Requirement A

requierment b consolidation

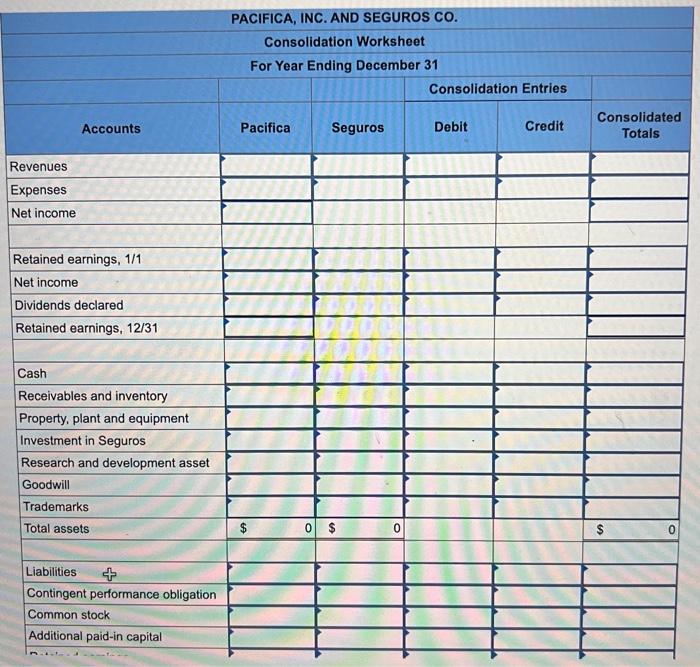

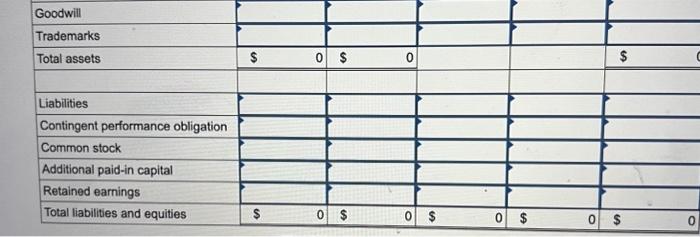

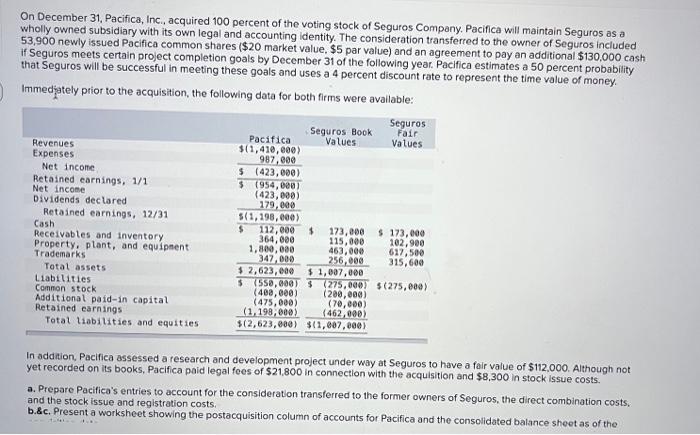

On December 31, Pacifica, Inc., acquired 100 percent of the voting stock of Seguros Company. Pacifica will maintain Seguros as a wholly owned subsidiary with its own legal and accounting identity. The consideration transferred to the owner of Seguros included 53,900 newly issued Pacifica common shares ( $20 market value, $5 par value) and an agreement to pay an additional $130,000 cash if Seguros meets certain project completion goals by December 31 of the following year. Pacifica estimates a 50 percent probability that Seguros will be successful in meeting these goals and uses a 4 percent discount rate to represent the time value of money. Immediately prior to the acquisition, the following data for both firms were avallable: In addition, Pacifica assessed a research and development project under way at Seguros to have a fair value of $112,000. Although not yet recorded on its books, Pacifica paid legal fees of $21,800 in connection with the acquisition and $8,300 in stock issue costs. a. Prepare Pacifica's entries to account for the consideration transferred to the former owners of Seguros, the direct combination costs, and the stock issue and registration costs. b.8c. Present a worksheet showing the postacquisition column of accounts for Pacifica and the consolidated balance sheet as of the Complete this question by entering your answers in the tabs below. Prepare Pacifica's entries to account for the consideration transferred to the former owners of Seguros, the direct combination costs, and the stock issue and registration costs. (Use a 0.961538 present value factor where applicable. If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) Journal entry worksheet Journal entry worksheet Record the acquisition of Seguros Company. Note: Enter debits before credits. Journal entry worksheet Record the legal fees related to the combination. Note: Enter debits before credits. Journal entry worksheet Record the payment of stock issuance costs. Note: Enter debits before credits. PACIFICA, INC. AND SEGUROS CO. Consolidation Worksheet For Year Ending December 31 \begin{tabular}{|c|c|c|c|c|c|c|c|} \hline \multicolumn{8}{|l|}{ Goodwill } \\ \hline \multicolumn{8}{|l|}{ Trademarks } \\ \hline Total assets & $ & 0 & $ & 0 & & & $ \\ \hline \multicolumn{8}{|l|}{ Liabilities } \\ \hline \multicolumn{8}{|c|}{ Contingent performance obligation } \\ \hline \multicolumn{8}{|l|}{ Common stock } \\ \hline \multicolumn{8}{|l|}{ Additional paid-in capital } \\ \hline \multicolumn{8}{|l|}{ Retained earnings } \\ \hline