Question

Relate the following basic principles of insurance to the case entitled The Insurance Claim of Stolen Power Generator: 1) the principle of indemnity 2) the

Relate the following basic principles of insurance to the case entitled The Insurance Claim of Stolen Power Generator:

1) the principle of indemnity

2) the principle of insurable interest

3) the principle of subrogation

*Need more explanation to relate the following principles to the case study not the definitions of the principles*

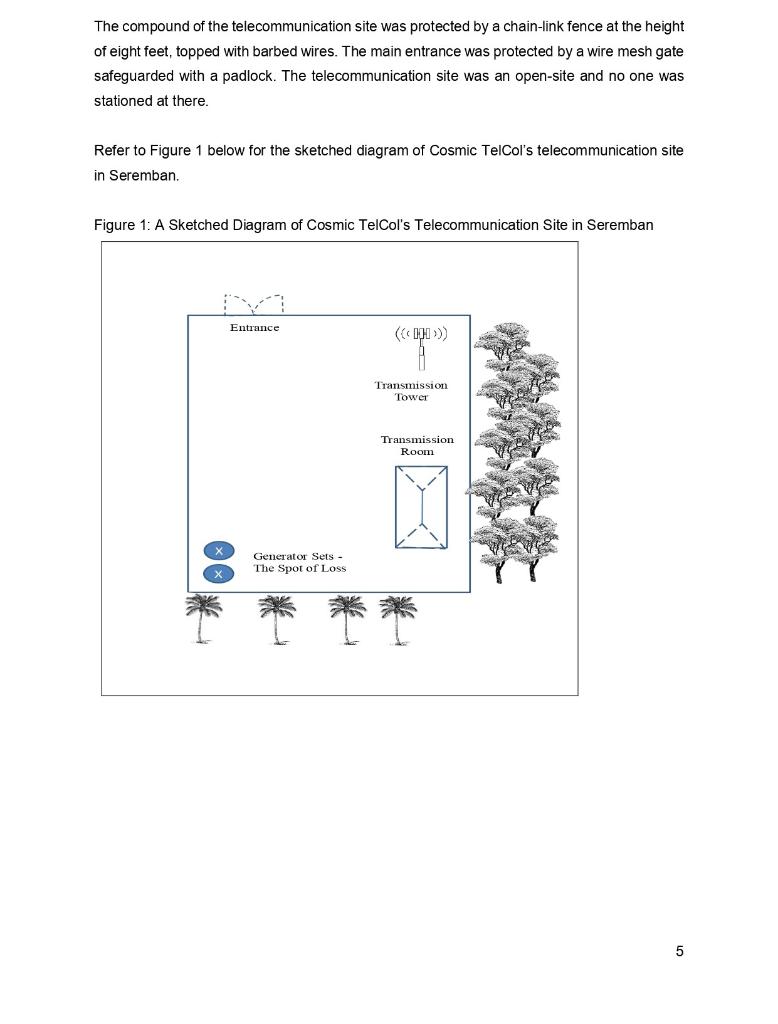

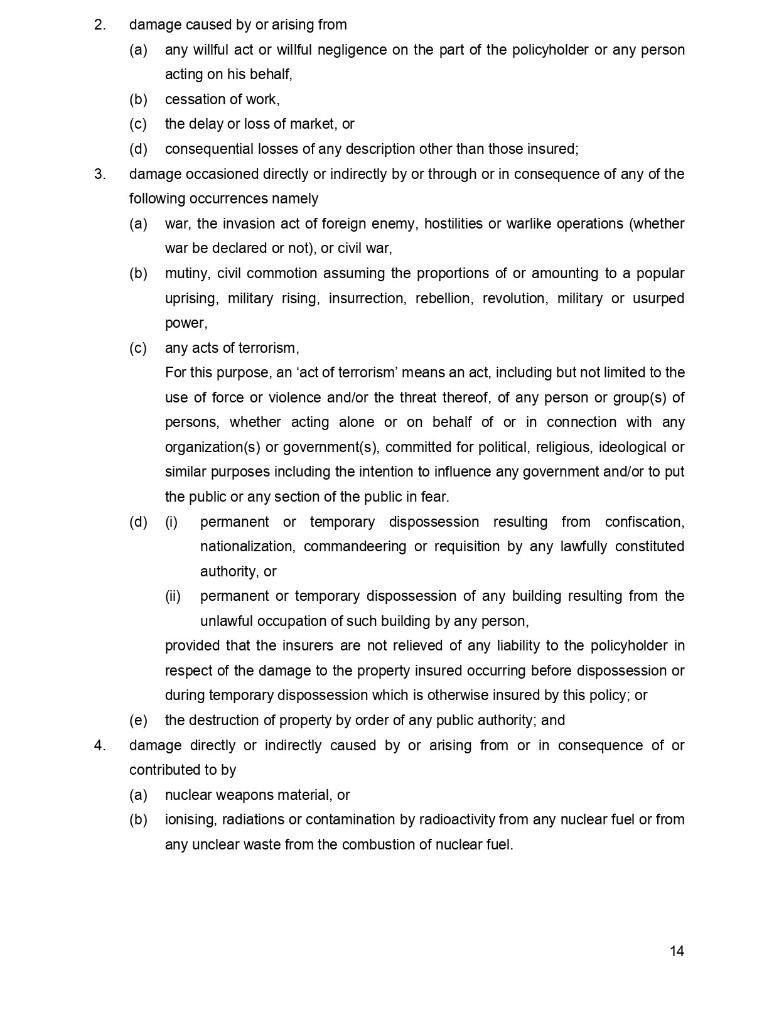

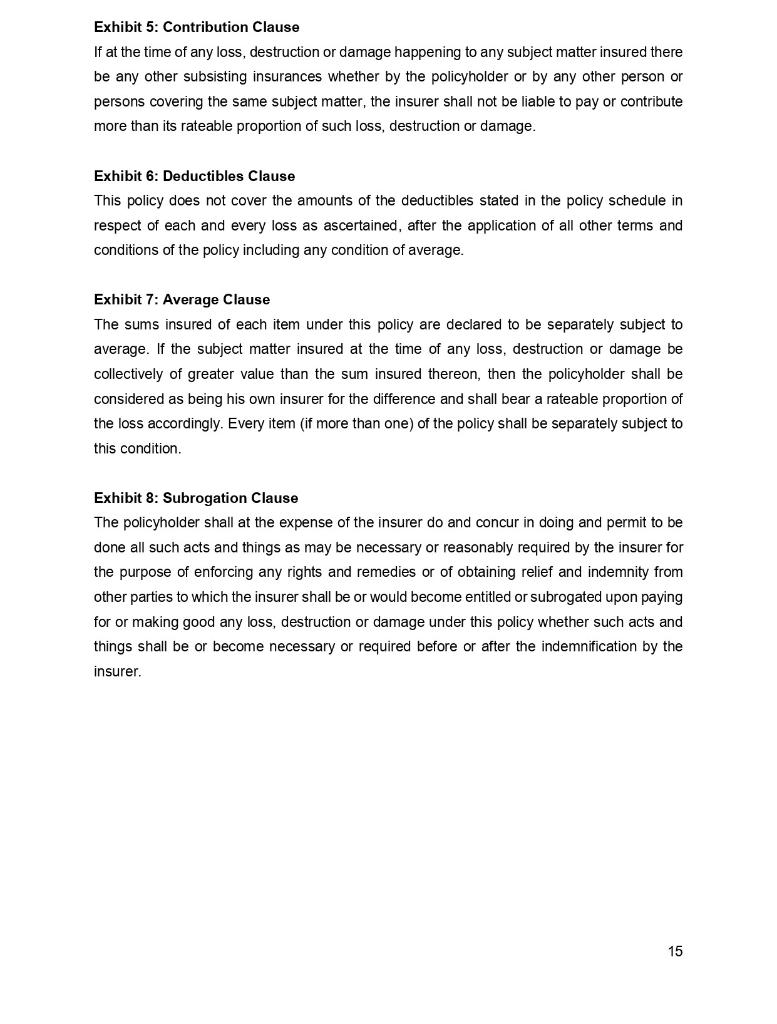

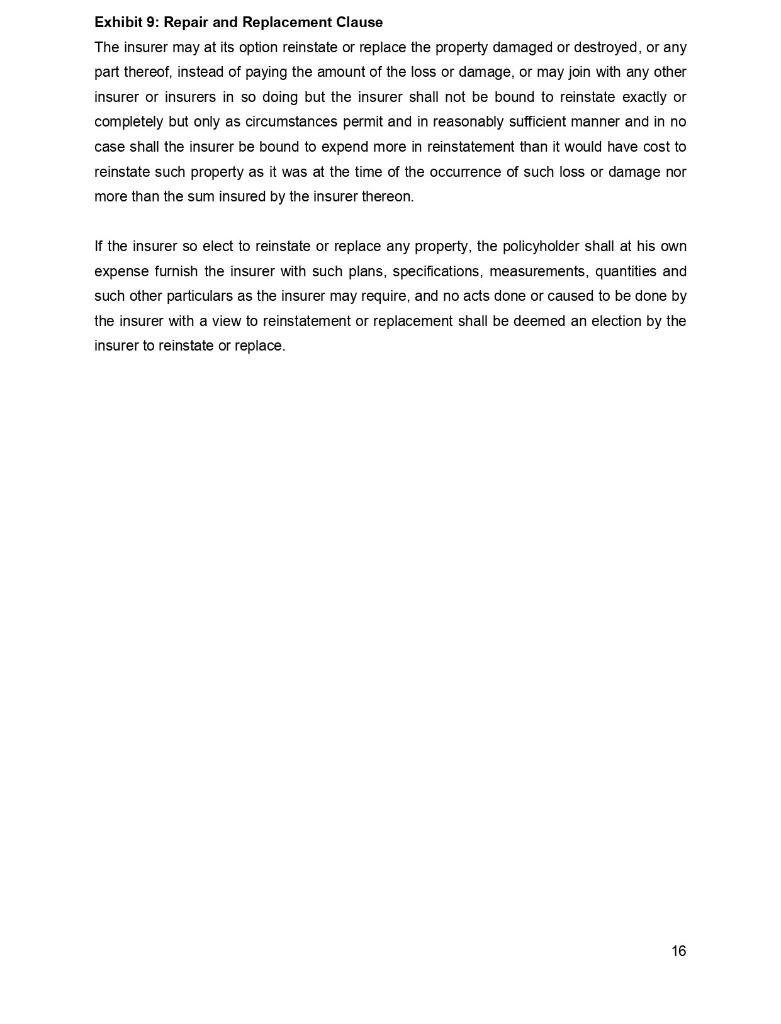

Decision on the Insurance Claim of a Stolen Power Generator On 15 March 2012, Azizan, the claim manager of Universal Takaful Berhad (Universal Takaful), was scrutinizing an investigation report prepared by an independent loss adjuster (Asiatic Adjuster Sdn. Bhd.) in his office in Kuala Lumpur. The report was about an industrial all-risks insurance claim of a stolen power generator. The generator was owned by Universal Takaful's policyholder (Classy Tech Machinery Sdn. Bhd.). However, the generator had been leased to a telecommunication company (Cosmic TelCol Sdn. Bhd.) and the loss of the generator occurred at the site of the policyholder's customer. After a close scrutiny of the investigation report provided by the loss adjuster, Azizan had to make a decision whether his insurance company had a liability to pay for the loss experienced by its policyholder. Universal Takaful Berhad (Universal Takaful) Universal Takaful was a pioneer in Islamic insurance in Malaysia. Its main business operations were family and general Takaful business, whilst the main business operations of its subsidiaries were family and general re-Takaful business and investment holding. The business models of Universal Takaful adhered to Syariah laws, which were according to the Islamic principles of al-Takaful and al-mudharabah. Universal Takaful was incorporated in 1984. The company was subsequently transformed into a public limited company listed on the main board of the stock exchange of Malaysia in 1996. At the end of 2003 , after undergoing a corporate restructuring exercise, Universal Takaful's capital increased significantly. Its authorised capital was raised to RM500 million and its paidup capital stood at RM162.817 million. Asiatic Adjuster Sdn. Bhd. (Asiatic Adjuster) Asiatic Adjuster was a loss adjusting firm established in 1987. The company was licensed by the central bank of Malaysia (Bank Negara Malaysia) and the Ministry of Internal Security and Home Affairs. The headquarter office of Asiatic Adjuster was located at Wangsa Maju, Kuala Lumpur. It had nine branches throughout Malaysia with a total of 40 loss adjusters and support employees serving 10 local insurance companies and Takaful operators. Asiatic Adjuster was a family-based business founded and run by a father-and-daughter team. The father was a former police officer whilst his daughter was a graduate from a local university with academic qualifications in risk management and insurance. Over the years since its inception, Asiatic Adjuster had built up its reputations as an expert in theft and road accident investigations as well as in loss adjustments of fraud and fire insurance claims. As a loss adjuster, Asiatic Adjuster was a professional representing the insurance company in settling claims. Its main roles were to gather facts related to an insurance claim and then to negotiate a settlement. Its tasks usually involved reviewing insurance contract and fact-finding in determining the actual value of loss. In the process of fact-finding, a loss adjuster would obtain information from relevant documents such as quotations (for price estimates), property valuation reports and police reports. The loss adjuster would also talk to people involved in the loss such as the policyholder, witness (if any) and police personnel. All these tasks were performed to ensure that the information gathered from the various parties matched with the descriptions of the incident and to determine whether a claim payment was warranted. Based on its investigation, the loss adjustor compiled information, which might include photographs or sketches, written statements, recorded statements and documents provided by the claimant, in a written report. In the report, the loss adjuster would also put forward its recommendations so that insurance company could evaluate the merits of the loss and make important decisions related to the insurance claim. Classy Tech Machinery Sdn. Bhd. (Classy Tech Machinery) Classy Tech Machinery was established in 1990. The company's principal business activities were supplying and renting machineries, mainly power generators, to corporate clients in the industrial and commercial sectors. Other than power generators, machineries such as air compressors and welding equipment were also available for renting. Meanwhile, the principal business activities of its subsidiaries were providing other complementary services such as transportation and crane services and the use of forklifts for its clients. Classy Tech Machinery's business had experienced rapid growth and expansion. As such, the company started to set up its own task force of service team by equipping its employees with specialised skills to serve the various needs of its clients. Classy Tech Machinery also had an extensive network of parts and service dealers in strategic locations throughout Malaysia (including Sabah and Sarawak). This dealer network had further enhanced the company's ability to provide after sales support activities to its clients. Classy Tech Machinery had a collection of different types of machineries, especially the stocks of power generators with varying capacities ranging from 5KVA to 1250KVA to serve the different power requirements of its clients, and a sound record of after sales support activities, so the company had a voluminous and diverse portfolio of clients. Over the years, the company had built up its reputations as an excellent after sales service provider in the industry. This had prompted the company to increase even more stocks of power generators, air compressors and welding equipment, not just in terms of number but also in terms of a wide array of branded and quality models. Cosmic TelCol Sdn. Bhd. (Cosmic TelCol) Cosmic TelCol was one of the leading telecommunication service providers in Malaysia. It was granted licences in 1993 to provide mobile, fixed-line and international gateway telecommunication services. Its clienteles consisted of both home and business customers. Cosmic TelCol operated actively in four major segments: (a) mobile services, e.g. postpaid mobile, prepaid mobile, mobile data, broadband and roaming services; (b) enterprise fixed services, e.g. a suite of voice services, data