Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Required B: what was the dollar amount of gross profit? Required information The following information applies to the questions displayed below] Inventory at the beginning

Required B: what was the dollar amount of gross profit?

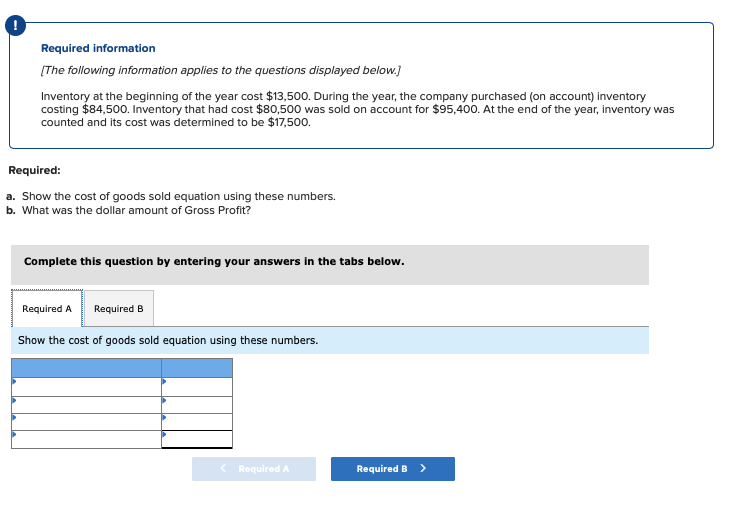

Required information The following information applies to the questions displayed below] Inventory at the beginning of the year cost $13,500. During the year, the company purchased (on account) inventory costing $84,500. Inventory that had cost $80,500 was sold on account for $95,400. At the end of the year, inventory was counted and its cost was determined to be $17,500. Required: a. Show the cost of goods sold equation using these numbers. b. What was the dollar amount of Gross Profit? Complete this question by entering your answers in the tabs below. Required ARequired B Show the cost of goods sold equation using these numbers Required A Required BStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Access Audit Handbook

Authors: Alison Grant

1st Edition

1859461778, 978-1859461778