Answered step by step

Verified Expert Solution

Question

1 Approved Answer

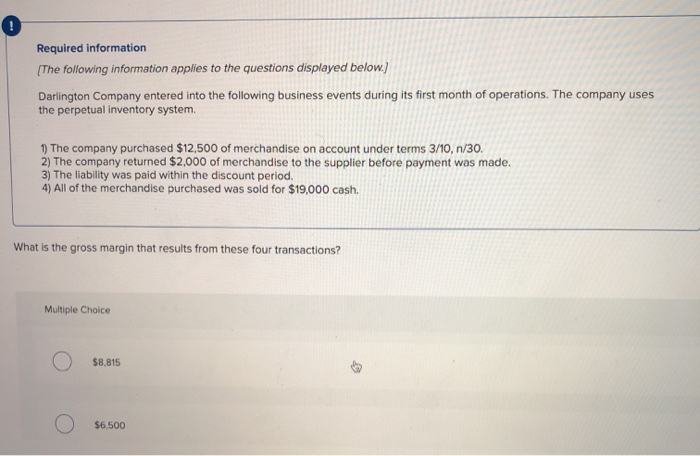

Required information (The following information applies to the questions displayed below.) Darlington Company entered into the following business events during its first month of operations.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

101 Recipes For Audit In Psychiatry

Authors: Clare Oakley, Floriana Coccia, Neil Masson, Iain McKinnon, Meinou Simmons

1st Edition

1908020016, 978-1908020017