Question: REQUIRED: - To/From/Date/Subject - Overview/Introduction of the case (short description of the business, environment, general case facts, etc.) - Problem Statement/Root Issue (a clear and

REQUIRED: - To/From/Date/Subject - Overview/Introduction of the case (short description of the business, environment, general case facts, etc.) - Problem Statement/Root Issue (a clear and concise statement directed at what specific problem(s) will be addressed) - Analysis (either one fulsome analysis if there is only one main issue, or an analysis with alternatives for each issue) - Conclusion on each issue (provide a clear conclusion for each applicable point of analysis, alternative, etc.) - Overall Recommendation (from the above analysis and conclusions, add general recommendations to provide to the recipient/audience from the case analysis) - Next Steps/Implementation Plan (providing a few points on next steps, i.e., short term, mid term, long term, or 3-6-12 month plan or suggested steps to move conclusion and recommendations forward)

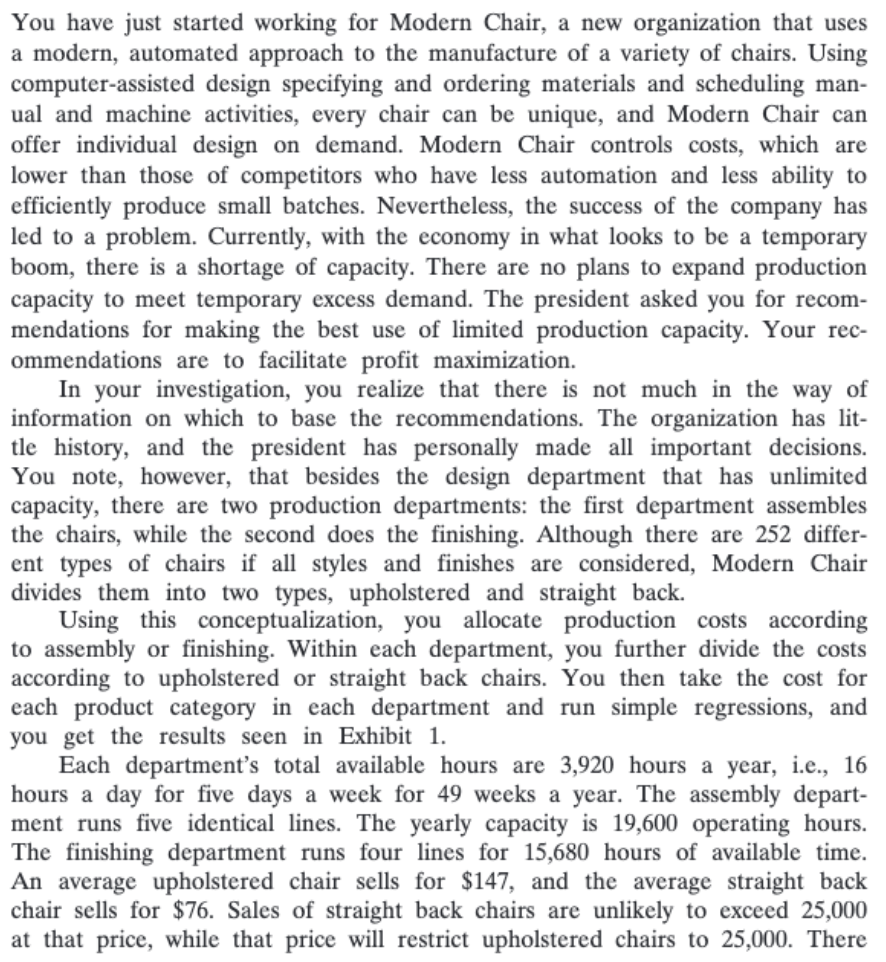

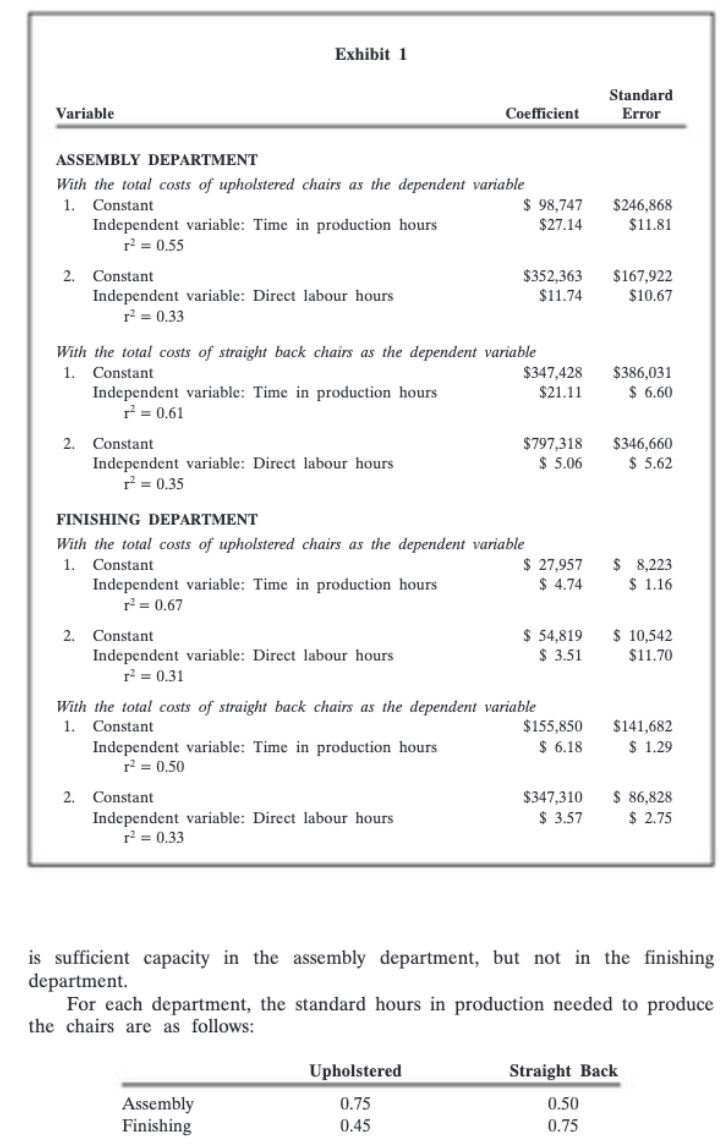

You have just started working for Modern Chair, a new organization that uses a modern, automated approach to the manufacture of a variety of chairs. Using computer-assisted design specifying and ordering materials and scheduling man- ual and machine activities, every chair can be unique, and Modern Chair can offer individual design on demand. Modern Chair controls costs, which are lower than those of competitors who have less automation and less ability to efficiently produce small batches. Nevertheless, the success of the company has led to a problem. Currently, with the economy in what looks to be a temporary boom, there is a shortage of capacity. There are no plans to expand production capacity to meet temporary excess demand. The president asked you for recom- mendations for making the best use of limited production capacity. Your rec- ommendations are to facilitate profit maximization. In your investigation, you realize that there is not much in the way of information on which to base the recommendations. The organization has lit- tle history, and the president has personally made all important decisions. You note, however, that besides the design department that has unlimited capacity, there are two production departments: the first department assembles the chairs, while the second does the finishing. Although there are 252 differ- ent types of chairs if all styles and finishes are considered, Modern Chair divides them into two types, upholstered and straight back. Using this conceptualization, you allocate production costs according to assembly or finishing. Within each department, you further divide the costs according to upholstered or straight back chairs. You then take the cost for each product category in each department and run simple regressions, and you get the results seen in Exhibit 1. Each department's total available hours are 3,920 hours a year, i.e., 16 hours a day for five days a week for 49 weeks a year. The assembly depart- ment runs five identical lines. The yearly capacity is 19,600 operating hours. The finishing department runs four lines for 15,680 hours of available time. An average upholstered chair sells for $147, and the average