint: for the sales revenue categories shown in Table 1, prepare a flexible budget based on actual units sold multiplied by the master (static) budget prices. For Internet sales, use a revised budget price of $42. To analyze sales volume effects, also prepare a second flexible budget for the sales revenue categories based on the total of 325,556 units sold, multiplied by the budgeted mix (85 percent for retail, 0 percent for Internet, and 15 percent for wholesale). Multiply these quantities by the respective budgeted sales prices. The difference between the two flexible budget amounts is generally termed a sales mix variance, which quantifies the effect on income that results because the actual mix of distribution channels deviates from the budgeted mix. A comparison between the master (static) budget and the flexible budget prepared on the basis of the budgeted mix is the sales volume variance. This variance measures the effect on operating income of selling more or fewer units than planned. The net of the sales mix variance and the sales volume variance equals the sales activity variance.)

- Compute the bonuses earned in fiscal 1998, if any, by David Hall of the purchasing department, Rita Smith of the marketing department, and Bill Wilford of the production department.

(P.S. the highlighted columns is what i have to solve for)

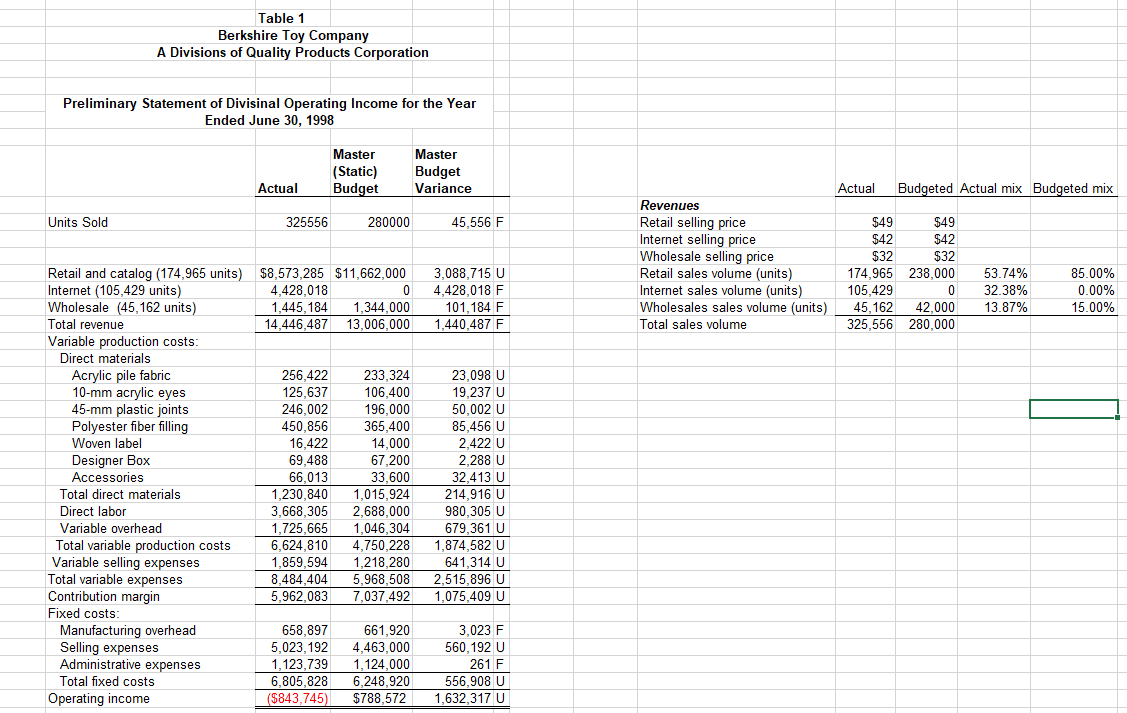

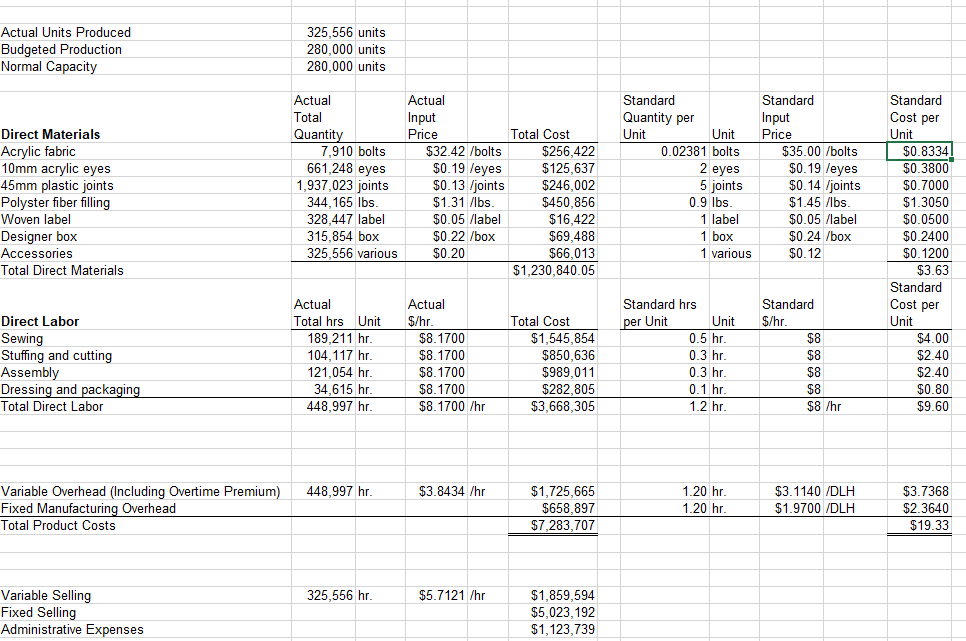

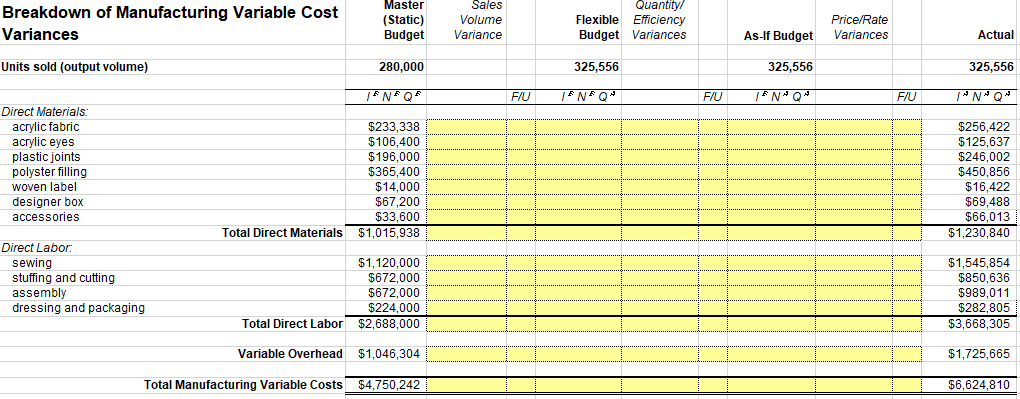

Table 1 Berkshire Toy Company A Divisions of Quality Products Corporation Preliminary Statement of Divisinal Operating Income for the Year Ended June 30, 1998 Master (Static) Budget Master Budget Variance Actual Actual Budgeted Actual mix Budgeted mix Units Sold 325556 280000 45,556 F $8,573,285 $11,662,000 4,428,018 0 1,445,184 1,344,000 14,446,487 13,006,000 3,088,715 U 4,428,018 F 101,184 F 1,440,487 F Revenues Retail selling price Internet selling price Wholesale selling price Retail sales volume (units) Internet sales volume (units) Wholesales sales volume (units) Total sales volume $49 $49 $42 $42 $32 $32 174.965 238,000 105,429 0 45.162 42.000 325,556 280,000 53.74% 32.38% 13.87% 85.00% 0.00% 15.00% Retail and catalog (174,965 units) Internet (105,429 units) Wholesale (45,162 units) Total revenue Variable production costs: Direct materials Acrylic pile fabric 10-mm acrylic eyes 45-mm plastic joints Polyester fiber filling Woven label Designer Box Accessories Total direct materials Direct labor Variable overhead Total variable production costs Variable selling expenses Total variable expenses Contribution margin Fixed costs: Manufacturing overhead Selling expenses Administrative expenses Total fixed costs Operating income 256,422 125,637 246,002 450,856 16,422 69.488 66,013 1,230,840 3,668,305 1.725,665 