services, very small aperture terminal services and internet protocol (IP), and managed services for business customers; (c) international gateway services, e.g. services to international telecommunication carriers for termination of traffic into Malaysia, services to send its own international traffic abroad and bandwidth leasing services; and (d) home services, e.g. fixed voice services and data services to home customers. Cosmic TelCol's Telecommunication Site in Seremban Cosmic TelCol's telecommunication site in Seremban was located at a higher ground in an isolated area. The lands to its left and behind were not developed and surrounded by trees. At the left, the land was packed with massively overgrown trees. At the back, the land was filled with rows of coconut trees. A transmission tower and a transmission room were erected at the left of the enclosed area of the telecommunication site, parallel with the massively overgrown trees. The transmission tower was located at the front and the transmission room was located behind the tower towards the back of the site near the fence, where rows of coconut trees appeared immediately outside of the fence. The transmission room was installed with an alarm system which was directly connected to Cosmic TelCol's office. The alarm would be set off when the electricity supply was found faulty, or when the transmission room was encroached. At this time, Cosmic TelCol's office would be alerted automatically so that prompt actions could be taken to find out what had happened at the telecommunication site. 4 The compound of the telecommunication site was protected by a chain-link fence at the height of eight feet, topped with barbed wires. The main entrance was protected by a wire mesh gate safeguarded with a padlock. The telecommunication site was an open-site and no one was stationed at there. Refer to Figure 1 below for the sketched diagram of Cosmic TelCol's telecommunication site in Seremban. Classy Tech Machinery agreed to lease two power generators of 20KVA and to provide maintenance service twice weekly to Cosmic TelCol for three years starting 1 January 2011. As such two power generators were delivered to Cosmic TelCol's telecommunication site in Seremban. They were soundproof re-conditioned power generators and both were operated on diesel. The two generators were placed in the compound of the customer's telecommunication site and they were being welded to the iron anchors on a concrete slab beside the transmission room to make them difficult to be removed. The two power generators switched operation twice weekly for maintenance purpose, so only one generator was in use at a time to provide electricity supply to the digital equipment in the transmission room. Classy Tech Machinery had insurance coverage for the two power generators, each from a different insurance company. The power generator of model Nissha NES55SM bearing the engine number of W04D-TA10511 was insured for RM16,500 with Universal Takaful. Classy Tech Machinery had purchased this generator from 5-Star Technology Sdn. Bhd. on 24 October 2009 at the price of RM20,500 but the information about its year of manufacture was not available. The insurance coverage of another power generator was provided by Nasional Takaful Bhd. The Incident of Missing Power Generators According to the loss adjuster's investigation report, the incident of missing power generators at Cosmic TelCol's telecommunication site in Seremban occurred on 24 February 2012. At about 5.10 p.m., when the alarm at the telecommunication site was being set off, it alerted Cosmic TelCol and prompted the company to make an emergency call to Classy Tech Machinery. The manager of Classy Tech Machinery immediately instructed a technician to perform an inspection at the telecommunication site to find out what had happened. Upon arrival at the site at about 6.45 p.m., the technician discovered that the main gate to the transmission tower was partly opened, the padlock chain was cut and two power generators secured at the concrete slab beside the transmission room had gone missing. (Refer to Figure1 for the sketched diagram showing the scene of loss at the time of discovery at Cosmic TelCol's telecommunication site in Seremban.) The technician informed his manager of his discovery at the telecommunication site. Classy Tech Machinery took immediate action to replace the two missing power generators for its customer on the same day so that Cosmic TelCol could restore electricity supply to its digital equipment in the transmission room at the site. On the following day, at about 12.36 p.m., the technician lodged a police report on the two missing power generators at Seremban police station. After lodging the police report, Classy Tech Machinery notified the two insurance companies insuring the two missing power generators seeking for compensation for the loss that had happened. (Refer to Exhibit-1 for 'conditions on claims' contained in the policyholder's industrial all-risks insurance policy.) Police Findings Based on the circumstances of the case and the evidence gathered at the scene of loss, the police believed that the perpetrators had come to the site and cut the padlock chain at the gate to go into the enclosed area of the telecommunication site of Cosmic TelCol in Seremban. After successfully removing the two power generators from the concrete slab, the perpetrators then used a mobile crane to lift the generators onto a lorry and fled the scene. As no one was stationed at the telecommunication site, the police believed that the theft could have taken place in broad daylight after the perpetrators managed to gain entry into the site where the generators were located. At the time when the investigation report was prepared by the loss adjuster, the police had not managed to arrest any suspects or recover the missing power generators. However, the police Short Form Services Agreement The lease contract which was the rental agreement of the two power generators between the lessor (Classy Tech Machinery) and the lessee (Cosmic TelCol) was referred to as 'short form services agreement'. The loss adjuster's investigation report highlighted that two clauses in the short form services agreement required special attention to their interpretation. The two clauses were item-13 and item-15: (a) The clause in item-13 stated that lessor could hold lessee responsible for a loss, if the loss was due to lessee's negligence. (b) The clause in item-15 stated that lessor should arrange and insure the equipment on lease. Industrial All-Risks Insurance Policy The missing power generator of model Nissha NES55SM bearing the engine number of W04D-TA10511 was insured under an industrial all-risks insurance for RM16,500 by Universal Takaful. The insuring period was from 11/03/2011 to 10/03/2012 and the insurance coverage was subject to Takaful contribution