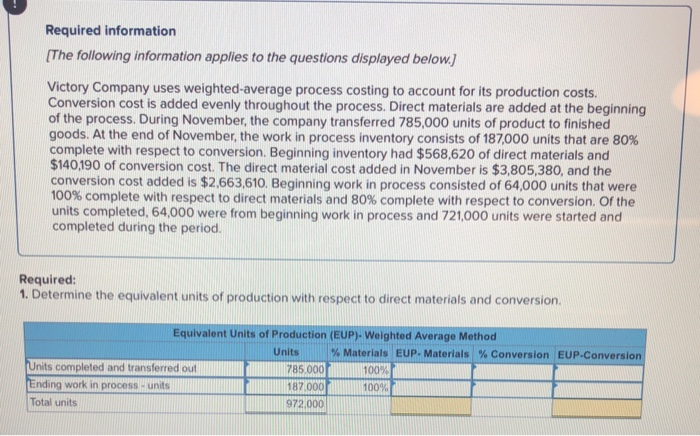

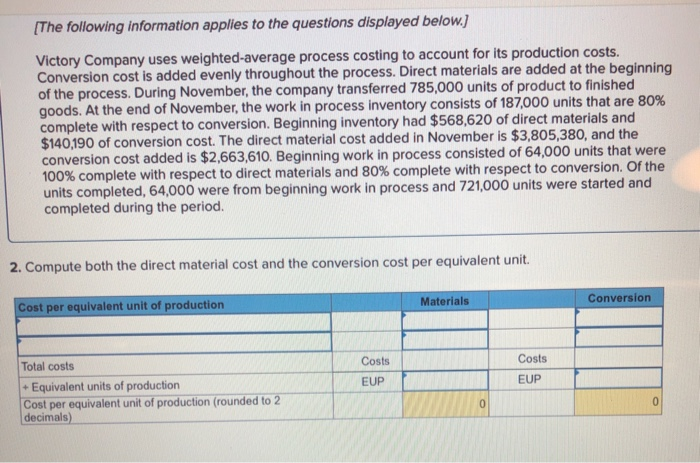

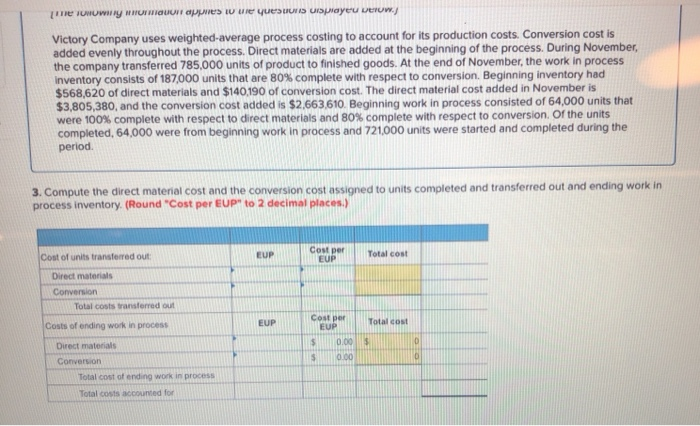

Required information IThe following information applies to the questions displayed below] Victory Company uses weighted-average process costing to account for its production costs. Conversion cost is added evenly throughout the process. Direct materials are added at the beginning of the process. During November, the company transferred 785,000 units of product to finished goods. At the end of November, the work in process inventory consists of 187,000 units that are 80% complete with respect to conversion. Beginning inventory had $568,620 of direct materials and $140190 of conversion cost. The direct material cost added in November is $3,805,380, and the conversion cost added is $2.663,610. Beginning work in process consisted of 64,000 units that were 100% complete with respect to direct materials and 80% complete with respect to conversion. Of the units completed, 64,000 were from beginning work in process and 721,000 units were started and completed during the period. Required: 1. Determine the equivalent units of production with respect to direct materials and conversion Equivalent Units of Production (EUP)- Weighted Average Method Units | % Materials EUP-Materials %Conversion EUP-Conversion Units completed and transferred out Ending work in process - units Total units 785,000 187,000 972.000 100% 100% The following information applies to the questions displayed below] Victory Company uses weighted-average process costing to account for its production costs. Conversion cost is added evenly throughout the process. Direct materials are added at the beginning of the process. During November, the company transferred 785,000 units of product to finished goods. At the end of November, the work in process inventory consists of 187000 units that are 8 complete with respect to conversion. Beginning inventory had $568,620 of direct materials and $140190 of conversion cost. The direct material cost added in November is $3,805,380, and the conversion cost added is $2,663,610. Beginning work in process consisted of 64,000 units that were 100% complete with respect to direct materials and 80% complete with respect to conversion. Of the units completed, 64,000 were from beginning work in process and 721,000 units were started and completed during the period. 2. Compute both the direct material cost and the conversion cost per equivalent unit. Materials Conversion Cost per equivalent unit of production Costs Costs EUP Total costs EUP Equivalent units of production Cost per equivalent unit of production (rounded to 2 decimals) 0 Victory Company uses weighted-average process costing to account for its production costs. Conversion cost is added evenly throughout the process. Direct materials are added at the beginning of the process. During November the company transferred 785.000 units of product to finished goods. At the end of November, the work in process inventory consists of 187,000 units that are 80% complete with respect to conversion. Beginning inventory had $568,620 of direct materials and $140190 of conversion cost. The direct material cost added in November is $3,805,380, and the conversion cost added is $2.663.610. Beginning work in process consisted of 64,000 units that were 100% complete with respect to direct materials and 80% complete with respect to conversion, or the units completed, 64,000 were from beginning work in process and 721000 units were started and completed during the period 3. Compute the direct material cost and the conversion cost assigned to units completed and transferred out and ending work in process inventory. (Round "Cost per EUPt to 2 decimal places.) Cost per Total cost Cost of units transterred out EUP EUP Direct materials Total costs transterred out Cost perTotal cost Costs of ending work in process Direct materials Conversion 0.00 s 0.00 Total cost of ending work in process Total costs accounted for