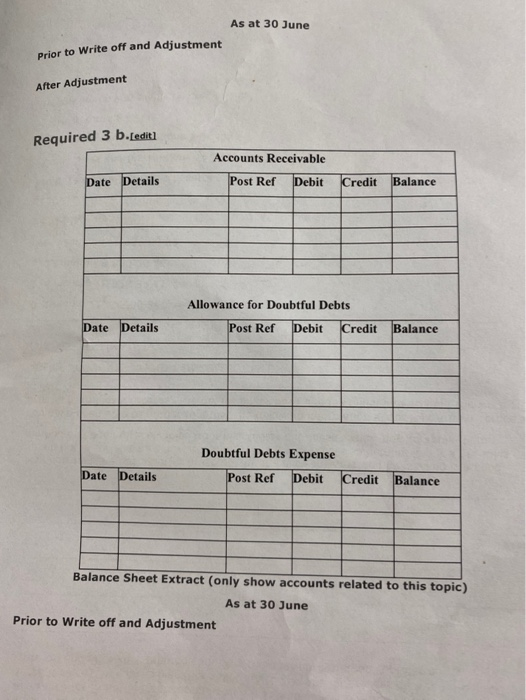

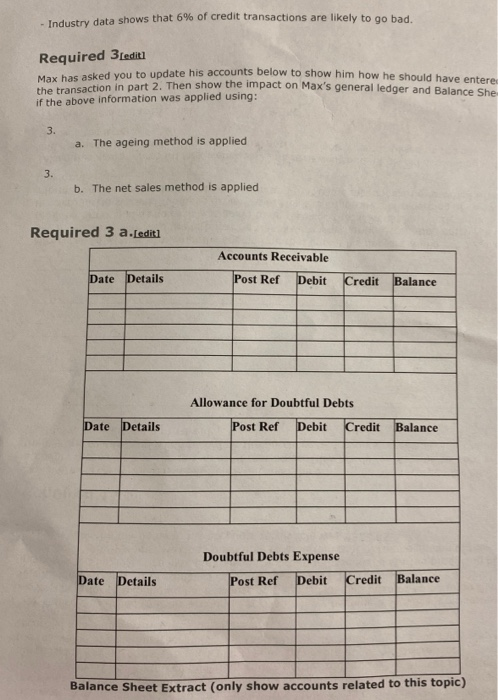

require 3 only

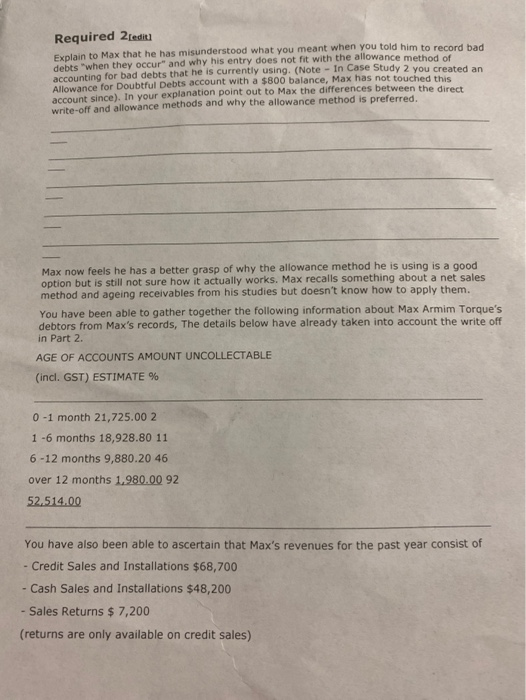

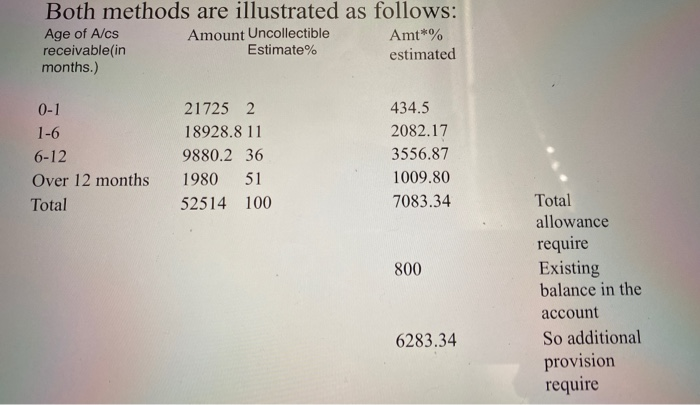

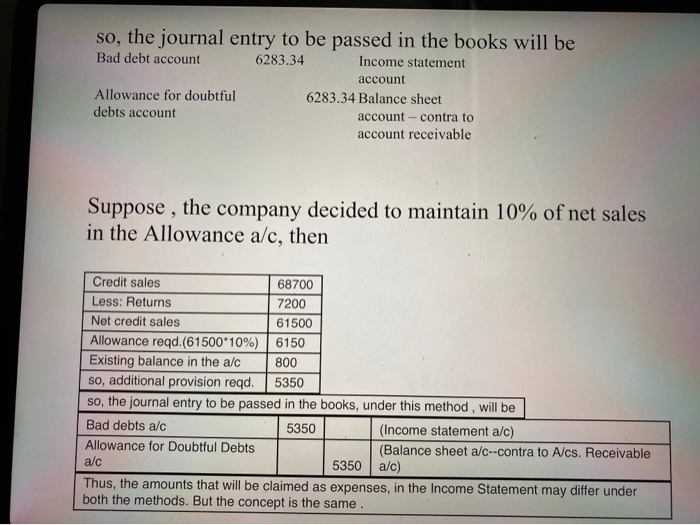

Max has asked you to update his accounts below to show him how he should have entere - Industry data shows that 6% of credit transactions are likely to go bad. Required 3[edit the transaction in part 2. Then show the impact on Max's general ledger and Balance She if the above information was applied using: 3. a. The ageing method is applied 3. b. The net sales method is applied Required 3 a.[edit] Accounts Receivable Date Details Post Ref Debit Credit Balance Allowance for Doubtful Debts Date Details Post Ref Debit Credit Balance Doubtful Debts Expense Post Ref Debit Credit Date Details Balance Balance Sheet Extract (only show accounts related to this topic) As at 30 June Prior to Write off and Adjustment After Adjustment Required 3 b.[edit] Accounts Receivable Date Details Post Ref Debit Credit Balance Allowance for Doubtful Debts Date Details Post Ref Debit Credit Balance Doubtful Debts Expense Post Ref Debit Credit Date Details Balance Balance Sheet Extract (only show accounts related to this topic) As at 30 June Prior to Write off and Adjustment Required 2 [edit Explain to Max that he has misunderstood what you meant when you told him to record bad debts 'when they occur" and why his entry does not fit with the allowance method of accounting for bad debts that he is currently using. (Note - In Case Study 2 you created an Allowance for Doubtful Debts account with a $800 balance, Max has not touched this account since). In your explanation point out to Max the differences between the direct write-off and allowance methods and why the allowance method is preferred. Max now feels he has a better grasp of why the allowance method he is using is a good option but is still not sure how it actually works. Max recalls something about a net sales method and ageing receivables from his studies but doesn't know how to apply them. You have been able to gather together the following information about Max Armim Torque's debtors from Max's records, The details below have already taken into account the write off in Part 2 AGE OF ACCOUNTS AMOUNT UNCOLLECTABLE (incl. GST) ESTIMATE % 0-1 month 21,725.00 2 1 -6 months 18,928.80 11 6-12 months 9,880.20 46 over 12 months 1.980.00 92 52.514.00 You have also been able to ascertain that Max's revenues for the past year consist of - Credit Sales and Installations $68,700 - Cash Sales and Installations $48,200 -Sales Returns $ 7,200 (returns are only available on credit sales) Both methods are illustrated as follows: Age of A/cs Amount Uncollectible Amt*% receivable(in Estimate% estimated months.) 