warranty. (Refer to Exhibit-2 for 'premium warranty clause' contained in the policyholder's industrial all-risks insurance policy.) Under industrial all-risks insurance, the insurance company agreed to provide coverage for losses other than those losses resulting from an excluded cause specified in the policy provided that at the time of the happening of the loss, the insurance covering the interest of the insured equipment shall be in force. (Refer to Exhibit-3 for 'insuring clause' and Exhibit-4 for 'clauses on excluded causes' contained in the policyholder's industrial all-risks insurance policy.) A thorough review of Classy Tech Machinery's industrial all-risks insurance policy by the loss adjuster revealed that there were no other parties having an interest in the insured power generator being stated in the insurance policy. There was also no other insurance providing similar coverage on the insured power generator. However, it was noted that a claim would be subject to an excess of RM1,500 on each and every loss. (Refer to Exhibit-5 for 'contribution clause' and Exhibit-6 for 'deductible clause' contained in the policyholder's industrial all-risks insurance policy.) 8 Another two important clauses contained in the policyholder's industrial all-risks insurance policy were clauses related to 'average' and 'subrogation'. The former was a co-insurance clause that required the policyholder to purchase insurance for a stipulated portion of the entire value of the property insured. The latter was an assignment or substitution clause that allowed the insurance company to step into the rights of the policyholder who had been indemnified by the insurance company. (Refer to Exhibit-7 for 'average clause' and Exhibit-8 for 'subrogation clause' contained in the policyholder's industrial all-risks insurance policy.) In claim settlement, the insurance company had the option of either to make cash payment, to reinstate or to replace the lost, damaged or destroyed equipment. (Refer to Exhibit-9 for 'repair and replacement clause' contained in the policyholder's industrial all-risks insurance policy.) Previous Claim Experience This was not the first incident Classy Tech Machinery's power generators had been stolen. The investigation of the loss adjuster showed that Classy Tech Machinery had experienced similar losses in the past with three other insurance companies, namely Tokio Marine Insurans (M) Berhad, Zurich Insurance Bhd and Allianz General Insurance Malaysia Bhd. Price Estimate for Power Generator Classy Tech Machinery had purchased two power generators from Century Machinery Sdn. Bhd. on 24 February 2012 in order to replace the missing power generators at its customer's telecommunication site in Seremban. The policyholder had forwarded the quotation and the purchase invoice to Universal Takaful to facilitate its insurance claim. On the other hand, Asiatic Adjuster had approached several dealers in a market survey it conducted to find out the price estimate of power generator. According to the dealers, the market price of a re-conditioned power generator similar in make and model as that of the missing power generator at the time of loss was in the range from RM19,000 to RM20,000. The price of a re-conditioned power generator was in fact higher now than in the past. Is Universal Takaful Berhad Liable to Pay the Insurance Claim? The claim manager of Universal Takaful, Azizan, had spent the whole morning carefully studying the investigation report provided by Asiatic Adjuster. Azizan had been able to make a comprehensive assessment on the validity of the insurance claim of Classy Tech Machinery for its stolen power generator insured by Universal Takaful. With the passage of three weeks since the occurrence of the loss, now Azizan could reach a decision whether his insurance company was liable to pay the insurance claim of Classy Tech Machinery to bring this pending case to a closure. The policyholder shall at all times at his own expense produce, procure and give to the insurer all such further particulars, plans, specifications, books, vouchers, invoices, duplicates or copies of documents, proofs and information with respect to the claim, and the origin and cause of the loss or damage, and the circumstances under which the loss or damage occurred, and any matter touching the liability or the amount of liability of the insurer as may be reasonably required by or on behalf of the insurer together with a declaration on oath in other legal form of the truth of the claim and any matters connected therewith. Exhibit 2: Premium Warranty Clause It is a fundamental and absolute special condition of this contract of insurance that the premium due must be paid and received by the insurer within sixty (60) days from the inception date of this policy/endorsement/renewal certificate. If this condition is not complied with, this contract is automatically cancelled and the insurer shall be entitled to the pro rata premium on the period it has been on risk. Where the premium payable pursuant to this warranty is received by an authorised agent of the insurer, the payment shall be deemed to be received by the insurer for the purpose of this warranty and the onus of proving that the premium payable was received by a person, including an insurance agent, who was not authorised to receive such premium shall lie on the insurer. Exhibit 3: Insuring Clause If any of the property insured situated in the premises within the geographical areas of Malaysia and Singapore is accidentally physically lost, destroyed or damaged, other than by an excluded cause, at any time during the period of insurance or any subsequent period in respect of which the policyholder shall have paid and the insurer shall have accepted the premium required for the renewal of the policy, the insurer will pay to the policyholder the actual value of the property at the time of the happening of the damage, or at its option to reinstate or replace such property or any part thereof. Exhibit 4: Clauses on Excluded Causes This policy does not cover 1. damage to the property insured caused by (a) (i) faulty or defective design, materials or workmanship, latent defect, gradual deterioration, deformation or distortion, or wear and tear, (ii) the interruption of water supply, gas, electricity or fuel systems, or the failure of effluent disposal systems to and from the premises, or (iii) the settling or bedding down of structures, shrinkage, or the expansion of foundations, walls, floors or ceilings, unless damaged by a cause not excluded in the policy ensues, then the insurer shall be liable only for such ensuing damage; (b) (i) collapse or cracking of buildings, or (ii) corrosion, rust, extremes or changes in temperature, dampness, dryness, wet or dry rot fungus, shrinkage, evaporation, loss of weight, pollution, contamination, changes in color, flavor, texture or