Answered step by step

Verified Expert Solution

Question

1 Approved Answer

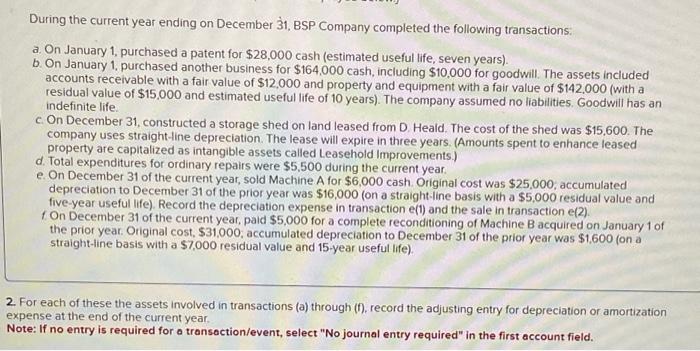

Record the adjusting entry for depreciation or amortization expense for transaction a through f During the current year ending on December 31, BSP Company completed

Record the adjusting entry for depreciation or amortization expense for transaction a through f

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

External Quality Audit Has It Improved Quality Assurance In Universities

Authors: Mahsood Shah, Chenicheri Sid Nair

1st Edition

1843346761, 978-1843346760