Answered step by step

Verified Expert Solution

Question

1 Approved Answer

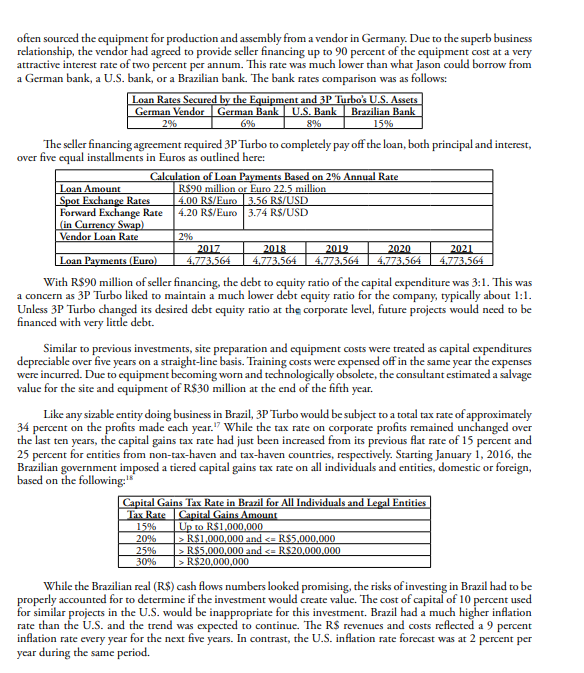

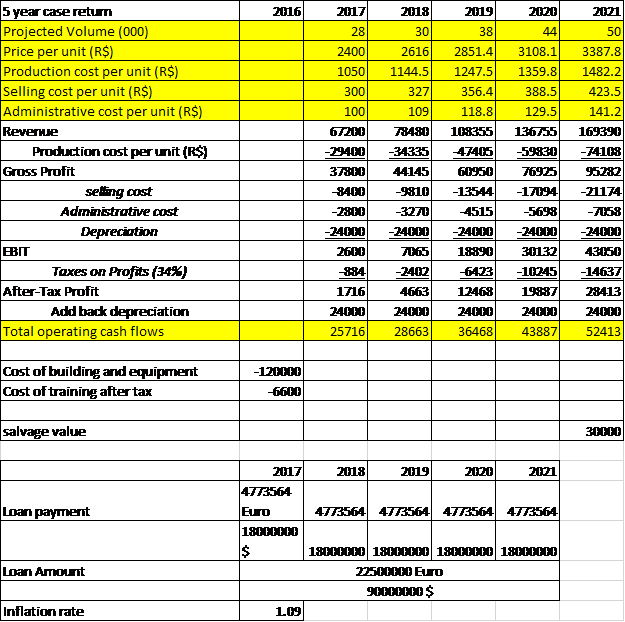

Refer to the cash flows, discuss the reasons why project should consider for investing? often sourced the equipment for production and assembly from a vendor

Refer to the cash flows, discuss the reasons why project should consider for investing?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting principles and analysis

Authors: Terry d. Warfield, jerry j. weygandt, Donald e. kieso

2nd Edition

471737933, 978-0471737933