finish, action of light, vermin, insects, marring or scratching, or inherent vice, unless such loss is caused directly by damage to the property insured or to the premises containing such property by a cause not excluded in the policy; (c) (i) theft unless accompanied by violence or threat of violence to persons, or forcible and violent entry to or exit from the premises, (ii) any fraudulent scheme, trick, device or false pretence practised upon the policyholder or upon any person(s) having care of the insured property at such time, (iii) the act of infidelity or acts of dishonesty on the part of the policyholder or any of the employees of the policyholder, (iv) disappearance unexplained or inventory shortage, misfiling or misplacing of information, shortage in supply or delivery of materials, or shortage due to clerical or accounting error, (v) the cracking, fracturing, collapse or overheating of boilers, economizers, vessels, tubes or pipes, nipple leakage, or the failure of the welds of boilers, (vi) mechanical or electrical breakdown, or derangement of machinery or equipment including electronic installations, computers and data processing equipment, (vii) the damage to boilers, economizers, turbines, or other vessels machinery or apparatus in which pressure is used, or their contents resulting from their explosion or rupture, or (viii) bursting, overflowing, discharging or leaking of water tanks, apparatus or pipes when the premises becomes unoccupied and so remains for a period of more than thirty (30) days, unless (I) damaged by a cause not excluded in the policy ensues, then the insurer shall be liable only for such ensuing damage, and/or (II) such loss is caused directly by damage to the property insured or to the premises containing such property by a cause not excluded in the policy; (d) (i) coastal or river erosion, (ii) storm, tempest, water and rain to the property in the open (other than property designed to exist and operate in the open), (iii) freezing, solidification or inadvertent escape of molten or gaseous material, unless a fire ensues, then the insurer shall be liable for such ensuing damage, or (iv) false programming, punching, labeling or inserting, inadvertent cancelling of information or discarding of data media, and the loss of information caused by magnetic fields; 13 2. damage caused by or arising from (a) any willful act or willful negligence on the part of the policyholder or any person acting on his behalf, (b) cessation of work, (c) the delay or loss of market, or (d) consequential losses of any description other than those insured; 3. damage occasioned directly or indirectly by or through or in consequence of any of the following occurrences namely (a) war, the invasion act of foreign enemy, hostilities or warlike operations (whether war be declared or not), or civil war, (b) mutiny, civil commotion assuming the proportions of or amounting to a popular uprising, military rising, insurrection, rebellion, revolution, military or usurped power, (c) any acts of terrorism, For this purpose, an 'act of terrorism' means an act, including but not limited to the use of force or violence and/or the threat thereof, of any person or group(s) of persons, whether acting alone or on behalf of or in connection with any organization(s) or government(s), committed for political, religious, ideological or similar purposes including the intention to influence any government and/or to put the public or any section of the public in fear. (d) (i) permanent or temporary dispossession resulting from confiscation, nationalization, commandeering or requisition by any lawfully constituted authority, or (ii) permanent or temporary dispossession of any building resulting from the unlawful occupation of such building by any person, provided that the insurers are not relieved of any liability to the policyholder in respect of the damage to the property insured occurring before dispossession or during temporary dispossession which is otherwise insured by this policy; or (e) the destruction of property by order of any public authority; and 4. damage directly or indirectly caused by or arising from or in consequence of or contributed to by (a) nuclear weapons material, or (b) ionising, radiations or contamination by radioactivity from any nuclear fuel or from any unclear waste from the combustion of nuclear fuel. Exhibit 5: Contribution Clause If at the time of any loss, destruction or damage happening to any subject matter insured there be any other subsisting insurances whether by the policyholder or by any other person or persons covering the same subject matter, the insurer shall not be liable to pay or contribute more than its rateable proportion of such loss, destruction or damage. Exhibit 6: Deductibles Clause This policy does not cover the amounts of the deductibles stated in the policy schedule in respect of each and every loss as ascertained, after the application of all other terms and conditions of the policy including any condition of average. Exhibit 7: Average Clause The sums insured of each item under this policy are declared to be separately subject to average. If the subject matter insured at the time of any loss, destruction or damage be collectively of greater value than the sum insured thereon, then the policyholder shall be considered as being his own insurer for the difference and shall bear a rateable proportion of the loss accordingly. Every item (if more than one) of the policy shall be separately subject to this condition. Exhibit 8: Subrogation Clause The policyholder shall at the expense of the insurer do and concur in doing and permit to be done all such acts and things as may be necessary or reasonably required by the insurer for the purpose of enforcing any rights and remedies or of obtaining relief and indemnity from other parties to which the insurer shall be or would become entitled or subrogated upon paying for or making good any loss, destruction or damage under this policy whether such acts and things shall be or become necessary or required before or after the indemnification by the insurer. Exhibit 9: Repair and Replacement Clause The insurer may at its option reinstate or replace the property damaged or destroyed, or any part thereof, instead of paying the amount of the loss or damage, or may join with any other insurer or insurers in so doing but the insurer shall not be bound to reinstate exactly or completely but only as circumstances permit and in reasonably sufficient manner and in no case shall the insurer be bound to expend more in reinstatement than it would have cost to reinstate such property as it was at the time of the occurrence of such loss or damage nor more than the sum insured by the insurer thereon. If the insurer so elect to reinstate or replace any property, the policyholder shall at his own expense furnish the insurer with such