Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Requirement 5-8 Page 1 PRACTICE SET ACCOUNTING 3341 (5133) SPRING 2019 This practice set is intended to refresh your basic accounting skills by requiring you

Requirement 5-8

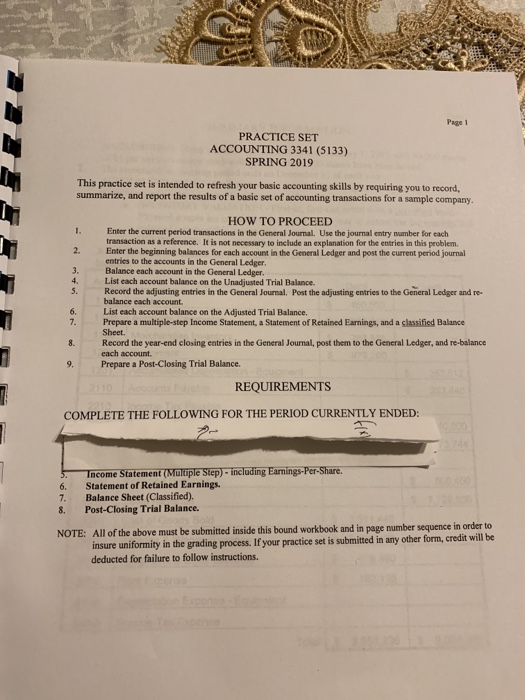

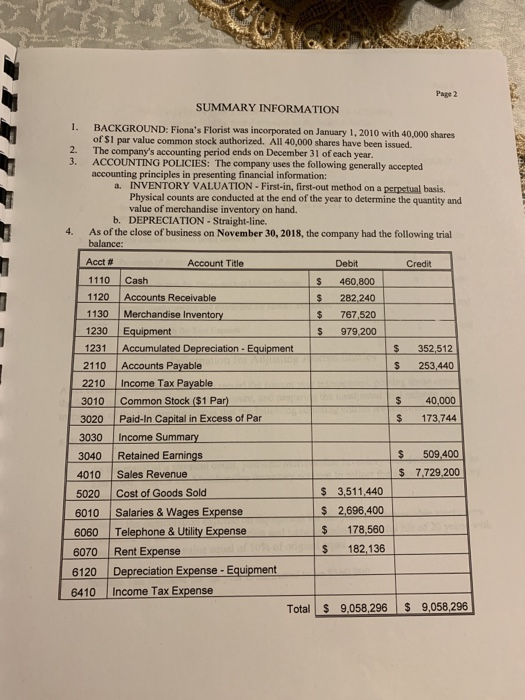

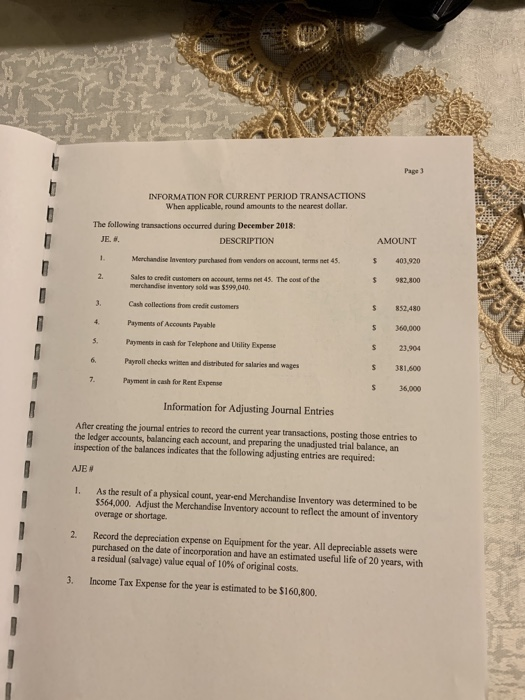

Page 1 PRACTICE SET ACCOUNTING 3341 (5133) SPRING 2019 This practice set is intended to refresh your basic accounting skills by requiring you to record, summarize, and report the results of a basic set of accounting transactions for a sample company. HOW TO PROCEED Enter the current period transactions in the General Journal. Use the journal entry number for each transaction as a reference. It is not necessary to include an explanation for the entries in this problem Enter the beginning balances for each account in the General Ledger and post the current period journal entries to the accounts in the General Ledger Balance each account in the General Ledger List each account balance on the Unadjusted Trial Balance. 2. 4. 5. Record the adjusting entries in the General Journal. Post the adjusting entries to the General Ledger and re balance each account List each account balance on the Adjusted Trial Balance. Prepare a multiple-step Income Statement, a Statement of Retained Earnings, and a classified Balance Sheet Record the year-end closing entries in the General Journal, post them to the General Ledger, and re-balance each account. 6. 8. 9. Prepare a Post-Closing Trial Balance. REQUIREMENTS COMPLETE THE FOLLOWING FOR THE PERIOD CURRENTLY ENDED: Income Statement (Multiple Step)-including Earnings-Per-Share 6. Statement of Retained Earnings. 7. Balance Sheet (Classified) 8. Post-Closing Trial Balance. All of the above must be submitted inside this bound workbook and in page number sequence in order to insure uniformity in the grading process. If your practice set is submitted in any other deducted for failure to follow instructions. NOTE: form, credit will be Page 2 SUMMARY INFORMATION Fiona's Florist was incorporated on January 1, 2010 with 40,000 shares of $1 par value common stock authorized. All 40,000 shares have been issued The company's accounting period ends on December 31 of each year. ACCOUNTING POLICIES: The company uses the following generally accepted accounting principles in presenting financial information: 2. 