Answered step by step

Verified Expert Solution

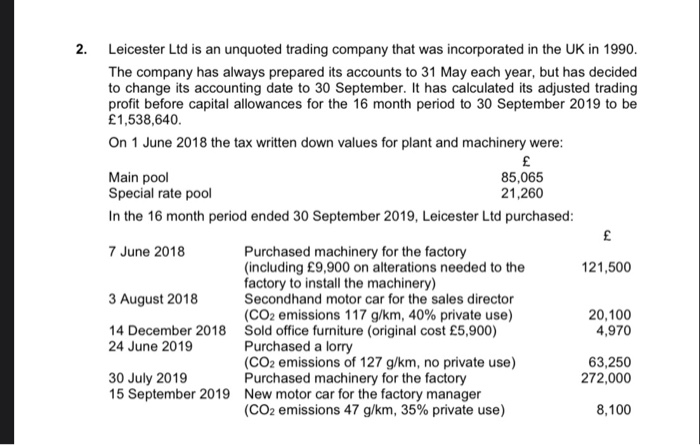

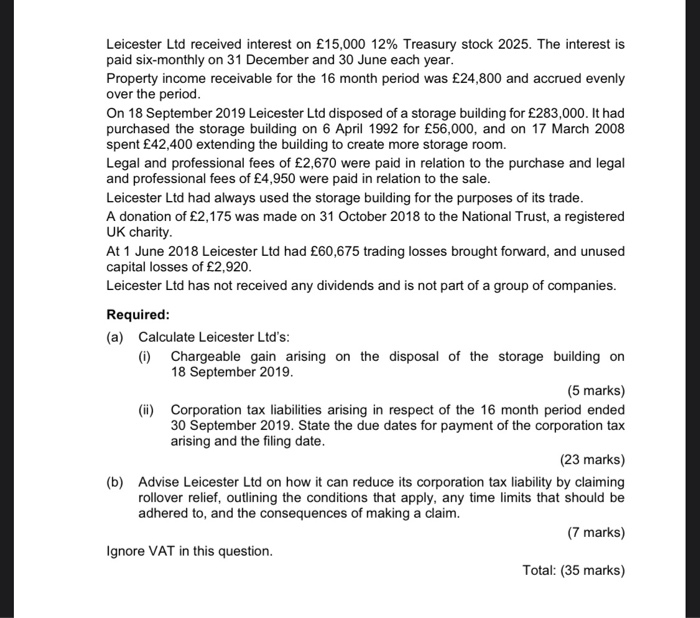

Question

1 Approved Answer

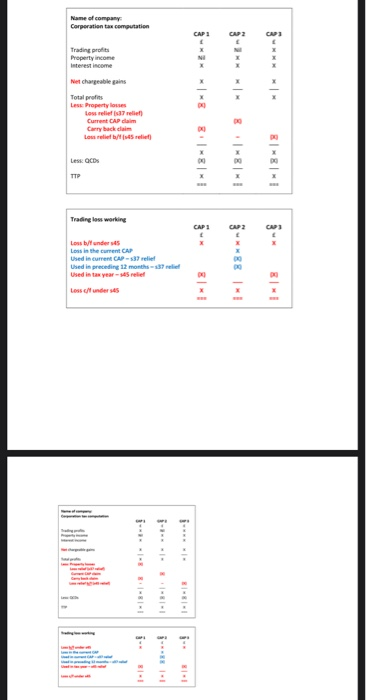

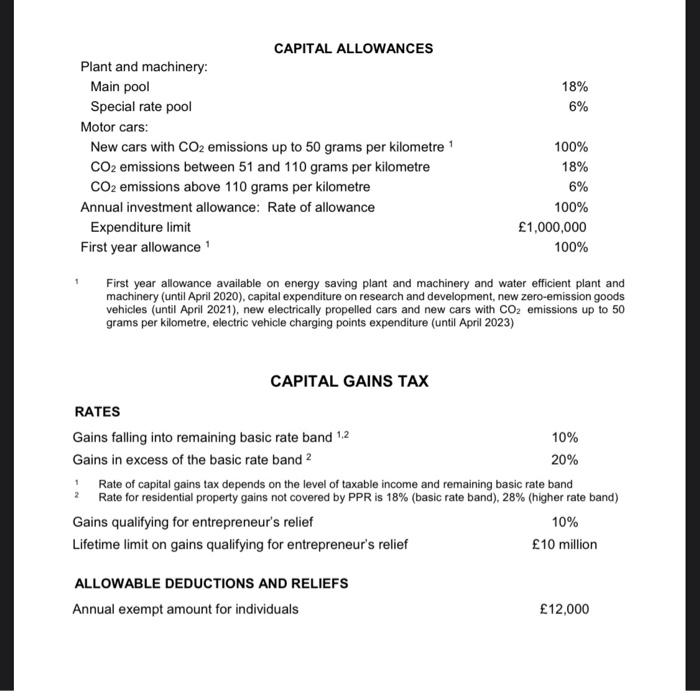

Required: (a) Calculate Leicester Ltds: (i) Chargeable gain arising on the disposal of the storage building on 18 September 2019. (5 marks) (ii) Corporation tax

Required:

(a) Calculate Leicester Ltds:

(i) Chargeable gain arising on the disposal of the storage building on 18 September 2019.

