Answered step by step

Verified Expert Solution

Question

1 Approved Answer

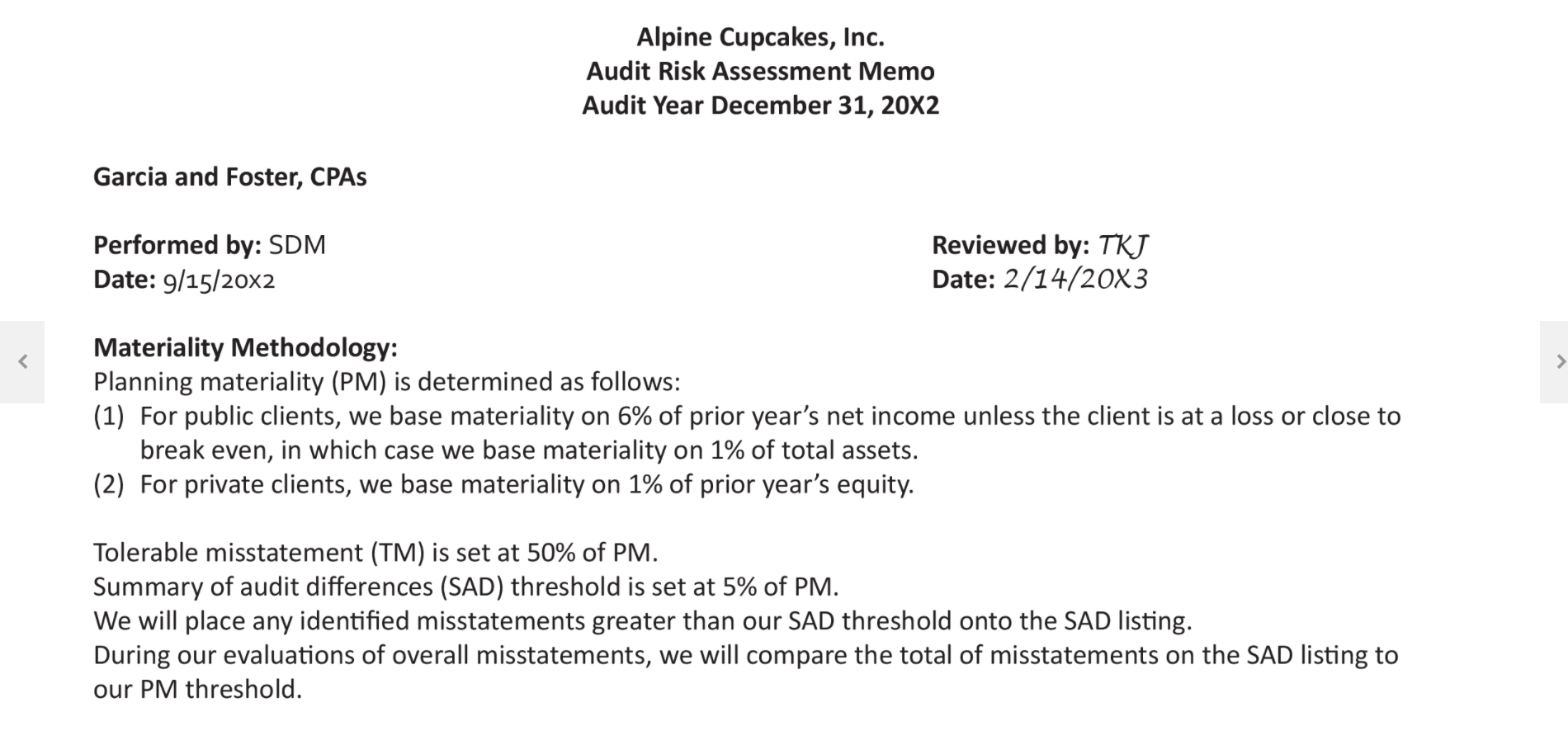

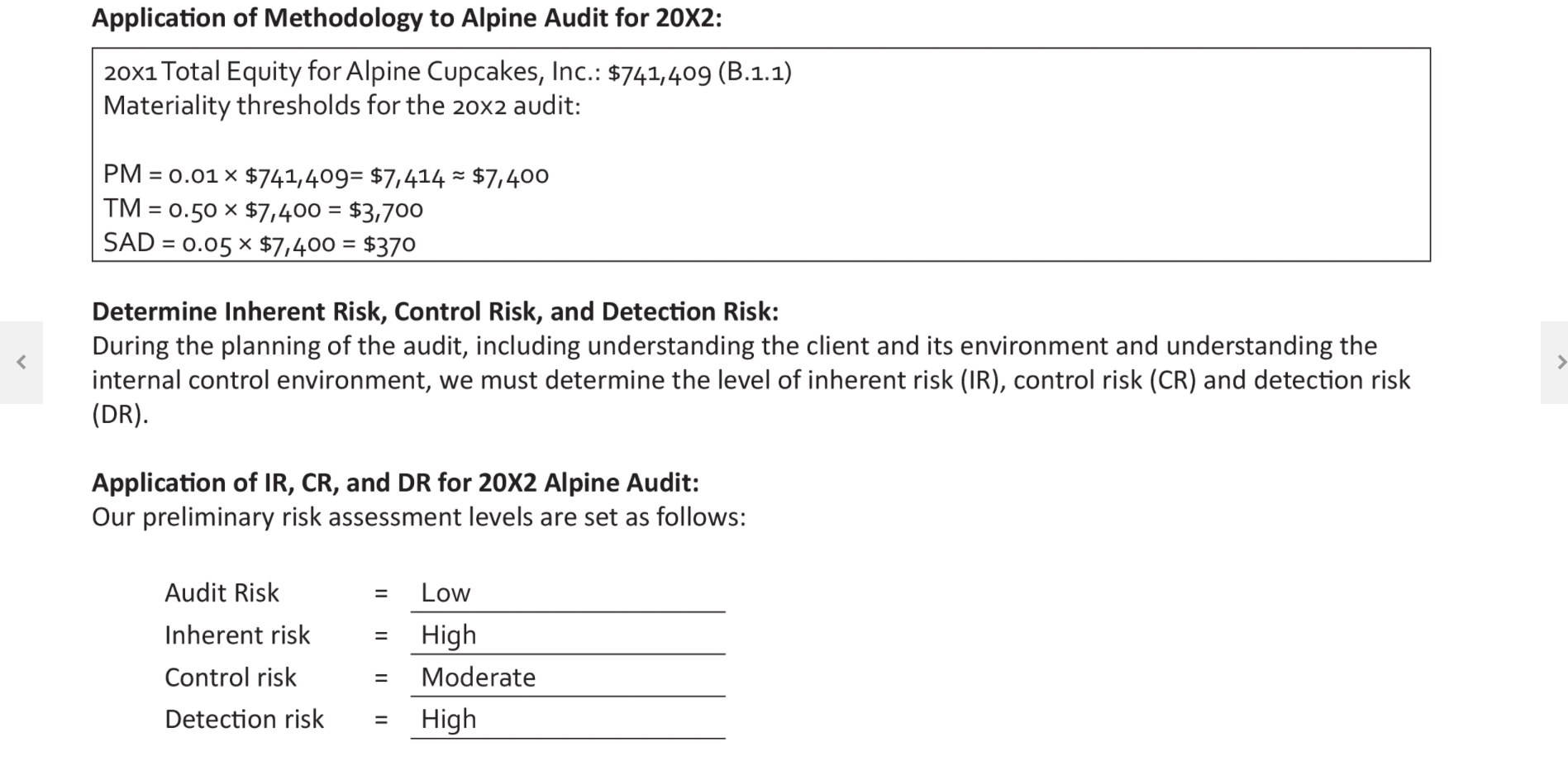

Review the audit risk model assessment and documentation . How should this assessment be altered to correctly reflect the appropriate risk assessment of the firm?

- Review the audit risk model assessment and documentation . How should this assessment be altered to correctly reflect the appropriate risk assessment of the firm? How might the documentation of audit risk be improved?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Energy Audits

Authors: Albert Thumann, Terry Niehus, William J. Younger

7th Edition

1420067915, 978-1420067910