Answered step by step

Verified Expert Solution

Question

1 Approved Answer

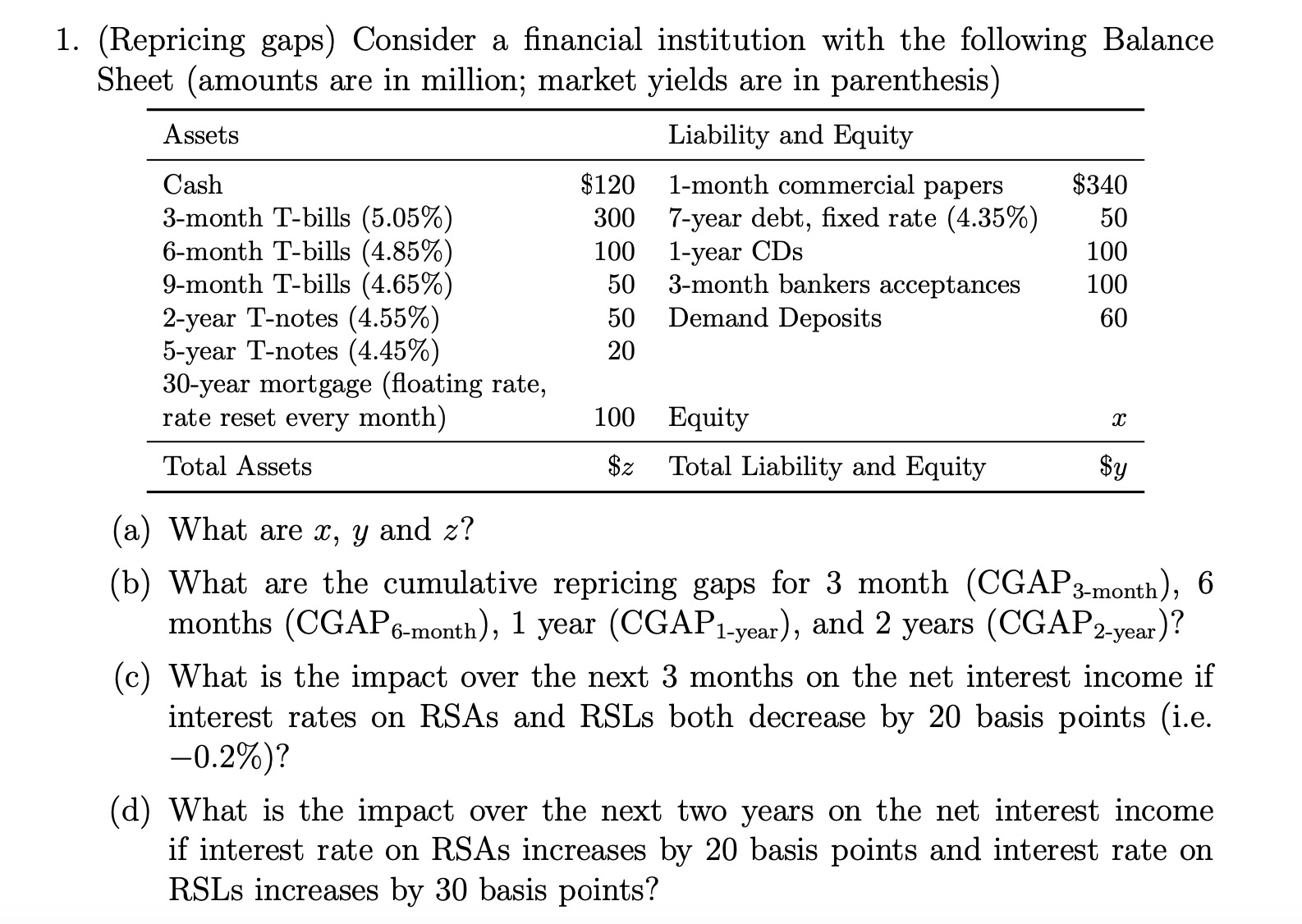

( Repricing gaps ) Consider a financial institution with the following Balance Sheet ( amounts are in million; market yields are in parenthesis ) (

Repricing gaps Consider a financial institution with the following Balance

Sheet amounts are in million; market yields are in parenthesis

a What are and

b What are the cumulative repricing gaps for month

months year and years

c What is the impact over the next months on the net interest income if

interest rates on RSAs and RSLs both decrease by basis points ie

d What is the impact over the next two years on the net interest income

if interest rate on RSAs increases by basis points and interest rate on

RSLs increases by basis points?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance For Non Financial Managers

Authors: Gene Siciliano

1st Edition

0071413774, 978-0071413770