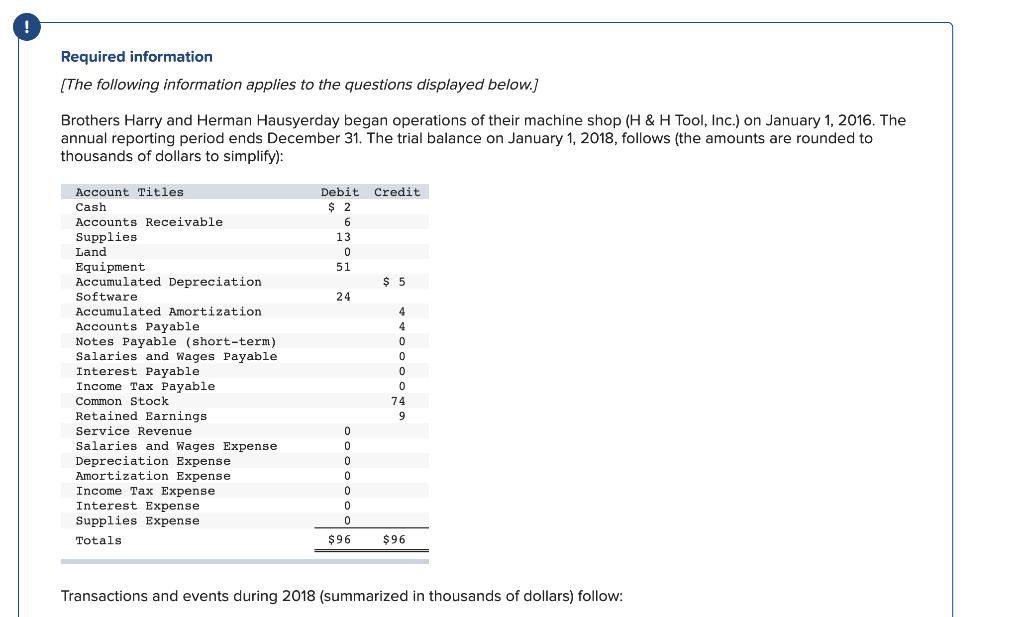

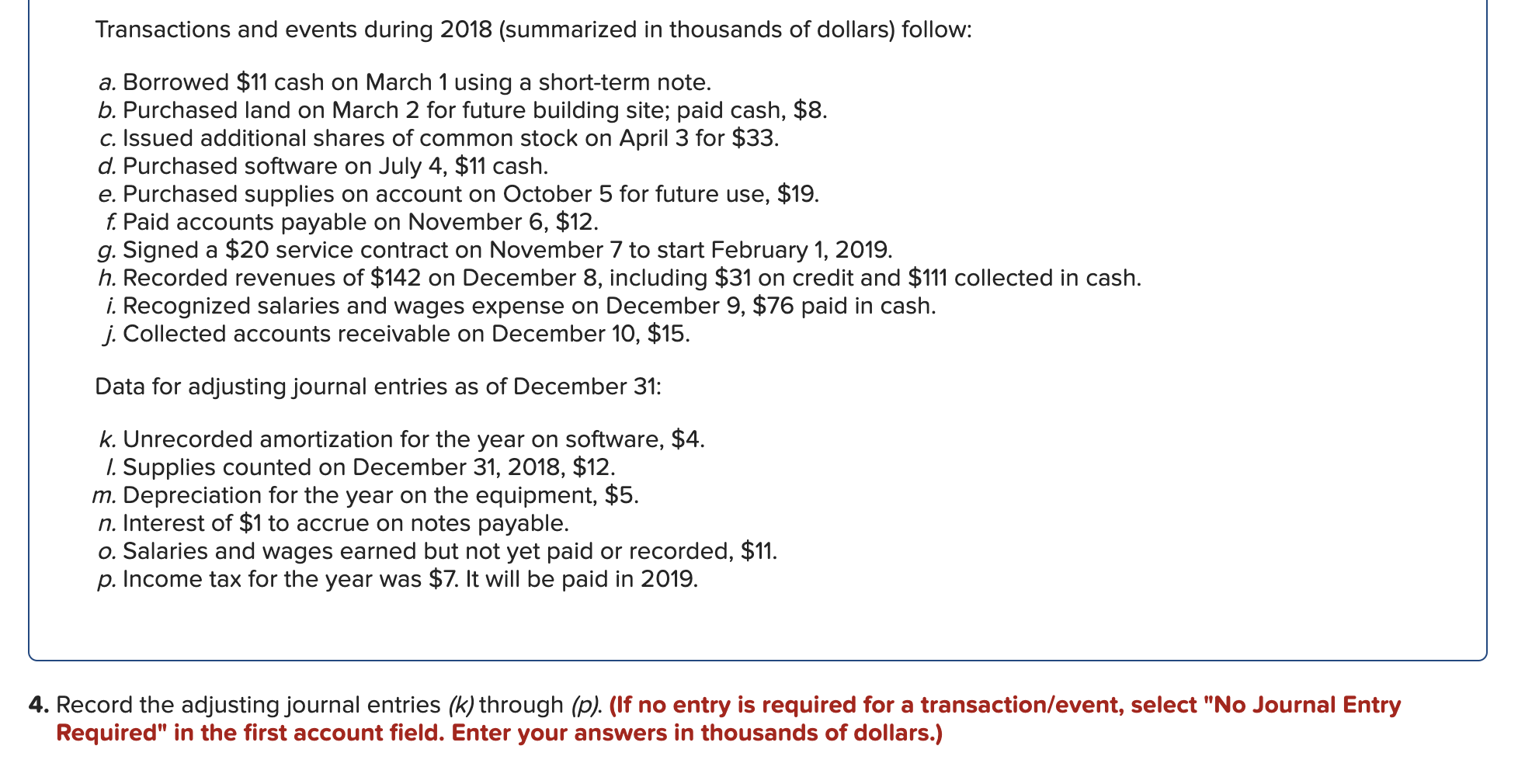

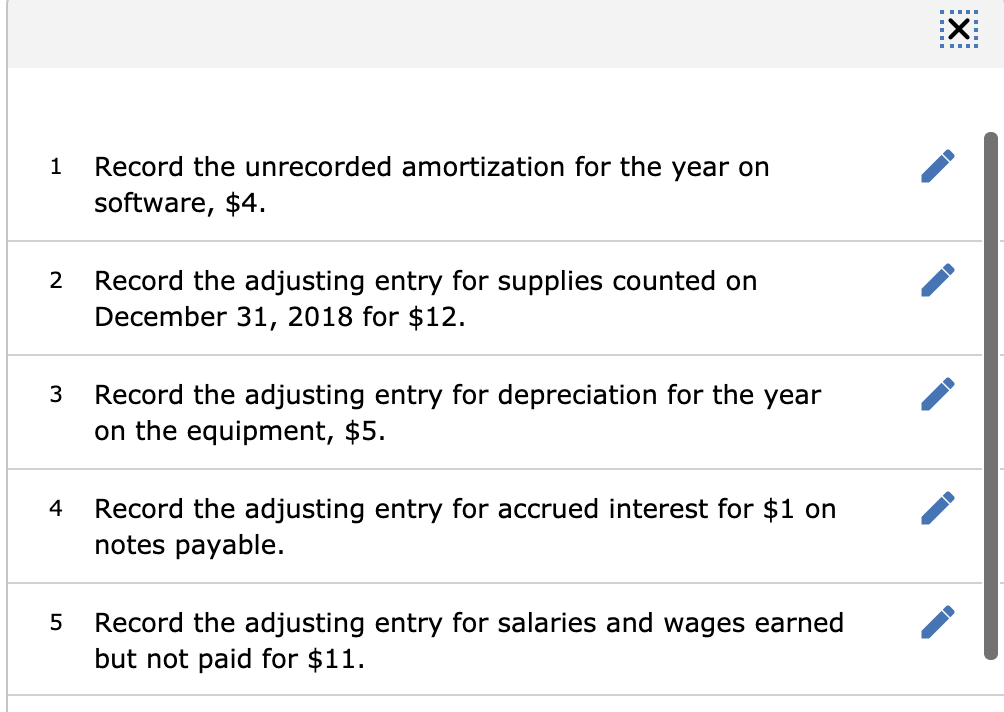

Required information (The following information applies to the questions displayed below.) Brothers Harry and Herman Hausyerday began operations of their machine shop (H&H Tool, Inc.) on January 1, 2016. The annual reporting period ends December 31. The trial balance on January 1, 2018, follows (the amounts are rounded to thousands of dollars to simplify): Account Titles Cash Debit Credit $ 2 6 13 0 51 $ 5 24 4 4 0 0 Accounts Receivable Supplies Land Equipment Accumulated Depreciation Software Accumulated Amortization Accounts Payable Notes Payable (short-term) Salaries and Wages Payable Interest Payable Income Tax Payable Common Stock Retained Earnings Service Revenue Salaries and Wages Expense Depreciation Exper Amortization Expense Income Tax Expense Interest Expense Supplies Expense Totals 0 74 9 0 0 0 0 0 0 0 $96 $96 Transactions and events during 2018 (summarized in thousands of dollars) follow: Transactions and events during 2018 (summarized in thousands of dollars) follow: a. Borrowed $11 cash on March 1 using a short-term note. b. Purchased land on March 2 for future building site; paid cash, $8. C. Issued additional shares of common stock on April 3 for $33. d. Purchased software on July 4, $11 cash. e. Purchased supplies on account on October 5 for future use, $19. f. Paid accounts payable on November 6, $12. g. Signed a $20 service contract on November 7 to start February 1, 2019. h. Recorded revenues of $142 on December 8, including $31 on credit and $111 collected in cash. i. Recognized salaries and wages expense on December 9, $76 paid in cash. j. Collected accounts receivable on December 10, $15. Data for adjusting journal entries as of December 31: k. Unrecorded amortization for the year on software, $4. 1. Supplies counted on December 31, 2018, $12. m. Depreciation for the year on the equipment, $5. n. Interest of $1 to accrue on notes payable. o. Salaries and wages earned but not yet paid or recorded, $11. p. Income tax for the year was $7. It will be paid in 2019. 4. Record the adjusting journal entries (k) through (p). (If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field. Enter your answers in thousands of dollars.) :X 1 Record the unrecorded amortization for the year on software, $4. 2 Record the adjusting entry for supplies counted on December 31, 2018 for $12. 3 Record the adjusting entry for depreciation for the year on the equipment, $5. 4 Record the adjusting entry for accrued interest for $1 on notes payable. 5 Record the adjusting entry for salaries and wages earned but not paid for $11. 6 Record the adjusting entry for income tax for the year was $7. It will be paid in 2019