Total liabilities and equities & $ & 0 & $ & 0 & $ & $ & $ \\ \hline \end{tabular} On December 31, Pacifica, Inc., acquired 100 percent of the voting stock of Seguros Company. Pacifica will maintain Seguros as a wholly owned subsidiary with its own legal and accounting identity. The consideration transferred to the owner of Seguros included 53,900 newly issued Pacifica common shares ( $20 market value, $5 par value) and an agreement to pay an additional $130,000 cash if Seguros meets certain project completion goals by December 31 of the following year. Pacifica estimates a 50 percent probability that Seguros will be successful in meeting these goals and uses a 4 percent discount rate to represent the time value of money. Immediately prior to the acquisition, the following data for both firms were avallable: In addition, Pacifica assessed a research and development project under way at Seguros to have a fair value of $112,000. Although not yet recorded on its books, Pacifica paid legal fees of $21,800 in connection with the acquisition and $8,300 in stock issue costs. a. Prepare Pacifica's entries to account for the consideration transferred to the former owners of Seguros, the direct combination costs, and the stock issue and registration costs. b.8c. Present a worksheet showing the postacquisition column of accounts for Pacifica and the consolidated balance sheet as of the Complete this question by entering your answers in the tabs below. Prepare Pacifica's entries to account for the consideration transferred to the former owners of Seguros, the direct combination costs, and the stock issue and registration costs. (Use a 0.961538 present value factor where applicable. If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) Journal entry worksheet Journal entry worksheet Record the acquisition of Seguros Company. Note: Enter debits before credits. Journal entry worksheet Record the legal fees related to the combination. Note: Enter debits before credits. Journal entry worksheet Record the payment of stock issuance costs. Note: Enter debits before credits. PACIFICA, INC. AND SEGUROS CO. Consolidation Worksheet For Year Ending December 31 \begin{tabular}{|c|c|c|c|c|c|c|c|} \hline \multicolumn{8}{|l|}{ Goodwill } \\ \hline \multicolumn{8}{|l|}{ Trademarks } \\ \hline Total assets & $ & 0 & $ & 0 & & & $ \\ \hline \multicolumn{8}{|l|}{ Liabilities } \\ \hline \multicolumn{8}{|c|}{ Contingent performance obligation } \\ \hline \multicolumn{8}{|l|}{ Common stock } \\ \hline \multicolumn{8}{|l|}{ Additional paid-in capital } \\ \hline \multicolumn{8}{|l|}{ Retained earnings } \\ \hline Total liabilities and equities & $ & 0 & $ & 0 & $ & $ & $ \\ \hline \end{tabular}