3. . INVENTORY VALUATION- First-in, first-out method on a perpetual basis. Physical counts are conducted at the end of the year to determine the quantity and value of merchandise inventory on hand. b. DEPRECIATION - Straight-line. 4. As of the close of business on November 30, 2018, the company had the following trial balance: Acct # Account Title Debit S 460,800 $ 282,240 $ 767,520 S 979,200 Credit 1110 Cash 1120 Accounts Receivable 1130 Merchandise Inventory 1230 Equipment 1231 Accumulated Depreciation- Equipment 2110 Accounts Payable 2210 Income Tax Payable 3010 Common Stock ($1 Par) 3020 Paid-In Capital in Excess of Par 3030 Income Summary 3040 Retained Earnings 4010 Sales Revenue 5020 Cost of Goods Sold S 352,512 S 253,440 $ 40,000 S 173,744 $ 509,400 $ 7,729,200 $ 3,511,440 2696,400 $ 178,560 182,136 6010 Salaries & Wages Expense 6060 Telephone &Utility Expense 6070 Rent Expense 6120 Depreciation Expense -Equipment 6410 Income Tax Expense Total 9,058,296 $ 9,058,296 Page 3 INFORMATION FOR CURRENT PERIOD TRANSACTIONS When applicable, round amounts to the nearest dollar The following transactions occurred during December 2018: AMOUNT JE. #. DESCRIPTION 403,920 S 982,800 $ 852,480 S 360,000 s 23,904 s 381,600 s 36,000 Merchandise laventory parchased from vendors on account, terms net 4s Sales so credit customers on account, terms net 45. The cont of the merchandise investory sold was 5399,040 Cash collections from credit customers 4. Payments of Accounts Payable S. Pyments in cash for Telephone and Ulility Expense Payroll checks written and disributed for salaries und wages Payment in cash for Rent Expense Information for Adjusting Journal Entries After creating the journal entries to record the current year transactions, posting those entries to the ledger accounts, balancing each account, and preparing the unadjusted trial balance, an inspection of the balances indicates that the following adjusting entries are required As the result of a physical count, year-end Merchandise Inventory was determined to be $564,000. Adjust the Merchandise Inventory account to reflect the amount of inventory overage or shortage. I. 2. Record the depreciation expense on Equipment for the year. All depreciable assets were purchased on the date of incorporation and have an estimated useful life of 20 years, with a residual (salvage) value equal of 10% of original costs. 3. Income Tax Expense for the year is estimated to be $160,800

