Question

Recording Sales with Expected Returns Novelty Inc. developed a new product during the year, and its nancial results follow. To increase acceptance by retailers, Novelty

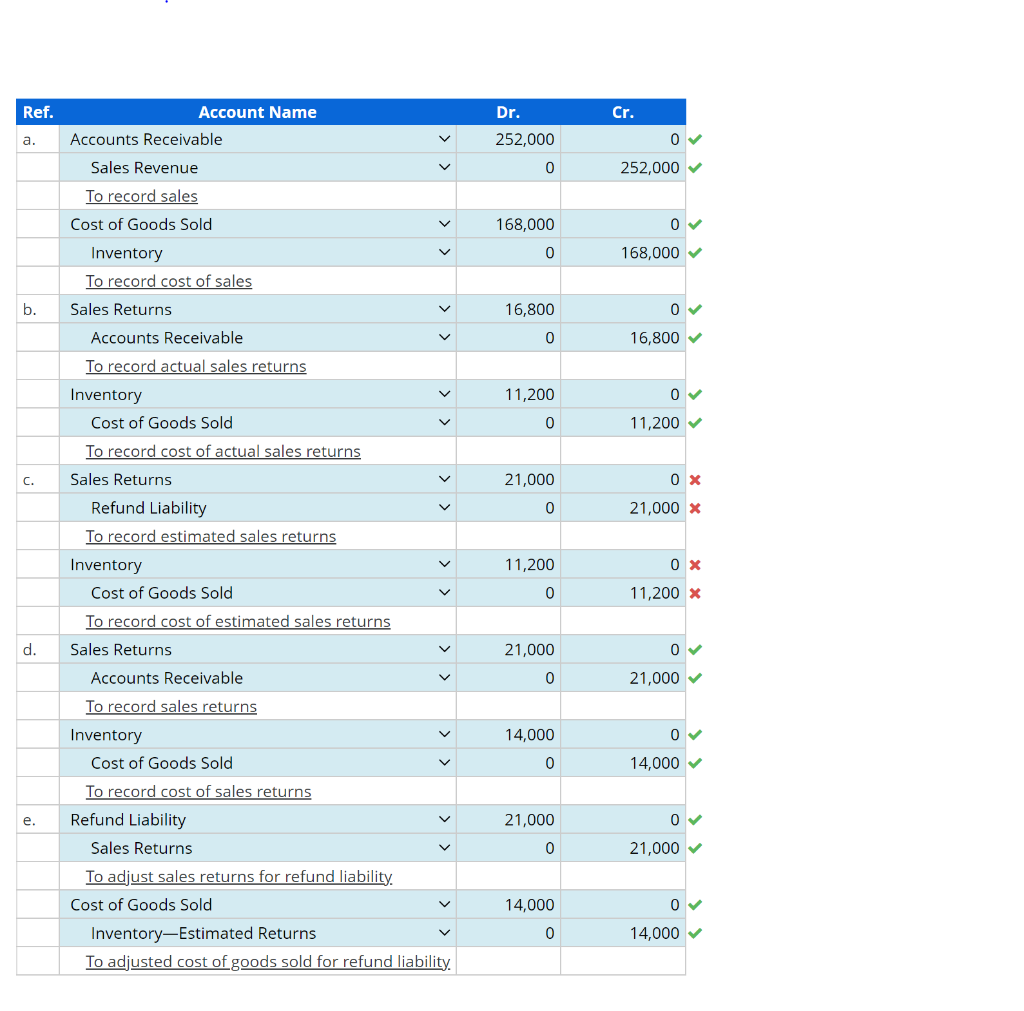

Recording Sales with Expected Returns Novelty Inc. developed a new product during the year, and its nancial results follow. To increase acceptance by retailers, Novelty sold the product to retailers with an unconditional right of return, which expires on February 1 of the next year. Novelty estimates total returns to be 30% of sales, originally made on account. All sales are on credit. Novelty uses the perpetual inventory system.

| Sales in the current year | $252,000 | |

| Cost of goods sold in the current year | 168,000 | |

| Returns of current year sales in the current year | 16,800 | ( cost $11,200 ) |

| Returns of current year sales in January of next year | 21,000 | (cost $14,000 ) |

Required Prepare the following entries, including the sales and cost of goods sold entry for each requirement. a. Prepare the current year sales journal entries. b. Record actual returns in the current year. Assume actual returns are on credit. c. Record estimated returns on December 31 of the current year. d. Record actual returns in January of the next year. Assume actual returns are on credit. e. Record adjusting entries at year end.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting

Authors: Ray H. Garrison, Eric W. Noreen, Peter C. Brewer

13th Edition

978-0073379616, 73379611, 978-0697789938