0-1 1-6 6-12 Over 12 months Total 21725 2. 18928.8 11 9880.2 36 1980 51 52514 100 434.5 2082.17 3556.87 1009.80 7083.34 800 Total allowance require Existing balance in the account So additional provision require 6283.34 so, the journal entry to be passed in the books will be Bad debt account 6283.34 Income statement account Allowance for doubtful 6283.34 Balance sheet debts account account - contra to account receivable Suppose , the company decided to maintain 10% of net sales in the Allowance a/c, then Credit sales 68700 Less: Returns 7200 Net credit sales 61500 Allowance reqd(61500*10%) 6150 Existing balance in the a/c 800 so, additional provision reqd. 5350 so, the journal entry to be passed in the books, under this method, will be Bad debts a/c 5350 (Income statement a/c) Allowance for Doubtful Debts (Balance sheet a/c-contra to A/cs. Receivable a/c 5350 a/c) Thus, the amounts that will be claimed as expenses, in the Income Statement may differ under both the methods. But the concept is the same. Max has asked you to update his accounts below to show him how he should have entere - Industry data shows that 6% of credit transactions are likely to go bad. Required 3[edit the transaction in part 2. Then show the impact on Max's general ledger and Balance She if the above information was applied using: 3. a. The ageing method is applied 3. b. The net sales method is applied Required 3 a.[edit] Accounts Receivable Date Details Post Ref Debit Credit Balance Allowance for Doubtful Debts Date Details Post Ref Debit Credit Balance Doubtful Debts Expense Post Ref Debit Credit Date Details Balance Balance Sheet Extract (only show accounts related to this topic) As at 30 June Prior to Write off and Adjustment After Adjustment Required 3 b.[edit] Accounts Receivable Date Details Post Ref Debit Credit Balance Allowance for Doubtful Debts Date Details Post Ref Debit Credit Balance Doubtful Debts Expense Post Ref Debit Credit Date Details Balance Balance Sheet Extract (only show accounts related to this topic) As at 30 June Prior to Write off and Adjustment Required 2 [edit Explain to Max that he has misunderstood