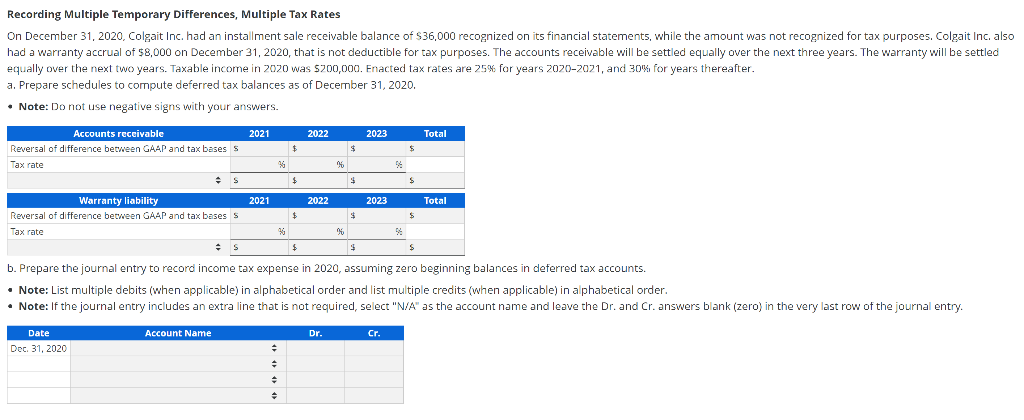

Recording Multiple Temporary Differences, Multiple Tax Rates On December 31, 2020, Colgait Inc. had an installment sale receivable balance of $36,000 recognized on its financial statements, while the amount was not recognized for tax purposes. Colgait Inc also had a warranty accrual of $8,000 on December 31, 2020, that is not deductible for tax purposes. The accounts receivable will be settled equally over the next three years. The warranty will be settled equally over the next two years. Taxable income in 2020 was $200,000. Enacted tax rates are 25% for years 2020-2021, and 30% for years thereafter. a. Prepare schedules to compute deferred tax balances as of December 31, 2020. Note: Do not use negative signs with your answers. 2021 2022 2023 Total Accounts receivable Reversal of difference between GAAP and tax bases s Tax rate $ $ 14 $ $ 2021 2022 2023 Total Warranty liability Reversal of difference between GAAP and tax bases s Tax rate $ $ $ $ $ b. Prepare the journal entry to record income tax expense in 2020, assuming zero beginning balances in deferred tax accounts. Note: List multiple debits (when applicable) in alphabetical order and list multiple credits (when applicable) in alphabetical order. Note: If the journal entry includes an extra line that is not required, select "N/A" as the account name and leave the Dr. and Cr.answers blank (zero) in the very last row of the journal entry. Account Name Dr. Date Dec 31, 2020 Recording Multiple Temporary Differences, Multiple Tax Rates On December 31, 2020, Colgait Inc. had an installment sale receivable balance of $36,000 recognized on its financial statements, while the amount was not recognized for tax purposes. Colgait Inc also had a warranty accrual of $8,000 on December 31, 2020, that is not deductible for tax purposes. The accounts receivable will be settled equally over the next three years. The warranty will be settled equally over the next two years. Taxable income in 2020 was $200,000. Enacted tax rates are 25% for years 2020-2021, and 30% for years thereafter. a. Prepare schedules to compute deferred tax balances as of December 31, 2020. Note: Do not use negative signs with your answers. 2021 2022 2023 Total Accounts receivable Reversal of difference between GAAP and tax bases s Tax rate $ $ 14 $ $ 2021 2022 2023 Total Warranty liability Reversal of difference between GAAP and tax bases s Tax rate $ $ $ $ $ b. Prepare the journal entry to record income tax expense in 2020, assuming zero beginning balances in deferred tax accounts. Note: List multiple debits (when applicable) in alphabetical order and list multiple credits (when applicable) in alphabetical order. Note: If the journal entry includes an extra line that is not required, select "N/A" as the account name and leave the Dr. and Cr.answers blank (zero) in the very last row of the journal entry. Account Name Dr. Date Dec 31, 2020