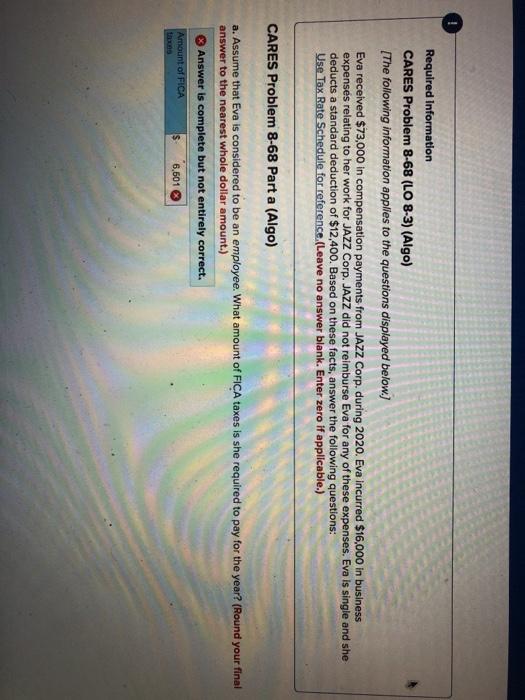

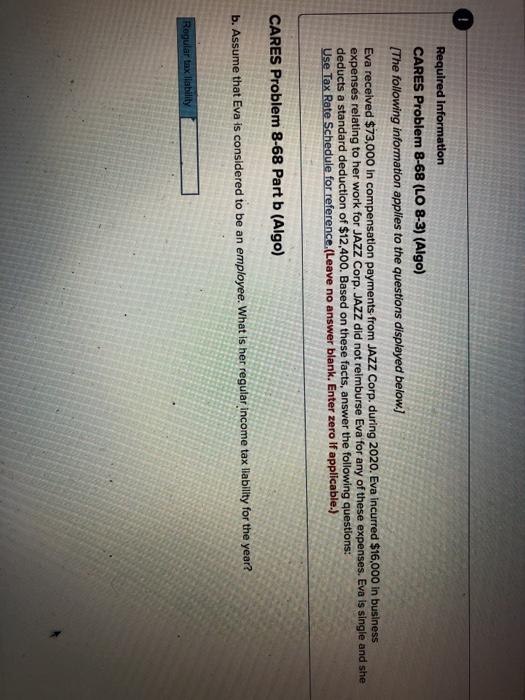

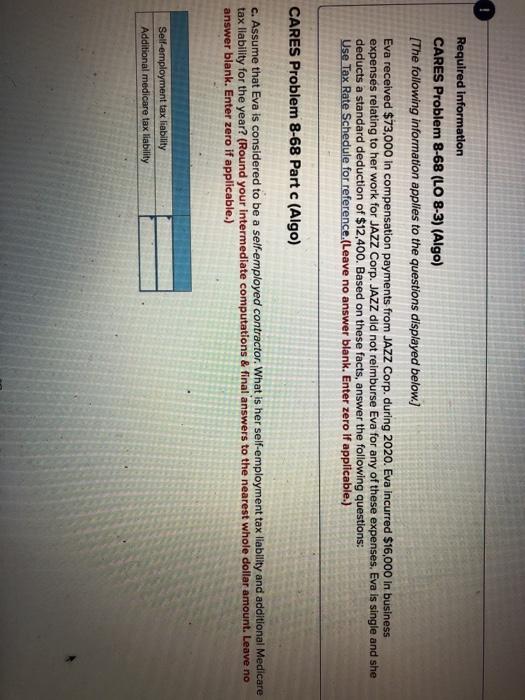

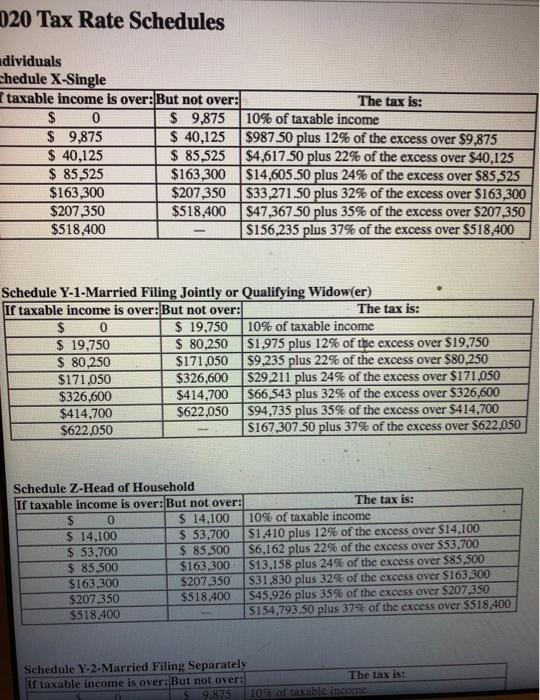

Required Information CARES Problem 8-68 (LO 8-3) (Algo) [The following information applies to the questions displayed below.) Eva received $73,000 in compensation payments from JAZZ Corp. during 2020. Eva incurred $16,000 in business expenses relating to her work for JAZZ Corp. JAZZ did not reimburse Eva for any of these expenses. Eva is single and she deducts a standard deduction of $12,400. Based on these facts, answer the following questions: Use Tax Rate Schedule for reference (Leave no answer blank. Enter zero if applicable.) CARES Problem 8-68 Part a (Algo) a. Assume that Eva is considered to be an employee. What amount of FICA taxes is she required to pay for the year? (Round your final answer to the nearest whole dollar amount.) Answer is complete but not entirely correct, Amount of FICA thons s 6,601 Required Information CARES Problem 8-68 (LO 8-3) (Algo) [The following information applies to the questions displayed below.) Eva received $73,000 in compensation payments from JAZZ Corp. during 2020. Eva incurred $16,000 in business expenses relating to her work for JAZZ Corp. JAZZ did not reimburse Eva for any of these expenses. Eva is single and she deducts a standard deduction of $12,400. Based on these facts, answer the following questions: Use Tax Rate Schedule for reference (Leave no answer blank. Enter zero If applicable.) CARES Problem 8-68 Part b (Algo) b. Assume that Eva is considered to be an employee. What is her regular income tax liability for the year? Regular tax lability Required Information CARES Problem 8-68 (LO 8-3) (Algo) [The following information applies to the questions displayed below.) Eva received $73,000 in compensation payments from JAZZ Corp. during 2020. Eva incurred $16,000 in business expenses relating to her work for JAZZ Corp. JAZZ did not reimburse Eva for any of these expenses. Eva is single and she deducts a standard deduction of $12,400. Based on these facts, answer the following questions: Use Tax Rate Schedule for reference (Leave no answer blank. Enter zero if applicable.) CARES Problem 8-68 Part c (Algo) c. Assume that Eva is considered to be a self-employed contractor. What is her self-employment tax liability and additional Medicare tax liability for the year? (Round your intermediate computations & final answers to the nearest whole dollar amount. Leave no answer blank. Enter zero if applicable.) Self-employment tax liability Additional medicare tax liability 020 Tax Rate Schedules dividuals chedule X-Single I taxable income is over: But not over: The tax is: $ 0 $ 9,875 10% of taxable income $ 9,875 $ 40,125 $987.50 plus 12% of the excess over $9,875 $ 40,125 $ 85,525 $4,617.50 plus 22% of the excess over $40,125 $ 85,525 $163,300 $14,605.50 plus 24% of the excess over $85,525 $163,300 $207,350 $33,271.50 plus 32% of the excess over $163,300 $207,350 $518,400 $47,367 50 plus 35% of the excess over $207,350 $518,400 $156,235 plus 37% of the excess over $518,400 Schedule Y-1-Married Filing Jointly or Qualifying Widow(er) If taxable income is over: But not over: The tax is: $ 0 $ 19,750 10% of taxable income $ 19,750 $ 80,250 $1,975 plus 12% of the excess over $19,750 $ 80,250 $171,050 $9,235 plus 22% of the excess over $80,250 $171,050 $326,600 $29,211 plus 24% of the excess over $171.050 $326,600 $414,700 $66,543 plus 32% of the excess over $326,600 $414,700 $622,050 $94,735 plus 35% of the excess over $414.700 $622,050 $167,307.50 plus 37% of the excess over $622,050 Schedule Z-Head of Household If taxable income is over: But not over: The tax is: 0 $ 14,100 10% of taxable income $ 14,100 $ 53,700 $1.410 plus 12% of the excess over $14.100 $ 53,700 $ 85,500 $6,162 plus 22% of the excess over $53.700 $ 85,500 $163.300 $13,158 plus 24% of the excess over $85.500 $163.300 $207.350 $31,830 plus 32% of the excess over $163,300 $207,350 $518,400 $45.926 plus 35% of the excess over $207,350 $518.400 S154.793.50 plus 37% of the excess over $518.400 Schedule Y-2-Married Filing Separately If taxable income is over:But not over: The tax is: 9.875 10% of taxable income $622,050 Opus JJ UI We excess over $414,700 $167,307 50 plus 37% of the excess over $622,050 Schedule Z-Head of Household If taxable income is over: But not over: The tax is: $ 0 $ 14,100 10% of taxable income $ 14,100 $ 53,700 $1,410 plus 12% of the excess over $14,100 $ 53,700 $ 85,500 $6,162 plus 22% of the excess over $53,700 $ 85,500 $163,300 $13,158 plus 24% of the excess over $85,500 $163,300 $207,350 $31,830 plus 32% of the excess over $163,300 $207,350 $518,400 $45,926 plus 35% of the excess over $207,350 $518,400 $154,793.50 plus 37% of the excess over $518,400 - Schedule Y-2-Married Filing Separately If taxable income is over: But not over: The tax is: $ 0 $ 9.875 10% of taxable income $ 9,875 $ 40,125 $987.50 plus 12% of the excess over $9,875 $ 40,125 $ 85,525 $4,617.50 plus 22% of the excess over $40,125 $ 85,525 $163,300 $14,605.50 plus 24% of the excess over $85,525 $163,300 $207,350 $33,271.50 plus 32% of the excess over $163,300 $207,350 $311,025 $47,367.50 plus 35% of the excess over $207,350 $311,025 $83.653.75 plus 37% of the excess over $311,025