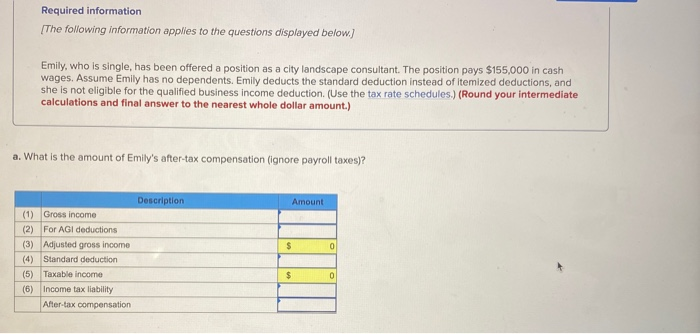

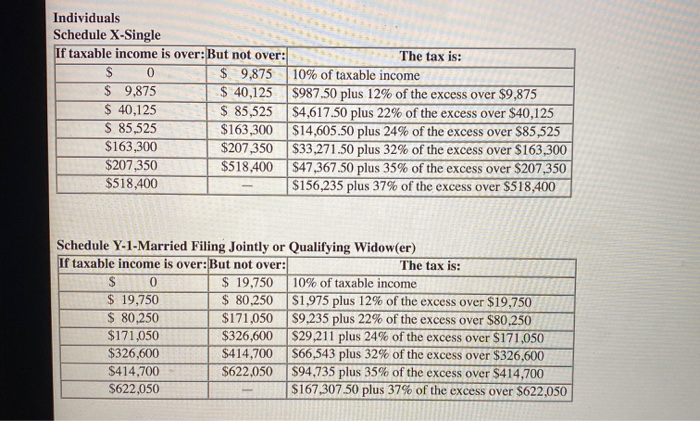

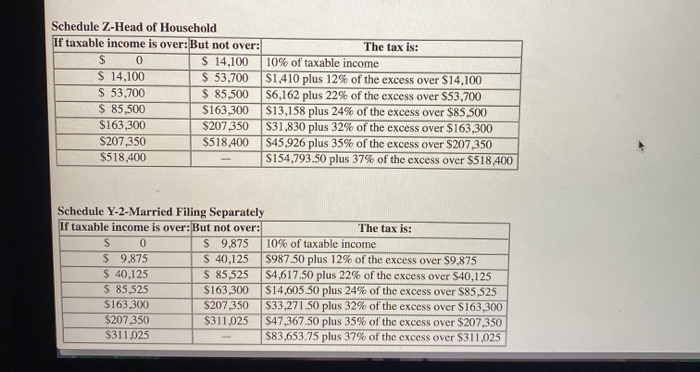

Required information The following information applies to the questions displayed below.) Emily, who is single, has been offered a position as a city landscape consultant. The position pays $155,000 in cash wages. Assume Emily has no dependents. Emily deducts the standard deduction instead of itemized deductions, and she is not eligible for the qualified business income deduction (Use the tax rate schedules.) (Round your intermediate calculations and final answer to the nearest whole dollar amount.) a. What is the amount of Emily's after-tax compensation (ignore payroll taxes)? Description Amount $ 0 (1) Gross income (2) For AGI deductions (3) Adjusted gross income (4) Standard deduction (5) Taxable income (6) Income tax liability After-tax compensation $ 0 Individuals Schedule X-Single If taxable income is over: But not over: The tax is: $ 0 $ 9,875 10% of taxable income $ 9.875 $ 40,125 $987.50 plus 12% of the excess over $9,875 $ 40,125 $ 85,525 $4,617.50 plus 22% of the excess over $40,125 $ 85,525 $ 163,300 $14,605.50 plus 24% of the excess over $85,525 $163,300 $207,350 $33,271.50 plus 32% of the excess over $163,300 $207,350 $518,400 $47,367.50 plus 35% of the excess over $207,350 $518,400 $156,235 plus 37% of the excess over $518,400 Schedule Y-1-Married Filing Jointly or Qualifying Widow(er) If taxable income is over: But not over: The tax is: $ 0 $ 19,750 10% of taxable income $ 19,750 $ 80,250 $1,975 plus 12% of the excess over $19,750 $ 80,250 $171,050 $9,235 plus 22% of the excess over $80,250 $171,050 $326,600 $29,211 plus 24% of the excess over $171,050 $326,600 $414,700 $66,543 plus 32% of the excess over $326,600 $414,700 $622,050 $94,735 plus 35% of the excess over $414,700 $622,050 $167,307 50 plus 37% of the excess over $622,050 Schedule Z-Head of Household If taxable income is over: But not over: $ 0 $ 14,100 $ 14,100 $ 53,700 $ 53,700 $ 85,500 $ 85,500 $163,300 $163,300 $207,350 $207,350 $518,400 $518,400 The tax is: 10% of taxable income $1,410 plus 12% of the excess over $14,100 56,162 plus 22% of the excess over $53,700 $13,158 plus 24% of the excess over $85,500 $31,830 plus 32% of the excess over $163,300 S45,926 plus 35% of the excess over $207,350 $154,793.50 plus 37% of the excess over $518,400 Schedule Y-2-Married Filing Separately If taxable income is over: But not over: The tax is: S 0 $ 9.875 10% of taxable income $ 9.875 $ 40,125 $987.50 plus 12% of the excess over $9.875 $ 40,125 $ 85,525 $4,617.50 plus 22% of the excess over $40,125 S 85,525 $163,300 $14,605 50 plus 24% of the excess over $85,525 $163,300 $207,350 $33,271.50 plus 32% of the excess over $ 163,300 $207,350 $311,025 $47,367 50 plus 35% of the excess over $207,350 $311,025 $83.653.75 plus 37% of the excess over $311,025