Answered step by step

Verified Expert Solution

Question

1 Approved Answer

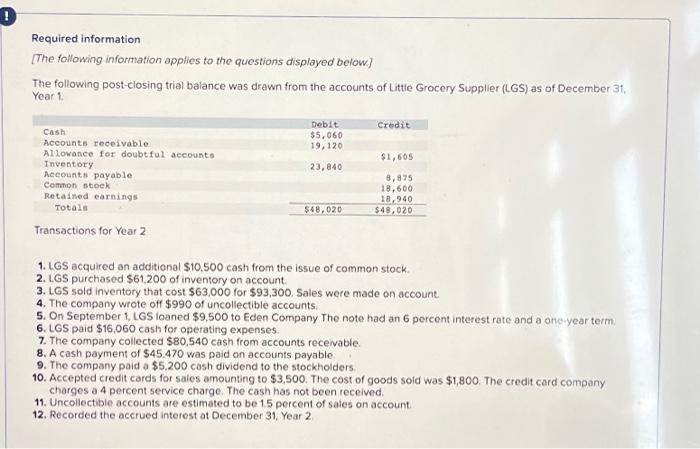

Required information [The following information applies to the questions displayed below.] The following post-closing trial balance was drawn from the accounts of Little Grocery Supplier

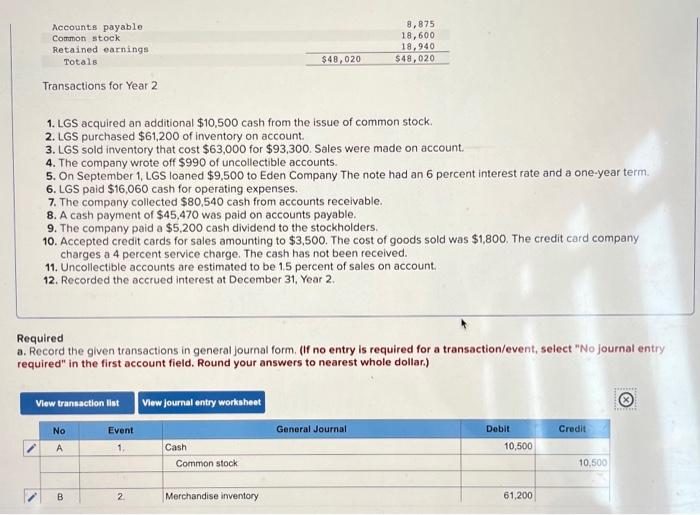

Required information [The following information applies to the questions displayed below.] The following post-closing trial balance was drawn from the accounts of Little Grocery Supplier (LGS) as of December 31, Year 1. Cash Accounts receivable Allowance for doubtful accounts Inventory Accounts payable Common stock Retained earnings Totals Transactions for Year 2 Debit $5,060 19, 120 23,840 $48,020 Credit 7. The company collected $80,540 cash from accounts receivable. 8. A cash payment of $45,470 was paid on accounts payable. $1,605 8,875 18,600 18,940 $48,020 1. LGS acquired an additional $10,500 cash from the issue of common stock. 2. LGS purchased $61,200 of inventory on account. 3. LGS sold inventory that cost $63,000 for $93,300. Sales were made on account. 4. The company wrote off $990 of uncollectible accounts. 5. On September 1, LGS loaned $9,500 to Eden Company The note had an 6 percent interest rate and a one-year term. 6. LGS paid $16,060 cash for operating expenses. 9. The company paid a $5,200 cash dividend to the stockholders. 10. Accepted credit cards for sales amounting to $3,500. The cost of goods sold was $1,800. The credit card company charges a 4 percent service charge. The cash has not been received. 11. Uncollectible accounts are estimated to be 1.5 percent of sales on account. 12. Recorded the accrued interest at December 31, Year 2.

Record the given transactions in general form.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Stand Up To The IRS How To Handle Audits Tax Bills And Tax Court

Authors: Frederick W. Daily Robin Leonard

2nd Edition

0873372409, 978-0873372404