straight back chair sells for $76. Sales of straight back chairs are unlikely to exceed 25,000 at that price, while that price will restrict upholstered chairs to 25,000. There Exhibit 1 Standard Error Variable Coefficient ASSEMBLY DEPARTMENT With the total costs of upholstered chairs as the dependent variable 1. Constant $ 98,747 Independent variable: Time in production hours $27.14 r2 = 0.55 $246,868 $11.81 2. Constant Independent variable: Direct labour hours r2 = 0.33 $352,363 $11.74 $167,922 $10.67 With the total costs of straight back chairs as the dependent variable 1. Constant $347,428 Independent variable: Time in production hours $21.11 r2 = 0.61 $386,031 $ 6.60 2. Constant Independent variable: Direct labour hours r = 0.35 $797,318 $ 5.06 $346,660 $ 5.62 FINISHING DEPARTMENT With the total costs of upholstered chairs as the dependent variable 1. Constant $ 27,957 Independent variable: Time in production hours $ 4.74 r2 = 0.67 $ 8,223 $ 1.16 2. Constant Independent variable: Direct labour hours r2 = 0.31 $ 54,819 $ 3.51 $ 10,542 $11.70 $141,682 $ 1.29 With the total costs of straight back chairs as the dependent variable 1. Constant $155,850 Independent variable: Time in production hours $ 6.18 r2 = 0.50 2. Constant $347,310 Independent variable: Direct labour hours $ 3.57 r2 = 0.33 $ 86,828 $ 2.75 is sufficient capacity in the assembly department, but not in the finishing department For each department, the standard hours in production needed to produce the chairs are as follows: Upholstered Straight Back Assembly Finishing 0.75 0.45 0.50 0.75 Modern Chair occupied its current facilities four years ago. The assembly department cost $927,000 for plant and equipment. The finishing department's plant and equipment cost $554,000. About 80 percent was for equipment, while the remaining 20 percent was for the land and buildings. Since then, the capac- ities of the two departments have increased about five or six percent a year. The managers and employees found ways to increase efficiency and effective- ness. In examining the non-manufacturing costs, you find that they are all fixed except the five percent sales commission paid on the sales price of each chair. You have just started working for Modern Chair, a new organization that uses a modern, automated approach to the manufacture of a variety of chairs. Using computer-assisted design specifying and ordering materials and scheduling man- ual and machine activities, every chair can be unique, and Modern Chair can offer individual design on demand. Modern Chair controls costs, which are lower than those of competitors who have less automation and less ability to efficiently produce small batches. Nevertheless, the success of the company has led to a problem. Currently, with the economy in what looks to be a temporary boom, there is a shortage of capacity. There are no plans to expand production capacity to meet temporary excess demand. The president asked you for recom- mendations for making the best use of limited production capacity. Your rec- ommendations are to facilitate profit maximization. In your investigation, you realize that there is not much in the way of information on which to base the recommendations. The organization has lit- tle history, and the president has personally made all important decisions. You