Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Required: Whats the value of the swap to the bank today? Please calculate the value of the swap to the bank in terms of forward

Required: Whats the value of the swap to the bank today? Please calculate the value of the swap to the bank in terms of forward contracts.

Required: Whats the value of the swap to the bank today? Please calculate the value of the swap to the bank in terms of forward contracts.

Hint: You may use the following tables to guide your calculations.

| Time | cash flow () | cash flow ($) | forward exch rate | cash flow in $ | net cash flow $ | pv factor | pv ($) |

| total |

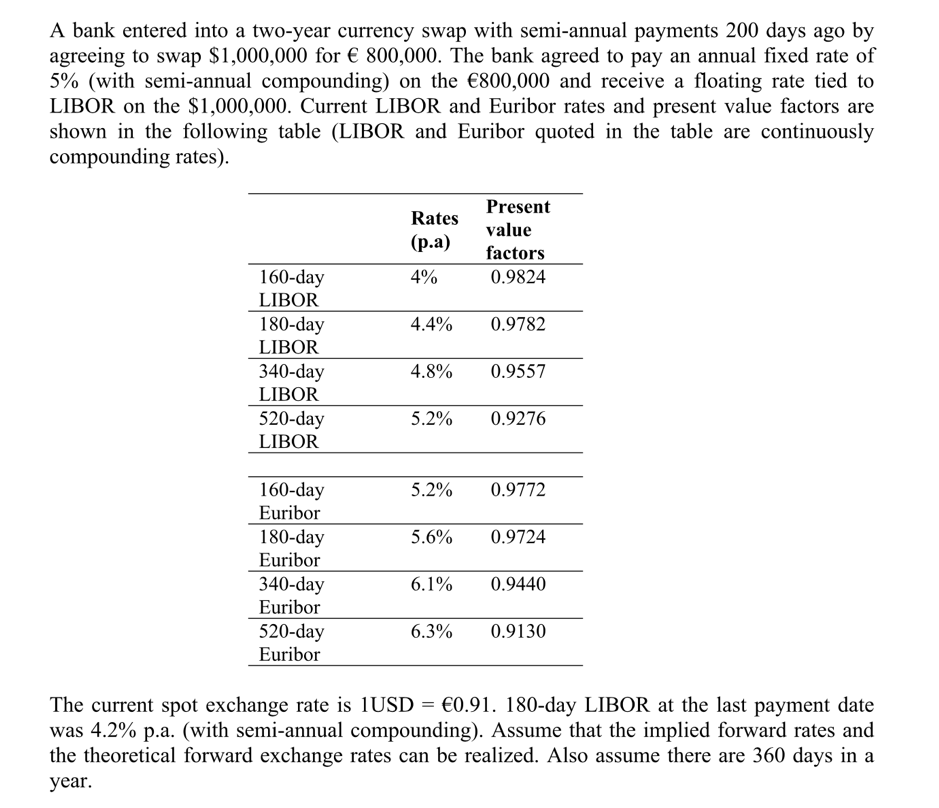

A bank entered into a two-year currency swap with semi-annual payments 200 days ago by agreeing to swap $1,000,000 for 800,000. The bank agreed to pay an annual fixed rate of 5% (with semi-annual compounding) on the 800,000 and receive a floating rate tied to LIBOR on the $1,000,000. Current LIBOR and Euribor rates and present value factors are shown in the following table (LIBOR and Euribor quoted in the table are continuously compounding rates) Present Rates value (.) factors 160-day 4% 0.9824 LIBOR 180-day 4.4% 0.9782 LIBOR 340-day 4.8% 0.9557 LIBOR 520-day 5.2% 0.9276 LIBOR 5.2% 160-day Euribor 0.9772 180-day Euribor 340-day Euribor 5.6% 0.9724 6.1% 0.9440 520-day 6.3% 0.9130 Euribor The current spot exchange rate is 1USD 0.91. 180-day LIBOR at the last payment date was 4.2% p.a. (with semi-annual compounding). Assume that the implied forward rates and the theoretical forward exchange rates can be realized. Also assume there are 360 days in a year A bank entered into a two-year currency swap with semi-annual payments 200 days ago by agreeing to swap $1,000,000 for 800,000. The bank agreed to pay an annual fixed rate of 5% (with semi-annual compounding) on the 800,000 and receive a floating rate tied to LIBOR on the $1,000,000. Current LIBOR and Euribor rates and present value factors are shown in the following table (LIBOR and Euribor quoted in the table are continuously compounding rates) Present Rates value (.) factors 160-day 4% 0.9824 LIBOR 180-day 4.4% 0.9782 LIBOR 340-day 4.8% 0.9557 LIBOR 520-day 5.2% 0.9276 LIBOR 5.2% 160-day Euribor 0.9772 180-day Euribor 340-day Euribor 5.6% 0.9724 6.1% 0.9440 520-day 6.3% 0.9130 Euribor The current spot exchange rate is 1USD 0.91. 180-day LIBOR at the last payment date was 4.2% p.a. (with semi-annual compounding). Assume that the implied forward rates and the theoretical forward exchange rates can be realized. Also assume there are 360 days in a year

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Ultimate Beginners Guide To Understanding NFTs

Authors: LM Anderson

1st Edition

1739781732, 978-1739781736