(5 marks)

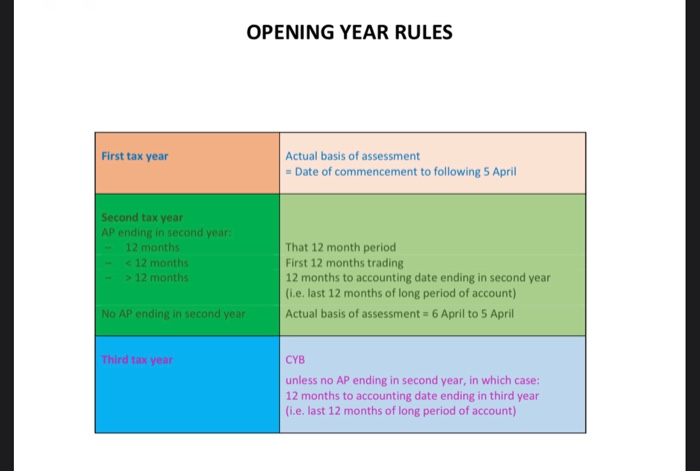

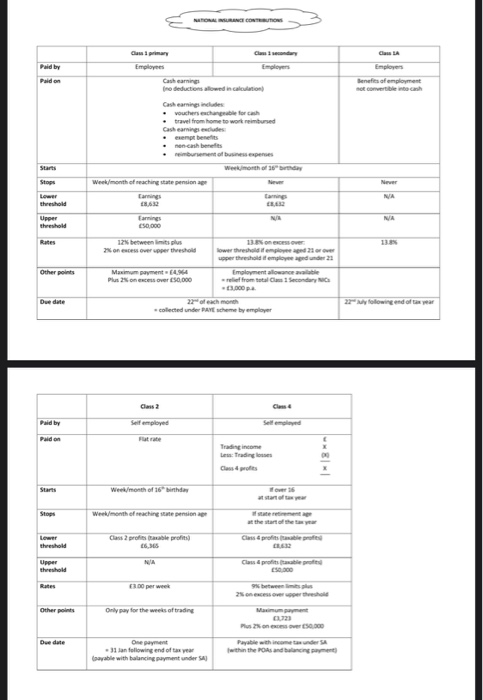

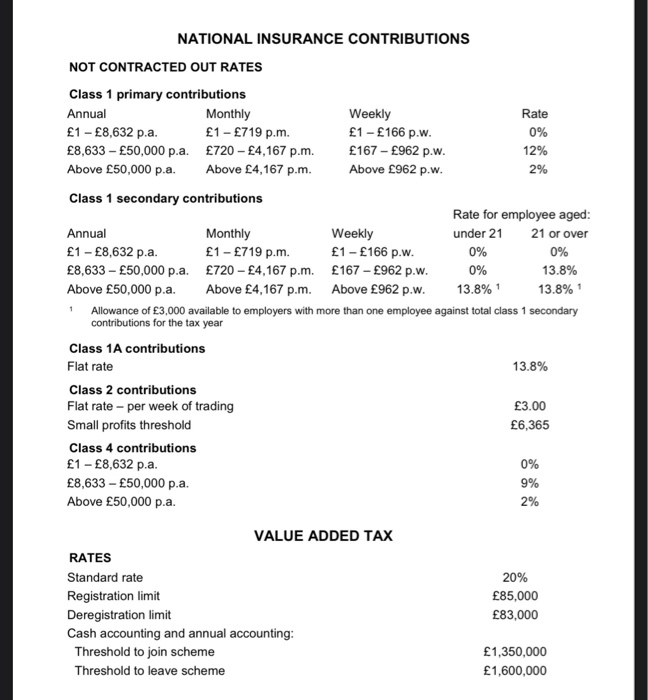

(ii) Corporation tax liabilities arising in respect of the 16 month period ended 30 September 2019. State the due dates for payment of the corporation tax arising and the filing date.

(23 marks)

(b) Advise Leicester Ltd on how it can reduce its corporation tax liability by claiming rollover relief, outlining the conditions that apply, any time limits that should be adhered to, and the consequences of making a claim.

Ignore VAT in this question.

(7 marks) Total: (35 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Excel For Accountants Tips, Tricks & Techniques

Authors: Conrad Carlberg

1st Edition

1932925015, 9781932925012