what you meant when you told him to record bad debts 'when they occur" and why his entry does not fit with the allowance method of accounting for bad debts that he is currently using. (Note - In Case Study 2 you created an Allowance for Doubtful Debts account with a $800 balance, Max has not touched this account since). In your explanation point out to Max the differences between the direct write-off and allowance methods and why the allowance method is preferred. Max now feels he has a better grasp of why the allowance method he is using is a good option but is still not sure how it actually works. Max recalls something about a net sales method and ageing receivables from his studies but doesn't know how to apply them. You have been able to gather together the following information about Max Armim Torque's debtors from Max's records, The details below have already taken into account the write off in Part 2 AGE OF ACCOUNTS AMOUNT UNCOLLECTABLE (incl. GST) ESTIMATE % 0-1 month 21,725.00 2 1 -6 months 18,928.80 11 6-12 months 9,880.20 46 over 12 months 1.980.00 92 52.514.00 You have also been able to ascertain that Max's revenues for the past year consist of - Credit Sales and Installations $68,700 - Cash Sales and Installations $48,200 -Sales Returns $ 7,200 (returns are only available on credit sales) Both methods are illustrated as follows: Age of A/cs Amount Uncollectible Amt*% receivable(in Estimate% estimated months.) 0-1 1-6 6-12 Over 12 months Total 21725 2. 18928.8 11 9880.2 36 1980 51 52514 100 434.5 2082.17 3556.87 1009.80 7083.34 800 Total allowance require Existing balance in the account So additional provision require 6283.34 so, the journal entry to be passed in the books will be Bad debt account 6283.34 Income statement account Allowance for doubtful 6283.34 Balance sheet debts account account - contra to account receivable Suppose , the company decided to maintain 10% of net sales in the Allowance a/c, then Credit sales 68700 Less: Returns 7200 Net credit sales 61500 Allowance reqd(61500*10%) 6150 Existing balance in the a/c 800 so, additional provision reqd. 5350 so, the journal entry to be passed in the books, under this method, will be Bad debts a/c 5350 (Income statement a/c) Allowance for Doubtful Debts (Balance sheet a/c-contra to A/cs. Receivable a/c 5350 a/c) Thus, the amounts that will be claimed as expenses, in the Income Statement may differ under both the methods. But the concept is the same