6,624,810 1,859,594 8,484.404 5,962,083 233,324 106,400 196,000 365,400 14,000 67,200 33,600 1,015,924 2,688,000 1,046,304 4,750,228 1,218,280 5,968,508 7,037,492 23,098 U 19,237 U 50,002 U 85,456 U 2,422 U 2,288 U 32,413 U 214,916 U 980,305 U 679,361 U 1,874,582 U 641,314 U 2,515,896 U 1,075,409 U 658.897 5,023,192 1,123,739 6,805,828 ($843,745) 661,920 4,463,000 1,124.000 6,248,920 $788,572 3,023 F 560.192 U 261 F 556,908 U 1,632,317 U Actual Units Produced Budgeted Production Normal Capacity 325,556 units 280,000 units 280,000 units Actual Total Quantity 7,910 bolts 661,248 eyes 1,937,023 joints 344,165 lbs 328,447 label 315,854 box 325,556 various Standard Quantity per Unit Unit 0.02381 bolts 2 eyes Direct Materials Acrylic fabric 10mm acrylic eyes 45mm plastic joints Polyster fiber filling Woven label Designer box Accessories Total Direct Materials Actual Input Price Total Cost $32.42 /bolts $256,422 $0.19 /eyes $125,637 $0.13 /joints $246,002 $1.31 /bs $450,856 $0.05 /label $16,422 $0.22 /box $69,488 $0.20 $66,013 $1,230,840.05 Standard Input Price $35.00 /bolts $0.19 /eyes $0.14 /joints $1.45 lbs. $0.05 /label $0.24 /box $0.12 5 joints Standard Cost per Unit $0.8334 $0.3800 $0.7000 $1.3050 $0.0500 $0.2400 $0.1200 $3.63 Standard 0.9 lbs 1 label 1 box 1 various Cost per Direct Labor Sewing Stuffing and cutting Assembly Dressing and packaging Total Direct Labor Actual Total hrs Unit 189,211 hr. 104,117 hr. 121,054 hr. 34,615 hr. 448,997 hr. Actual $/hr $8.1700 $8.1700 $8.1700 $8.1700 $8.1700 /hr Total Cost $1,545,854 $850,636 $989,011 $282,805 $3,668,305 Standard hrs per Unit Unit 0.5 hr. 0.3 hr. 0.3 hr. 0.1 hr. 1.2 hr. Standard $/hr. $8 $8 $8 $8 $8/hr Unit $4.00 $2.40 $2.40 $0.80 $9.60 448,997 hr. $3.8434 /hr Variable Overhead (Including Overtime Premium) Fixed Manufacturing Overhead Total Product Costs $1,725,665 $658,897 $7,283,707 1.20 hr. 1.20 hr. $3.1140 /DLH $1.9700 /DLH $3.7368 $2.3640 $19.33 325,556 hr. $5.7121 /hr Variable Selling Fixed Selling Administrative Expenses $1,859,594 $5,023,192 $1,123,739 Abbreviations MA. Actual mix of outputs p* Actual price of a unit of output Actual unit volume of output MB PA Budgeted mix of outputs Budgeted price of a unit of output Budgeted unit volume of output Revenue variances Actual Master (Static) Budget Sales Volume Variance Flexible Budget (Budgeted Mix) Sales Mix Variance Flexible Sales Price Budget Variance (Actual Mix) Units sold (output volume) 280,000 325,556 325,556 325,556 PB MQ FIU PB MQ FIU P8 MAQ" FIU PA MA QA Revenues retail internet wholesale Total Revenue $11,662,000 $0 $1,344,000 $13,006,000 $8,573,285 $4,428,018 $1,445,184 $14,446,487 Abbreviations 14. Actual price of Inputs N* Actual amount of input per unit of output Q : Actual unit volume of output NA 0 Budgeted price of Inputs Budgeted