plans, specifications, measurements, quantities and such other particulars as the insurer may require, and no acts done or caused to be done by the insurer with a view to reinstatement or replacement shall be deemed an election by the insurer to reinstate or replace. Decision on the Insurance Claim of a Stolen Power Generator On 15 March 2012, Azizan, the claim manager of Universal Takaful Berhad (Universal Takaful), was scrutinizing an investigation report prepared by an independent loss adjuster (Asiatic Adjuster Sdn. Bhd.) in his office in Kuala Lumpur. The report was about an industrial all-risks insurance claim of a stolen power generator. The generator was owned by Universal Takaful's policyholder (Classy Tech Machinery Sdn. Bhd.). However, the generator had been leased to a telecommunication company (Cosmic TelCol Sdn. Bhd.) and the loss of the generator occurred at the site of the policyholder's customer. After a close scrutiny of the investigation report provided by the loss adjuster, Azizan had to make a decision whether his insurance company had a liability to pay for the loss experienced by its policyholder. Universal Takaful Berhad (Universal Takaful) Universal Takaful was a pioneer in Islamic insurance in Malaysia. Its main business operations were family and general Takaful business, whilst the main business operations of its subsidiaries were family and general re-Takaful business and investment holding. The business models of Universal Takaful adhered to Syariah laws, which were according to the Islamic principles of al-Takaful and al-mudharabah. Universal Takaful was incorporated in 1984. The company was subsequently transformed into a public limited company listed on the main board of the stock exchange of Malaysia in 1996. At the end of 2003 , after undergoing a corporate restructuring exercise, Universal Takaful's capital increased significantly. Its authorised capital was raised to RM500 million and its paidup capital stood at RM162.817 million. Asiatic Adjuster Sdn. Bhd. (Asiatic Adjuster) Asiatic Adjuster was a loss adjusting firm established in 1987. The company was licensed by the central bank of Malaysia (Bank Negara Malaysia) and the Ministry of Internal Security and Home Affairs. The headquarter office of Asiatic Adjuster was located at Wangsa Maju, Kuala Lumpur. It had nine branches throughout Malaysia with a total of 40 loss adjusters and support employees serving 10 local insurance companies and Takaful operators. Asiatic Adjuster was a family-based business founded and run by a father-and-daughter team. The father was a former police officer whilst his daughter was a graduate from a local university with academic qualifications in risk management and insurance. Over the years since its inception, Asiatic Adjuster had built up its reputations as an expert in theft and road accident investigations as well as in loss adjustments of fraud and fire insurance claims. As a loss adjuster, Asiatic Adjuster was a professional representing the insurance company in settling claims. Its main roles were to gather facts related to an insurance claim and then to negotiate a settlement. Its tasks usually involved reviewing insurance contract and fact-finding in determining the actual value of loss. In the process of fact-finding, a loss adjuster would obtain information from relevant documents such as quotations (for price estimates), property valuation reports and police reports. The loss adjuster would also talk to people involved in the loss such as the policyholder, witness (if any) and police personnel. All these tasks were performed to ensure that the information gathered from the various parties matched with the descriptions of the incident and to determine whether a claim payment was warranted. Based on its investigation, the loss adjustor compiled information, which might include photographs or sketches, written statements, recorded statements and documents provided by the claimant, in a written report. In the report, the loss adjuster would also put forward its recommendations so that insurance company could evaluate the merits of the loss and make important decisions related to the insurance claim. Classy Tech Machinery Sdn. Bhd. (Classy Tech Machinery) Classy Tech Machinery was established in 1990. The company's principal business activities were supplying and renting machineries, mainly power generators, to corporate clients in the industrial and commercial sectors. Other than power generators, machineries such as air compressors and welding equipment were also available for renting. Meanwhile, the principal business activities of its subsidiaries were providing other complementary services such as transportation and crane services and the use of forklifts for its clients. Classy Tech Machinery's business had experienced rapid growth and expansion. As such, the company started to set up its own task force of service team by equipping its employees with specialised skills to serve the various needs of its clients. Classy Tech Machinery also had an extensive network of parts and service dealers in strategic locations throughout Malaysia (including Sabah and Sarawak). This dealer network had further enhanced the company's ability to provide after sales support activities to its clients. Classy Tech Machinery had a collection of different types of machineries, especially the stocks of power generators with varying capacities ranging from 5KVA to 1250KVA to serve the different power requirements of its clients, and a sound record of after sales support activities, so the company had a voluminous and diverse portfolio of clients. Over the years, the company had built up its reputations as an excellent after sales service provider in the industry. This had prompted the company to increase even more stocks of power generators, air compressors and welding equipment, not just in terms of number but also in terms of a wide array of branded and quality models. Cosmic TelCol Sdn. Bhd. (Cosmic TelCol) Cosmic TelCol was one of the leading telecommunication service providers in Malaysia. It was granted licences in 1993 to provide mobile, fixed-line and international gateway telecommunication services. Its clienteles consisted of both home and business customers. Cosmic TelCol operated actively in four major segments: (a) mobile services, e.g. postpaid mobile, prepaid mobile, mobile data, broadband and roaming services; (b) enterprise fixed services, e.g. a suite of voice services, data services, very small aperture terminal services and internet protocol (IP), and managed services for business customers; (c) international gateway services, e.g. services to international telecommunication carriers for termination of traffic into Malaysia, services to send its own international traffic abroad and bandwidth leasing services; and (d) home services, e.g. fixed voice services and data services to