Answered step by step

Verified Expert Solution

Question

1 Approved Answer

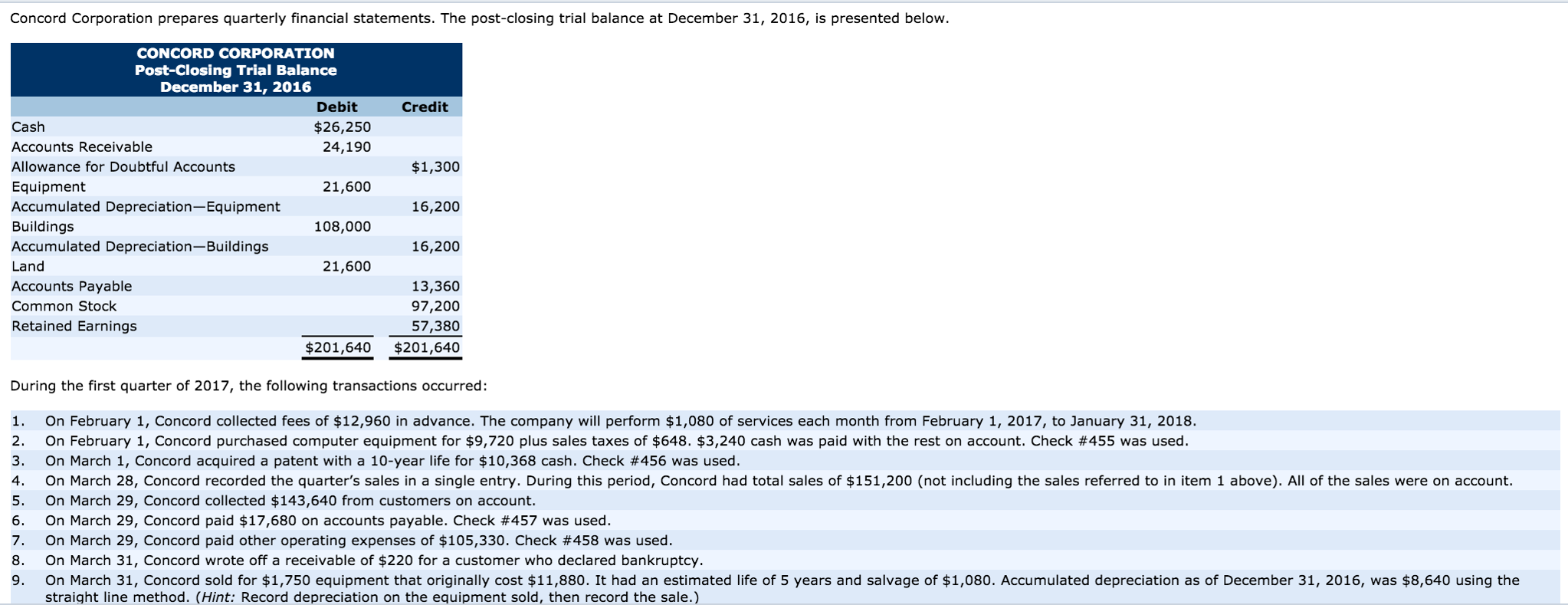

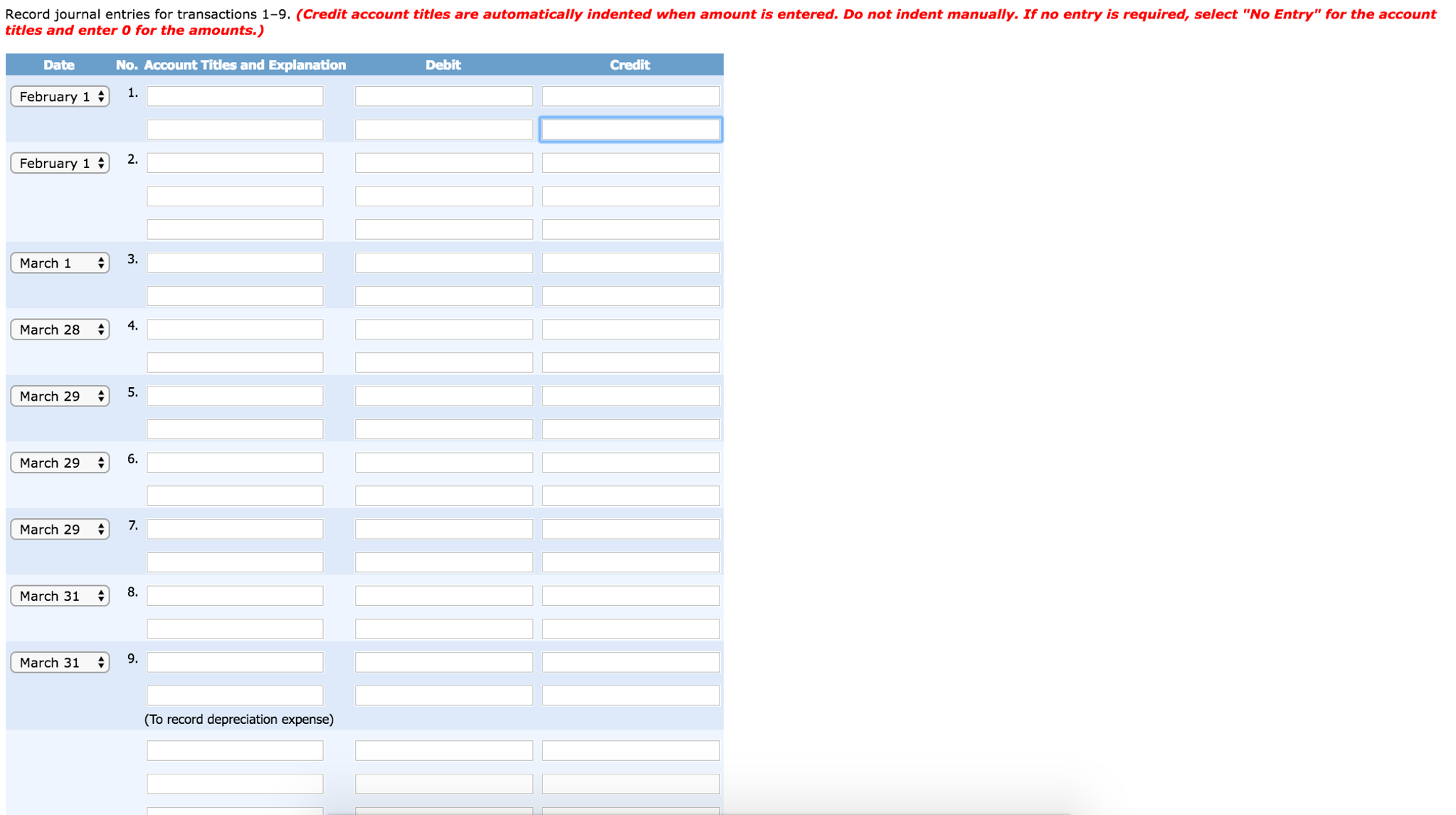

Record Journal Entries for the following 1-9 transactions. (NOTE: March 31 has 6 blanks to be filled - it got cut off). Concord Corporation prepares

Record Journal Entries for the following 1-9 transactions.

(NOTE: March 31 has 6 blanks to be filled - it got cut off).

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Principles

Authors: Jerry J. Weygandt, Paul D. Kimmel, Donald E. Kieso

10th Edition

1119491630, 978-1119491637, 978-0470534793