Answered step by step

Verified Expert Solution

Question

1 Approved Answer

REQ. #1 - JOURNAL ENTRY DROP DOWN OPTIONS: No journal entry required Accumulated depreciation Buildings Cash Common stock Cost of goods sold Deferred rent revenue

REQ. #1 - JOURNAL ENTRY DROP DOWN OPTIONS:

- No journal entry required

- Accumulated depreciation

- Buildings

- Cash

- Common stock

- Cost of goods sold

- Deferred rent revenue

- Depreciation expense

- Dividends

- Equipment

- Income tax expense

- Income tax payable

- Insurance expense

- Interest expense

- Interest payable

- Interest revenue

- Inventory

- Notes payable

- Operating expenses

- Paid-in capital - excess of par

- Patent

- Prepaid insurance

- Rent revenue

- Retained earnings

- Salaries expense

- Salaries payable

- Treasury stock

REQ. #2 - COMPARATIVE INCOME STATEMENT DROP DOWN OPTIONS:

- Cost of goods sold

- Income tax expense

- Interest expense

- Operating expenses

- Revenues

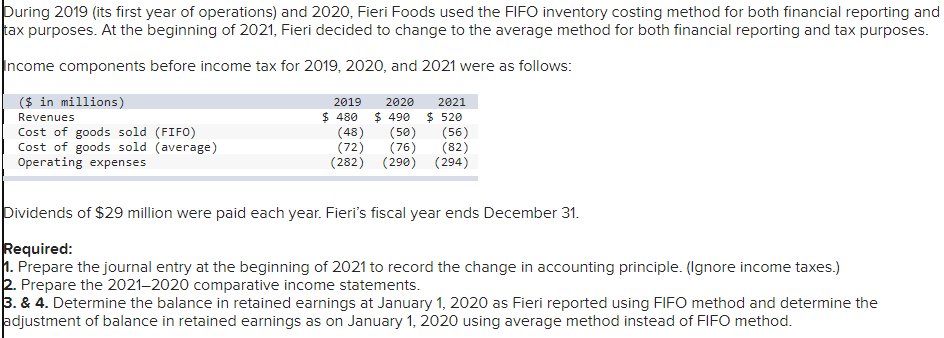

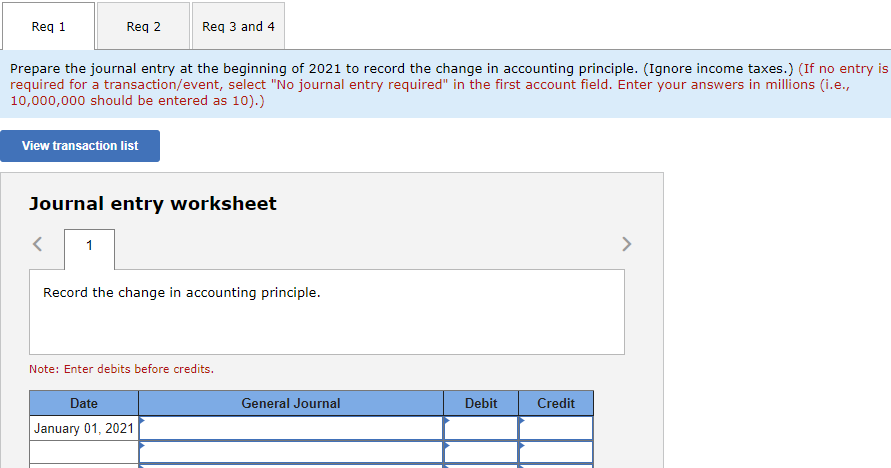

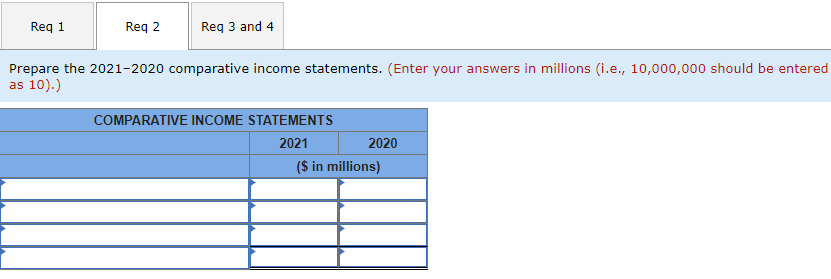

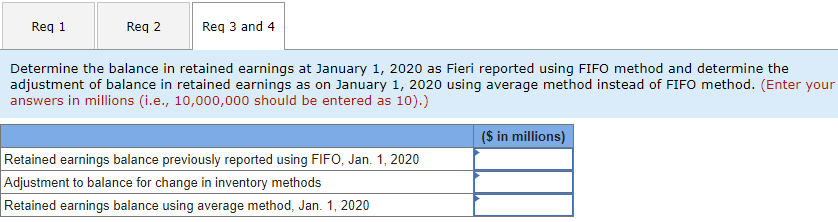

During 2019 (its first year of operations) and 2020, Fieri Foods used the FIFO inventory costing method for both financial reporting and tax purposes. At the beginning of 2021, Fieri decided to change to the average method for both financial reporting and tax purposes. Income components before income tax for 2019, 2020, and 2021 were as follows: Dividends of $29 million were paid each year. Fieri's fiscal year ends December 31. Required: 1. Prepare the journal entry at the beginning of 2021 to record the change in accounting principle. (Ignore income taxes.) 2. Prepare the 2021-2020 comparative income statements. 3. \& 4. Determine the balance in retained earnings at January 1, 2020 as Fieri reported using FIFO method and determine the adjustment of balance in retained earnings as on January 1, 2020 using average method instead of FIFO method. Prepare the journal entry at the beginning of 2021 to record the change in accounting principle. (Ignore income taxes.) (If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Enter your answers in millions (i.e., 10,000,000 should be entered as 10).) Journal