Answered step by step

Verified Expert Solution

Question

1 Approved Answer

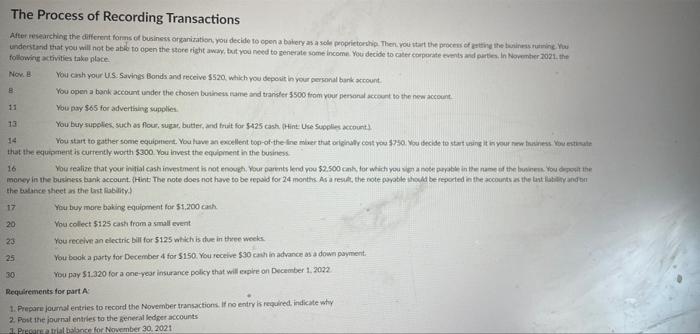

requirement for part A . this is the clearest i can get the picture. The Process of Recording Transactions After researching the different forms of

requirement for part A . this is the clearest i can get the picture.

The Process of Recording Transactions After researching the different forms of business organization, you decide to open a bakery as a sole proprietorship. Then you start the process of getting the business running. You understand that you will not be able to open the store right away, but you need to generate some income. You decide to cater corporate events and parties. In November 2021, the following activities take place. Nov. B 8 You cash your U.S. Savings Bonds and receive $520, which you deposit in your personal bank account. You open a bank account under the chosen business name and transfer $500 from your personal account to the new account. You pay $65 for advertising supplies. 11 13 You buy supplies, such as flour, sugar, butter, and fruit for $425 cash (Hint: Use Supplies account) 14 You start to gather some equipment. You have an excellent top-of-the-line mixer that originally cost you $750. You decide to start using it in your new business. You estimate that the equipment is currently worth $300 You invest the equipment in the business. 16 You realize that your initial cash investment is not enough. Your parents lend you $2.500 cash, for which you sign a note payable in the name of the business. You deposit the money in the business bank account. (Hint: The note does not have to be repaid for 24 months. As a result, the note payable should be reported in the accounts as the last ability and br the balance sheet as the last Rability) 17 20 23 25 30 You buy more baking equipment for $1.200 cash You collect $125 cash from a small event You receive an electric bill for $125 which is due in three weeks You book a party for December 4 for $150. You receive $30 cash in advance as a down payment. You pay $1.320 for a one-year insurance policy that will expire on December 1, 2022 Requirements for part A 1. Prepare journal entries to record the November transactions. If no entry is required, indicate why 2. Post the journal entries to the general ledger accounts 3. Prepare a trial balance for November 30, 2021 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Organizational Change

Authors: Barbara Senior, Stephen Swailes

5th Edition

1292063831, 9781292063836