amount of input per unit of output Budgeted unit volume of output Master (Static) Budget Sales Volume Variance Flexible Flexible Budget Budget Variances Actual Cost Variances Units sold (output volume) 280,000 325,556 325,556 NO FIU INQ FIU N'Q" Direct Materials: acrylic fabric acrylic eyes plastic joints polyster filling woven label designer box accessories $233,338 $106,400 $196,000 $365,400 $14,000 $67,200 $33,600 $1,015,938 $256,422 $125,637 $246,002 $450,856 $16,422 $69,488 $66,013 $1,230,840 Total Direct Materials Direct Labor: sewing stuffing and cutting assembly dressing and packaging $1,120,000 $672,000 $672,000 $224,000 Total Direct Labor $2,688,000 $1,545,854 $850,636 $989,011 $282,805 $3,668,305 Manufacturing Overhead: Variable Overhead Fixed Overhead $1,046,304 $661,920 Total Overhead $1,708,224 $1,725,665 $658,897 $2,384,562 Total Manufacturing Costs $5,412,162 $7,283,707 Period Expenses: Variable Selling Expense Fixed Selling Expenses Fixed Admin. Expenses $1,218,280 $4,463,000 $1,124,000 $6,805,280 (198,214) U 0 0 (198,214) U 1,416,494 4,463,000 1,124,000 4,463,000 (443,100) U (560,192) U 261 F (1,003,031) U $1,859,594 $5,023,192 $1,123,739 $8,006,525 Total Period Expenses Breakdown of Manufacturing Variable Cost Variances Master (Static) Budget Sales Volume Variance Quantity/ Flexible Efficiency Budget Variances As-If Budget Price/Rate Variances Actual Units sold (output volume) 280,000 325,556 325,556 325,556 NO" FIU 1NQ- FIU NON FIU 14NQ Direct Materials: acrylic fabric acrylic eyes plastic joints polyster filling woven label designer box accessories $233,338 $106,400 $196,000 $365,400 $14,000 $67,200 $33,600 Total Direct Materials $1,015,938 $256,422 $125,637 $246,002 $450,856 $16,422 $69,488 $66,013 $1,230,840 Direct Labor: sewing stuffing and cutting assembly dressing and packaging $1,120,000 $672,000 $672.000 $224,000 Total Direct Labor $2,688,000 $1,545,854 $850,636 $989,011 $282,805 $3,668,305 Variable Overhead $1,046,304 $1,725,665 Total Manufacturing Variable Costs $4,750,242 $6,624,810 Table 1 Berkshire Toy Company A Divisions of Quality Products Corporation Preliminary Statement of Divisinal Operating Income for the Year Ended June 30, 1998 Master (Static) Budget Master Budget Variance Actual Actual Budgeted Actual mix Budgeted mix Units Sold 325556 280000 45,556 F $8,573,285 $11,662,000 4,428,018 0 1,445,184 1,344,000 14,446,487 13,006,000 3,088,715 U 4,428,018 F 101,184 F 1,440,487 F Revenues Retail selling price Internet selling price Wholesale selling price Retail sales volume (units) Internet sales volume (units) Wholesales sales volume (units) Total sales volume $49 $49 $42 $42 $32 $32 174.965 238,000 105,429 0 45.162 42.000 325,556 280,000 53.74% 32.38% 13.87% 85.00% 0.00% 15.00% Retail and catalog (174,965 units) Internet (105,429 units) Wholesale (45,162 units) Total revenue Variable production costs: Direct materials Acrylic pile fabric 10-mm acrylic eyes 45-mm plastic joints Polyester fiber filling Woven label Designer Box Accessories Total direct materials Direct labor Variable overhead Total variable production costs Variable selling expenses Total variable expenses Contribution margin Fixed costs: Manufacturing overhead Selling expenses Administrative expenses Total fixed costs Operating income 256,422 125,637 246,002 450,856 16,422 69.488 66,013 1,230,840 3,668,305 1.725,665 6,624,810 1,859,594 8,484.404 5,962,083 233,324 106,400 196,000 365,400 14,000 67,200 33,600 1,015,924 2,688,000 1,046,304 4,750,228 1,218,280 5,968,508 7,037,492 23,098 U 19,237 U 50,002 U 85,456 U 2,422 U 2,288 U 32,413 U 214,916 U 980,305 U 679,361 U 1,874,582 U 641,314 U 2,515,896 U 1,075,409 U 658.897 5,023,192 1,123,739 6,805,828 ($843,745) 661,920 4,463,000 1,124.000 6,248,920 $788,572 3,023 F 560.192 U 261 F 556,908 U 1,632,317 U Actual Units Produced Budgeted Production Normal Capacity 325,556 units 280,000 units 280,000 units Actual Total Quantity 7,910 bolts 661,248 eyes 1,937,023 joints 344,165 lbs 328,447 label 315,854 box 325,556 various Standard Quantity per Unit Unit 0.02381 bolts 2 eyes Direct Materials Acrylic fabric 10mm acrylic eyes 45mm plastic joints Polyster fiber filling Woven label Designer box Accessories Total Direct Materials Actual Input Price Total Cost $32.42 /bolts $256,422 $0.19 /eyes $125,637 $0.13 /joints $246,002 $1.31 /bs $450,856 $0.05 /label $16,422 $0.22 /box $69,488 $0.20 $66,013 $1,230,840.05 Standard Input Price $35.00 /bolts $0.19 /eyes $0.14 /joints $1.45 lbs. $0.05 /label $0.24 /box $0.12 5 joints Standard Cost per Unit $0.8334 $0.3800 $0.7000 $1.3050 $0.0500 $0.2400 $0.1200 $3.63 Standard 0.9 lbs 1 label 1 box 1 various Cost per Direct Labor Sewing Stuffing and cutting Assembly Dressing and packaging Total Direct Labor Actual Total hrs Unit 189,211 hr. 104,117 hr. 121,054 hr. 34,615 hr. 448,997 hr. Actual $/hr $8.1700 $8.1700 $8.1700 $8.1700 $8.1700 /hr Total Cost $1,545,854 $850,636 $989,011 $282,805 $3,668,305 Standard hrs per Unit Unit 0.5 hr. 0.3 hr. 0.3 hr. 0.1 hr. 1.2 hr. Standard $/hr. $8 $8 $8 $8 $8/hr Unit $4.00 $2.40 $2.40 $0.80 $9.60 448,997 hr. $3.8434 /hr Variable Overhead (Including Overtime Premium) Fixed Manufacturing Overhead Total Product Costs $1,725,665 $658,897 $7,283,707 1.20 hr. 1.20 hr. $3.1140 /DLH $1.9700 /DLH $3.7368 $2.3640 $19.33 325,556 hr. $5.7121 /hr Variable Selling Fixed Selling Administrative Expenses $1,859,594 $5,023,192 $1,123,739 Abbreviations MA. Actual mix of outputs p* Actual price of a unit of output Actual unit volume of output MB PA Budgeted mix of outputs Budgeted price of a unit of output Budgeted unit volume of