entry worksheet Note: Enter debits before credits. Prepare the 2021-2020 comparative income statements. (Enter your answers in millions (i.e., 10,000,000 should be enterec as 10).) Determine the balance in retained earnings at January 1, 2020 as Fieri reported using FIFO method and determine the adjustment of balance in retained earnings as on January 1, 2020 using average method instead of FIFO method. (Enter your answers in millions (i.e., 10,000,000 should be entered as 10).)

During 2019 (its first year of operations) and 2020, Fieri Foods used the FIFO inventory costing method for both financial reporting and tax purposes. At the beginning of 2021, Fieri decided to change to the average method for both financial reporting and tax purposes. Income components before income tax for 2019, 2020, and 2021 were as follows: Dividends of $29 million were paid each year. Fieri's fiscal year ends December 31. Required: 1. Prepare the journal entry at the beginning of 2021 to record the change in accounting principle. (Ignore income taxes.) 2. Prepare the 2021-2020 comparative income statements. 3. \& 4. Determine the balance in retained earnings at January 1, 2020 as Fieri reported using FIFO method and determine the adjustment of balance in retained earnings as on January 1, 2020 using average method instead of FIFO method. Prepare the journal entry at the beginning of 2021 to record the change in accounting principle. (Ignore income taxes.) (If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Enter your answers in millions (i.e., 10,000,000 should be entered as 10).) Journal entry worksheet Note: Enter debits before credits. Prepare the 2021-2020 comparative income statements. (Enter your answers in millions (i.e., 10,000,000 should be enterec as 10).) Determine the balance in retained earnings at January 1, 2020 as Fieri reported using FIFO method and determine the adjustment of balance in retained earnings as on January 1, 2020 using average method instead of FIFO method. (Enter your answers in millions (i.e., 10,000,000 should be entered as 10).) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Continuous Auditing Theory And Application

Authors: David Y. Chan, Victoria Chiu

1st Edition

1787434141, 978-1787434141