Page 1 PRACTICE SET ACCOUNTING 3341 (5133) SPRING 2019 This practice set is intended to refresh your basic accounting skills by requiring you to record, summarize, and report the results of a basic set of accounting transactions for a sample company. HOW TO PROCEED Enter the current period transactions in the General Journal. Use the journal entry number for each transaction as a reference. It is not necessary to include an explanation for the entries in this problem Enter the beginning balances for each account in the General Ledger and post the current period journal entries to the accounts in the General Ledger Balance each account in the General Ledger List each account balance on the Unadjusted Trial Balance. 2. 4. 5. Record the adjusting entries in the General Journal. Post the adjusting entries to the General Ledger and re balance each account List each account balance on the Adjusted Trial Balance. Prepare a multiple-step Income Statement, a Statement of Retained Earnings, and a classified Balance Sheet Record the year-end closing entries in the General Journal, post them to the General Ledger, and re-balance each account. 6. 8. 9. Prepare a Post-Closing Trial Balance. REQUIREMENTS COMPLETE THE FOLLOWING FOR THE PERIOD CURRENTLY ENDED: Income Statement (Multiple Step)-including Earnings-Per-Share 6. Statement of Retained Earnings. 7. Balance Sheet (Classified) 8. Post-Closing Trial Balance. All of the above must be submitted inside this bound workbook and in page number sequence in order to insure uniformity in the grading process. If your practice set is submitted in any other deducted for failure to follow instructions. NOTE: form, credit will be Page 2 SUMMARY INFORMATION Fiona's Florist was incorporated on January 1, 2010 with 40,000 shares of $1 par value common stock authorized. All 40,000 shares have been issued The company's accounting period ends on December 31 of each year. ACCOUNTING POLICIES: The company uses the following generally accepted accounting principles in presenting financial information: 2. 3. . INVENTORY VALUATION- First-in, first-out method on a perpetual basis. Physical counts are conducted at the end of the year to determine the quantity and value of merchandise inventory on hand. b. DEPRECIATION - Straight-line. 4. As of the close of business on November 30, 2018, the company had the following trial balance: Acct # Account Title Debit S 460,800 $ 282,240 $ 767,520 S 979,200 Credit 1110 Cash 1120 Accounts Receivable 1130 Merchandise Inventory 1230 Equipment 1231 Accumulated Depreciation- Equipment 2110 Accounts Payable 2210 Income Tax Payable 3010 Common Stock ($1 Par) 3020 Paid-In Capital in Excess of Par 3030 Income Summary 3040 Retained Earnings 4010 Sales Revenue 5020 Cost of Goods Sold S 352,512 S 253,440 $ 40,000 S 173,744 $ 509,400 $ 7,729,200 $ 3,511,440 2696,400 $ 178,560 182,136 6010 Salaries & Wages Expense 6060 Telephone &Utility Expense 6070 Rent Expense 6120 Depreciation Expense -Equipment 6410 Income Tax Expense Total 9,058,296 $ 9,058,296 Page 3 INFORMATION FOR CURRENT PERIOD TRANSACTIONS When applicable, round amounts to the nearest dollar The following transactions occurred during December 2018: AMOUNT JE. #. DESCRIPTION 403,920 S 982,800 $ 852,480 S 360,000 s 23,904 s 381,600 s 36,000 Merchandise laventory parchased from vendors on account, terms net 4s Sales so credit customers on account, terms net 45. The cont of the merchandise investory sold was 5399,040 Cash collections from credit customers 4. Payments of Accounts Payable S. Pyments in cash for Telephone and Ulility Expense Payroll checks written and disributed for salaries und wages Payment in cash for Rent Expense Information for Adjusting Journal Entries After creating the journal entries to record the current year transactions, posting those entries to the ledger accounts, balancing each account, and preparing the unadjusted trial balance, an inspection of the balances indicates that the following adjusting entries are required As the result of a physical count, year-end Merchandise Inventory was determined to be $564,000. Adjust the Merchandise Inventory account to reflect the amount of inventory overage or shortage. I. 2. Record the depreciation expense on Equipment for the year. All depreciable assets were purchased on the date of incorporation and have an estimated useful life of 20 years, with a residual (salvage) value equal of 10% of original costs. 3. Income Tax Expense for the year is estimated to be $160,800

Requirement 5-8

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access with AI-Powered Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting concepts and applications

Authors: Albrecht Stice, Stice Swain

11th Edition

978-0538750196, 538745487, 538750197, 978-0538745482