output Revenue variances Actual Master (Static) Budget Sales Volume Variance Flexible Budget (Budgeted Mix) Sales Mix Variance Flexible Sales Price Budget Variance (Actual Mix) Units sold (output volume) 280,000 325,556 325,556 325,556 PB MQ FIU PB MQ FIU P8 MAQ" FIU PA MA QA Revenues retail internet wholesale Total Revenue $11,662,000 $0 $1,344,000 $13,006,000 $8,573,285 $4,428,018 $1,445,184 $14,446,487 Abbreviations 14. Actual price of Inputs N* Actual amount of input per unit of output Q : Actual unit volume of output NA 0 Budgeted price of Inputs Budgeted amount of input per unit of output Budgeted unit volume of output Master (Static) Budget Sales Volume Variance Flexible Flexible Budget Budget Variances Actual Cost Variances Units sold (output volume) 280,000 325,556 325,556 NO FIU INQ FIU N'Q" Direct Materials: acrylic fabric acrylic eyes plastic joints polyster filling woven label designer box accessories $233,338 $106,400 $196,000 $365,400 $14,000 $67,200 $33,600 $1,015,938 $256,422 $125,637 $246,002 $450,856 $16,422 $69,488 $66,013 $1,230,840 Total Direct Materials Direct Labor: sewing stuffing and cutting assembly dressing and packaging $1,120,000 $672,000 $672,000 $224,000 Total Direct Labor $2,688,000 $1,545,854 $850,636 $989,011 $282,805 $3,668,305 Manufacturing Overhead: Variable Overhead Fixed Overhead $1,046,304 $661,920 Total Overhead $1,708,224 $1,725,665 $658,897 $2,384,562 Total Manufacturing Costs $5,412,162 $7,283,707 Period Expenses: Variable Selling Expense Fixed Selling Expenses Fixed Admin. Expenses $1,218,280 $4,463,000 $1,124,000 $6,805,280 (198,214) U 0 0 (198,214) U 1,416,494 4,463,000 1,124,000 4,463,000 (443,100) U (560,192) U 261 F (1,003,031) U $1,859,594 $5,023,192 $1,123,739 $8,006,525 Total Period Expenses Breakdown of Manufacturing Variable Cost Variances Master (Static) Budget Sales Volume Variance Quantity/ Flexible Efficiency Budget Variances As-If Budget Price/Rate Variances Actual Units sold (output volume) 280,000 325,556 325,556 325,556 NO" FIU 1NQ- FIU NON FIU 14NQ Direct Materials: acrylic fabric acrylic eyes plastic joints polyster filling woven label designer box accessories $233,338 $106,400 $196,000 $365,400 $14,000 $67,200 $33,600 Total Direct Materials $1,015,938 $256,422 $125,637 $246,002 $450,856 $16,422 $69,488 $66,013 $1,230,840 Direct Labor: sewing stuffing and cutting assembly dressing and packaging $1,120,000 $672,000 $672.000 $224,000 Total Direct Labor $2,688,000 $1,545,854 $850,636 $989,011 $282,805 $3,668,305 Variable Overhead $1,046,304 $1,725,665 Total Manufacturing Variable Costs $4,750,242 $6,624,810Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting Practice And Principles

Authors: Jan Bebbington, M. Richard Laughlin, Robert H. Gray, Gray Dave

3rd Edition

1861527713, 978-1861527714