home customers. Cosmic TelCol's Telecommunication Site in Seremban Cosmic TelCol's telecommunication site in Seremban was located at a higher ground in an isolated area. The lands to its left and behind were not developed and surrounded by trees. At the left, the land was packed with massively overgrown trees. At the back, the land was filled with rows of coconut trees. A transmission tower and a transmission room were erected at the left of the enclosed area of the telecommunication site, parallel with the massively overgrown trees. The transmission tower was located at the front and the transmission room was located behind the tower towards the back of the site near the fence, where rows of coconut trees appeared immediately outside of the fence. The transmission room was installed with an alarm system which was directly connected to Cosmic TelCol's office. The alarm would be set off when the electricity supply was found faulty, or when the transmission room was encroached. At this time, Cosmic TelCol's office would be alerted automatically so that prompt actions could be taken to find out what had happened at the telecommunication site. 4 The compound of the telecommunication site was protected by a chain-link fence at the height of eight feet, topped with barbed wires. The main entrance was protected by a wire mesh gate safeguarded with a padlock. The telecommunication site was an open-site and no one was stationed at there. Refer to Figure 1 below for the sketched diagram of Cosmic TelCol's telecommunication site in Seremban. Classy Tech Machinery agreed to lease two power generators of 20KVA and to provide maintenance service twice weekly to Cosmic TelCol for three years starting 1 January 2011. As such two power generators were delivered to Cosmic TelCol's telecommunication site in Seremban. They were soundproof re-conditioned power generators and both were operated on diesel. The two generators were placed in the compound of the customer's telecommunication site and they were being welded to the iron anchors on a concrete slab beside the transmission room to make them difficult to be removed. The two power generators switched operation twice weekly for maintenance purpose, so only one generator was in use at a time to provide electricity supply to the digital equipment in the transmission room. Classy Tech Machinery had insurance coverage for the two power generators, each from a different insurance company. The power generator of model Nissha NES55SM bearing the engine number of W04D-TA10511 was insured for RM16,500 with Universal Takaful. Classy Tech Machinery had purchased this generator from 5-Star Technology Sdn. Bhd. on 24 October 2009 at the price of RM20,500 but the information about its year of manufacture was not available. The insurance coverage of another power generator was provided by Nasional Takaful Bhd. The Incident of Missing Power Generators According to the loss adjuster's investigation report, the incident of missing power generators at Cosmic TelCol's telecommunication site in Seremban occurred on 24 February 2012. At about 5.10 p.m., when the alarm at the telecommunication site was being set off, it alerted Cosmic TelCol and prompted the company to make an emergency call to Classy Tech Machinery. The manager of Classy Tech Machinery immediately instructed a technician to perform an inspection at the telecommunication site to find out what had happened. Upon arrival at the site at about 6.45 p.m., the technician discovered that the main gate to the transmission tower was partly opened, the padlock chain was cut and two power generators secured at the concrete slab beside the transmission room had gone missing. (Refer to Figure1 for the sketched diagram showing the scene of loss at the time of discovery at Cosmic TelCol's telecommunication site in Seremban.) The technician informed his manager of his discovery at the telecommunication site. Classy Tech Machinery took immediate action to replace the two missing power generators for its customer on the same day so that Cosmic TelCol could restore electricity supply to its digital equipment in the transmission room at the site. On the following day, at about 12.36 p.m., the technician lodged a police report on the two missing power generators at Seremban police station. After lodging the police report, Classy Tech Machinery notified the two insurance companies insuring the two missing power generators seeking for compensation for the loss that had happened. (Refer to Exhibit-1 for 'conditions on claims' contained in the policyholder's industrial all-risks insurance policy.) Police Findings Based on the circumstances of the case and the evidence gathered at the scene of loss, the police believed that the perpetrators had come to the site and cut the padlock chain at the gate to go into the enclosed area of the telecommunication site of Cosmic TelCol in Seremban. After successfully removing the two power generators from the concrete slab, the perpetrators then used a mobile crane to lift the generators onto a lorry and fled the scene. As no one was stationed at the telecommunication site, the police believed that the theft could have taken place in broad daylight after the perpetrators managed to gain entry into the site where the generators were located. At the time when the investigation report was prepared by the loss adjuster, the police had not managed to arrest any suspects or recover the missing power generators. However, the police Short Form Services Agreement The lease contract which was the rental agreement of the two power generators between the lessor (Classy Tech Machinery) and the lessee (Cosmic TelCol) was referred to as 'short form services agreement'. The loss adjuster's investigation report highlighted that two clauses in the short form services agreement required special attention to their interpretation. The two clauses were item-13 and item-15: (a) The clause in item-13 stated that lessor could hold lessee responsible for a loss, if the loss was due to lessee's negligence. (b) The clause in item-15 stated that lessor should arrange and insure the equipment on lease. Industrial All-Risks Insurance Policy The missing power generator of model Nissha NES55SM bearing the engine number of W04D-TA10511 was insured under an industrial all-risks insurance for RM16,500 by Universal Takaful. The insuring period was from 11/03/2011 to 10/03/2012 and the insurance coverage was subject to Takaful contribution warranty. (Refer to Exhibit-2 for 'premium warranty clause' contained in the policyholder's industrial all-risks insurance policy.) Under industrial all-risks insurance, the insurance company agreed to provide coverage for losses other than those losses resulting from an excluded cause specified in the policy provided that at the time of the happening of the loss, the insurance covering the interest of the insured equipment shall be in force. (Refer to Exhibit-3 for 'insuring clause' and Exhibit-4 for 'clauses on excluded causes' contained in the policyholder's industrial all-risks insurance policy.) A thorough review of Classy Tech Machinery's industrial all-risks insurance policy by the loss adjuster revealed that there were no other parties having an interest in the insured power generator being stated in the insurance policy. There was also no other insurance providing similar coverage on the insured power generator. However, it was noted that a claim would be subject to an excess of RM1,500 on each and every loss. (Refer to Exhibit-5 for 'contribution clause' and Exhibit-6 for 'deductible clause' contained in the policyholder's industrial all-risks insurance policy.) 8 Another two important clauses contained in the policyholder's industrial all-risks insurance policy were clauses related to 'average' and 'subrogation'. The former was a co-insurance clause that required the policyholder to purchase insurance for a stipulated portion of the entire value of the property insured. The latter was an assignment or substitution clause that allowed the insurance company to step into the rights of the policyholder who had been indemnified by the insurance company. (Refer to Exhibit-7 for 'average clause' and Exhibit-8 for 'subrogation clause' contained in the policyholder's industrial all-risks insurance policy.) In claim settlement, the insurance company had the option of either to make cash payment, to reinstate or to replace the lost, damaged or destroyed equipment. (Refer to Exhibit-9 for 'repair and replacement clause' contained in the policyholder's industrial all-risks insurance policy.) Previous Claim Experience This was not the first incident Classy Tech Machinery's power generators had been stolen. The investigation of the loss adjuster showed that Classy Tech Machinery had experienced similar losses in the past with three other insurance companies, namely Tokio Marine Insurans (M) Berhad, Zurich Insurance Bhd and Allianz General Insurance Malaysia Bhd. Price Estimate for Power Generator Classy Tech Machinery had purchased two power generators from Century Machinery Sdn. Bhd. on 24 February 2012 in order to replace the missing power generators at its customer's telecommunication site in Seremban. The policyholder had forwarded the quotation and the purchase invoice to Universal Takaful to facilitate its insurance claim. On the other hand, Asiatic Adjuster had approached several dealers in a market survey it conducted to find out the price estimate of power generator. According to the dealers, the market price of a re-conditioned power generator similar in make and model as that of the missing power generator at the time of loss was in the range from RM19,000 to RM20,000. The price of a re-conditioned power generator was in fact higher now than in the past. Is Universal Takaful Berhad Liable to Pay the Insurance Claim? The claim manager of Universal Takaful, Azizan, had spent the whole morning carefully studying the investigation report provided by Asiatic Adjuster. Azizan had been able to make a comprehensive assessment on the validity of the insurance claim of Classy Tech Machinery for its stolen power generator insured by Universal Takaful. With the passage of three weeks since the occurrence of the loss, now Azizan could reach a decision whether his insurance company was liable to pay the insurance claim of Classy Tech Machinery to bring this pending case to a closure. The policyholder shall at all times at his own expense produce, procure and give to the insurer all such further particulars, plans, specifications, books, vouchers, invoices, duplicates or copies of documents, proofs and information with respect to the claim, and the origin and cause of the loss or damage, and the circumstances under which the loss or damage occurred, and any matter touching the liability or the amount of liability of the insurer as may be reasonably required by or on behalf of the insurer together with a declaration on oath in other legal form of the truth of the claim and any matters connected therewith. Exhibit 2: Premium Warranty Clause It is a fundamental and absolute special condition of this contract of insurance that the premium due must be paid and received by the insurer within sixty (60) days from the inception date of this policy/endorsement/renewal certificate. If this condition is not complied with, this contract is automatically cancelled and the insurer shall be entitled to the pro rata premium on the period it has been on risk. Where the premium payable pursuant to this warranty is received by an authorised agent of the insurer, the payment shall be deemed to be received by the insurer for the purpose of this warranty and the onus of proving that the premium payable was received by a person, including an insurance agent, who was not authorised to receive such premium shall lie on the insurer. Exhibit 3: Insuring Clause If any of the property insured situated in the premises within the geographical areas of Malaysia and Singapore is accidentally physically lost, destroyed or damaged, other than by an excluded cause, at any time during the period of insurance or any subsequent period in respect of which the policyholder shall have paid and the insurer shall have accepted the premium required for the renewal of the policy, the insurer will pay to the policyholder the actual value of the property at the time of the happening of the damage, or at its option to reinstate or replace such property or any part thereof. Exhibit 4: Clauses on Excluded Causes This policy does not cover 1. damage to the property insured caused by (a) (i) faulty or defective design, materials or workmanship, latent defect, gradual deterioration, deformation or distortion, or wear and tear, (ii) the interruption of water supply, gas, electricity or fuel systems, or the failure of effluent disposal systems to and from the premises, or (iii) the settling or bedding down of structures, shrinkage, or the expansion of foundations, walls, floors or ceilings, unless damaged by a cause not excluded in the policy ensues, then the insurer shall be liable only for such ensuing damage; (b) (i) collapse or cracking of buildings, or (ii) corrosion, rust, extremes or changes in temperature, dampness, dryness, wet or dry rot fungus, shrinkage, evaporation, loss of weight, pollution, contamination, changes in color, flavor, texture or finish, action of light, vermin, insects, marring or scratching, or inherent vice, unless such loss is caused directly by damage to the property insured or to the premises containing such property by a cause not excluded in the policy; (c) (i) theft unless accompanied by violence or threat of violence to persons, or forcible and violent entry to or exit from the premises, (ii) any fraudulent scheme, trick, device or false pretence practised upon the policyholder or upon any person(s) having care of the insured property at such time, (iii) the act of infidelity or acts of dishonesty on the part of the policyholder or any of the employees of the policyholder, (iv) disappearance unexplained or inventory shortage, misfiling or misplacing of information, shortage in supply or delivery of materials, or shortage due to clerical or accounting error, (v) the cracking, fracturing, collapse or overheating of boilers, economizers, vessels, tubes or pipes, nipple leakage, or the failure of the welds of boilers, (vi) mechanical or electrical breakdown, or derangement of machinery or equipment including electronic installations, computers and data processing equipment, (vii) the damage to boilers, economizers, turbines, or other vessels machinery or apparatus in which pressure is used, or their contents resulting from their explosion or rupture, or (viii) bursting, overflowing, discharging or leaking of water tanks, apparatus or pipes when the premises becomes unoccupied and so remains for a period of more than thirty (30) days, unless (I) damaged by a cause not excluded in the policy ensues, then the insurer shall be liable only for such ensuing damage, and/or (II) such loss is caused directly by damage to the property insured or to the premises containing such property by a cause not excluded in the policy; (d) (i) coastal or river erosion, (ii) storm, tempest, water and rain to the property in the open (other than property designed to exist and operate in the open), (iii) freezing, solidification or inadvertent escape of molten or gaseous material, unless a fire ensues, then the insurer shall be liable for such ensuing damage, or (iv) false programming, punching, labeling or inserting, inadvertent cancelling of information or discarding of data media, and the loss of information caused by magnetic fields; 13 2. damage caused by or arising from (a) any willful act or willful negligence on the part of the policyholder or any person acting on his behalf, (b) cessation of work, (c) the delay or loss of market, or (d) consequential losses of any description other than those insured; 3. damage occasioned directly or indirectly by or through or in consequence of any of the following occurrences namely (a) war, the invasion act of foreign enemy, hostilities or warlike operations (whether war be declared or not), or civil war, (b) mutiny, civil commotion assuming the proportions of or amounting to a popular uprising, military rising, insurrection, rebellion, revolution, military or usurped power, (c) any acts of terrorism, For this purpose, an 'act of terrorism' means an act, including but not limited to the use of force or violence and/or the threat thereof, of any person or group(s) of persons, whether acting alone or on behalf of or in connection with any organization(s) or government(s), committed for political, religious, ideological or similar purposes including the intention to influence any government and/or to put the public or any section of the public in fear. (d) (i) permanent or temporary dispossession resulting from confiscation, nationalization, commandeering or requisition by any lawfully constituted authority, or (ii) permanent or temporary dispossession of any building resulting from the unlawful occupation of such building by any person, provided that the insurers are not relieved of any liability to the policyholder in respect of the damage to the property insured occurring before dispossession or during temporary dispossession which is otherwise insured by this policy; or (e) the destruction of property by order of any public authority; and 4. damage directly or indirectly caused by or arising from or in consequence of or contributed to by (a) nuclear weapons material, or (b) ionising, radiations or contamination by radioactivity from any nuclear fuel or from any unclear waste from the combustion of nuclear fuel. Exhibit 5: Contribution Clause If at the time of any loss, destruction or damage happening to any subject matter insured there be any other subsisting insurances whether by the policyholder or by any other person or persons covering the same subject matter, the insurer shall not be liable to pay or contribute more than its rateable proportion of such loss, destruction or damage. Exhibit 6: Deductibles Clause This policy does not cover the amounts of the deductibles stated in the policy schedule in respect of each and every loss as ascertained, after the application of all other terms and conditions of the policy including any condition of average. Exhibit 7: Average Clause The sums insured of each item under this policy are declared to be separately subject to average. If the subject matter insured at the time of any loss, destruction or damage be collectively of greater value than the sum insured thereon, then the policyholder shall be considered as being his own insurer for the difference and shall bear a rateable proportion of the loss accordingly. Every item (if more than one) of the policy shall be separately subject to this condition. Exhibit 8: Subrogation Clause The policyholder shall at the expense of the insurer do and concur in doing and permit to be done all such acts and things as may be necessary or reasonably required by the insurer for the purpose of enforcing any rights and remedies or of obtaining relief and indemnity from other parties to which the insurer shall be or would become entitled or subrogated upon paying for or making good any loss, destruction or damage under this policy whether such acts and things shall be or become necessary or required before or after the indemnification by the insurer. Exhibit 9: Repair and Replacement Clause The insurer may at its option reinstate or replace the property damaged or destroyed, or any part thereof, instead of paying the amount of the loss or damage, or may join with any other insurer or insurers in so doing but the insurer shall not be bound to reinstate exactly or completely but only as circumstances permit and in reasonably sufficient manner and in no case shall the insurer be bound to expend more in reinstatement than it would have cost to reinstate such property as it was at the time of the occurrence of such loss or damage nor more than the sum insured by the insurer thereon. If the insurer so elect to reinstate or replace any property, the policyholder shall at his own expense furnish the insurer with such plans, specifications, measurements, quantities and such other particulars as the insurer may require, and no acts done or caused to be done by the insurer with a view to reinstatement or replacement shall be deemed an election by the insurer to reinstate or replaceStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management Principles And Applications

Authors: Arthur J. Keown

9th Edition

013033362X, 9780130333629