note, however, that besides the design department that has unlimited capacity, there are two production departments: the first department assembles the chairs, while the second does the finishing. Although there are 252 differ- ent types of chairs if all styles and finishes are considered, Modern Chair divides them into two types, upholstered and straight back. Using this conceptualization, you allocate production costs according to assembly or finishing. Within each department, you further divide the costs according to upholstered or straight back chairs. You then take the cost for each product category in each department and run simple regressions, and you get the results seen in Exhibit 1. Each department's total available hours are 3,920 hours a year, i.e., 16 hours a day for five days a week for 49 weeks a year. The assembly depart- ment runs five identical lines. The yearly capacity is 19,600 operating hours. The finishing department runs four lines for 15,680 hours of available time. An average upholstered chair sells for $147, and the average straight back chair sells for $76. Sales of straight back chairs are unlikely to exceed 25,000 at that price, while that price will restrict upholstered chairs to 25,000. There Exhibit 1 Standard Error Variable Coefficient ASSEMBLY DEPARTMENT With the total costs of upholstered chairs as the dependent variable 1. Constant $ 98,747 Independent variable: Time in production hours $27.14 r2 = 0.55 $246,868 $11.81 2. Constant Independent variable: Direct labour hours r2 = 0.33 $352,363 $11.74 $167,922 $10.67 With the total costs of straight back chairs as the dependent variable 1. Constant $347,428 Independent variable: Time in production hours $21.11 r2 = 0.61 $386,031 $ 6.60 2. Constant Independent variable: Direct labour hours r = 0.35 $797,318 $ 5.06 $346,660 $ 5.62 FINISHING DEPARTMENT With the total costs of upholstered chairs as the dependent variable 1. Constant $ 27,957 Independent variable: Time in production hours $ 4.74 r2 = 0.67 $ 8,223 $ 1.16 2. Constant Independent variable: Direct labour hours r2 = 0.31 $ 54,819 $ 3.51 $ 10,542 $11.70 $141,682 $ 1.29 With the total costs of straight back chairs as the dependent variable 1. Constant $155,850 Independent variable: Time in production hours $ 6.18 r2 = 0.50 2. Constant $347,310 Independent variable: Direct labour hours $ 3.57 r2 = 0.33 $ 86,828 $ 2.75 is sufficient capacity in the assembly department, but not in the finishing department For each department, the standard hours in production needed to produce the chairs are as follows: Upholstered Straight Back Assembly Finishing 0.75 0.45 0.50 0.75 Modern Chair occupied its current facilities four years ago. The assembly department cost $927,000 for plant and equipment. The finishing department's plant and equipment cost $554,000. About 80 percent was for equipment, while the remaining 20 percent was for the land and buildings. Since then, the capac- ities of the two departments have increased about five or six percent a year. The managers and employees found ways to increase efficiency and effective- ness. In examining the non-manufacturing costs, you find that they are all fixed except the five percent sales commission paid on the sales price of each chair

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts