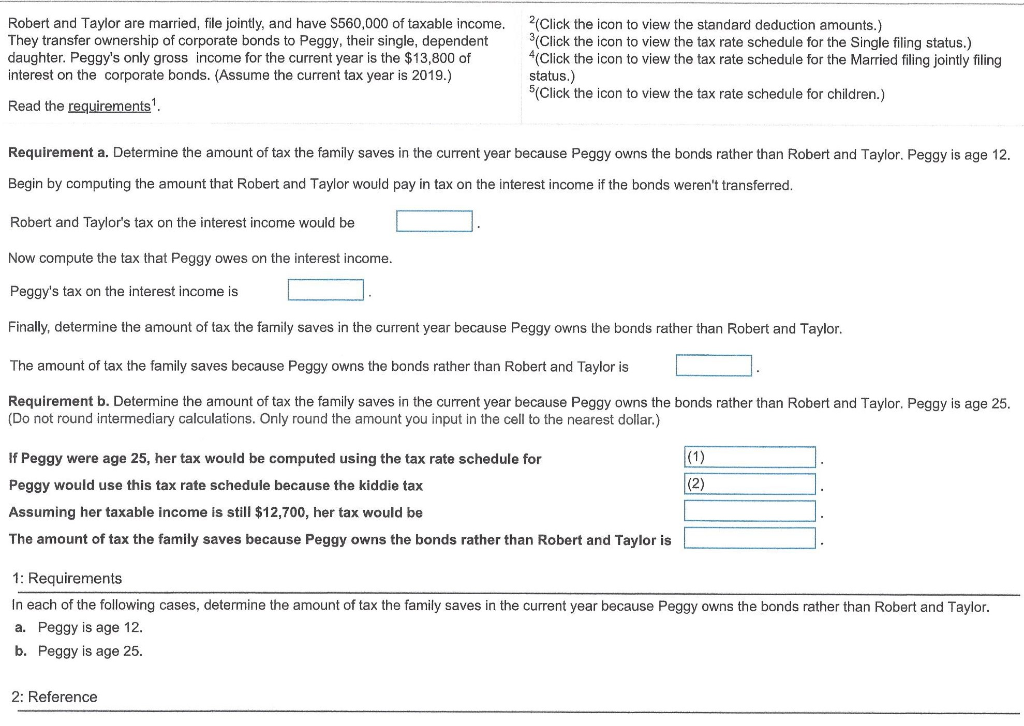

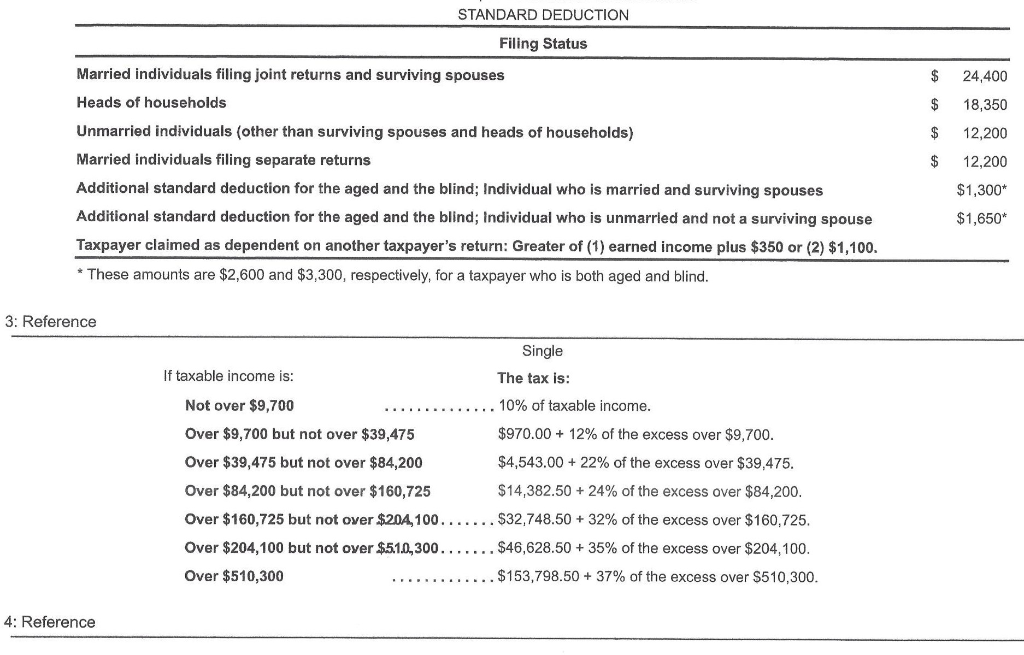

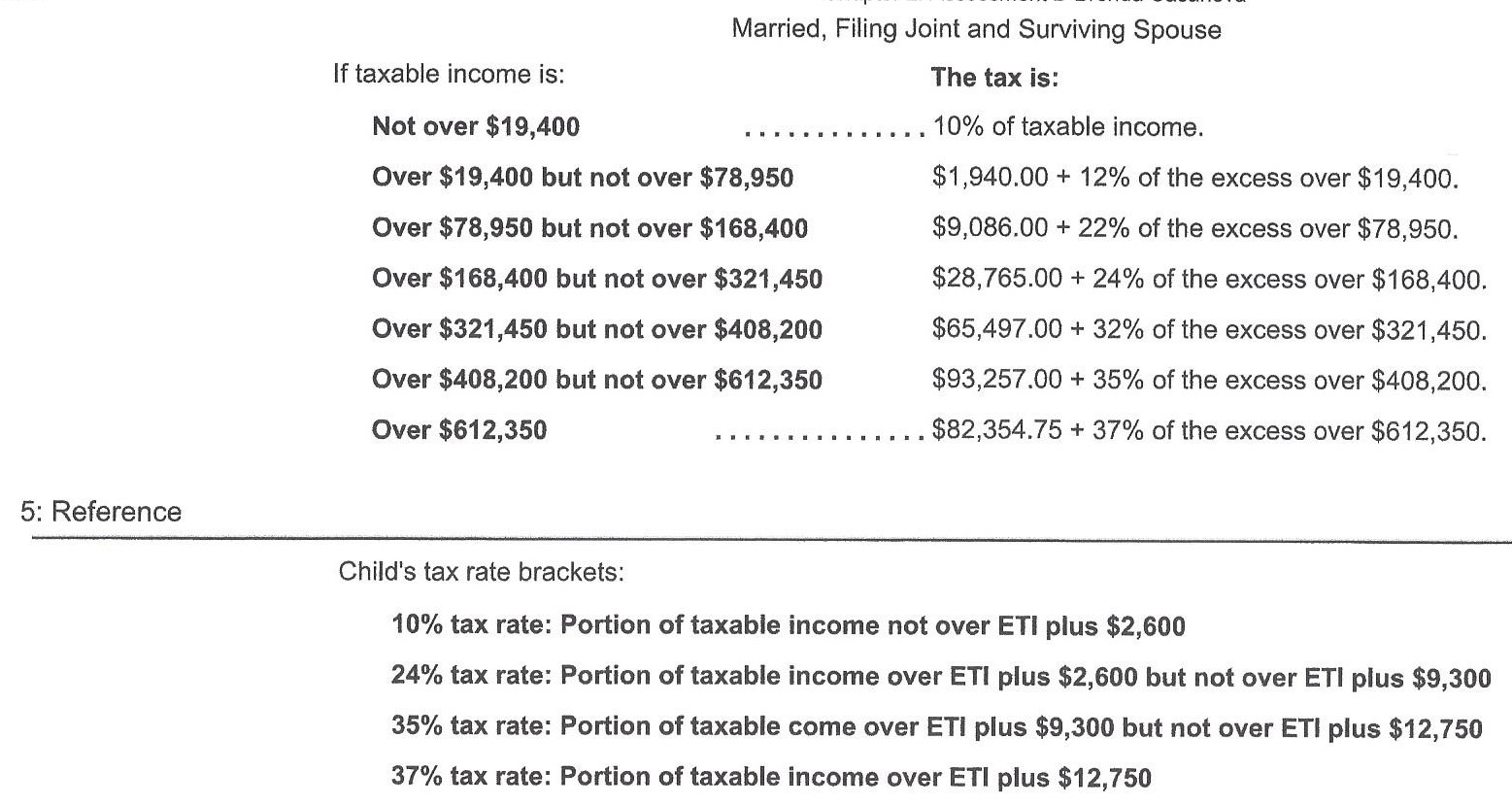

Robert and Taylor are married, file jointly, and have S560,000 of taxable income. They transfer ownership of corporate bonds to Peggy, their single, dependent daughter. Peggy's only gross income for the current year is the $13,800 of interest on the corporate bonds. (Assume the current tax year is 2019.) (Click the icon to view the standard deduction amounts.) (Click the icon to view the tax rate schedule for the Single filing status.) (Click the icon to view the tax rate schedule for the Married filing jointly filing status.) 5(Click the icon to view the tax rate schedule for children.) Read the requirements? Requirement a. Determine the amount of tax the family saves in the current year because Peggy owns the bonds rather than Robert and Taylor. Peggy is age 12. Begin by computing the amount that Robert and Taylor would pay in tax on the interest income if the bonds weren't transferred. Robert and Taylor's tax on the interest income would be Now compute the tax that Peggy owes on the interest income. Peggy's tax on the interest income is Finally, determine the amount of tax the family saves in the current year because Peggy owns the bonds rather than Robert and Taylor. The amount of tax the family saves because Peggy owns the bonds rather than Robert and Taylor is . Requirement b. Determine the amount of tax the family saves in the current year because Peggy owns the bonds rather than Robert and Taylor. Peggy is age 25. (Do not round intermediary calculations. Only round the amount you input in the cell to the nearest dollar) If Peggy were age 25, her tax would be computed using the tax rate schedule for Peggy would use this tax rate schedule because the kiddie tax Assuming her taxable income is still $12,700, her tax would be The amount of tax the family saves because Peggy owns the bonds rather than Robert and Taylor is 1: Requirements In each of the following cases, determine the amount of tax the family saves in the current year because Peggy owns the bonds rather than Robert and Taylor. a. Peggy is age 12. b. Peggy is age 25. 2: Reference STANDARD DEDUCTION Filing Status $ $ Married individuals filing joint returns and surviving spouses Heads of households Unmarried individuals (other than surviving spouses and heads of households) Married individuals filing separate returns Additional standard deduction for the aged and the blind; Individual who is married and surviving spouses Additional standard deduction for the aged and the blind; Individual who is unmarried and not a surviving spouse Taxpayer claimed as dependent on another taxpayer's return: Greater of (1) earned income plus $350 or (2) $1,100. * These amounts are $2,600 and $3,300, respectively, for a taxpayer who is both aged and blind. 24,400 18,350 12,200 12,200 $1,300* $1,650* $ 3: Reference Single If taxable income is: The tax is: Not over $9,700 10% of taxable income. Over $9,700 but not over $39,475 $970.00 + 12% of the excess over $9,700. Over $39,475 but not over $84,200 $4,543.00 + 22% of the excess over $39,475. Over $84,200 but not over $160,725 $14,382.50 + 24% of the excess over $84,200. Over $160,725 but not over $204, 100. ... ... $32,748.50 + 32% of the excess over $160,725. Over $204,100 but not over $51.0,300....... $46,628.50 + 35% of the excess over $204,100. Over $510,300 ....... $153,798.50 + 37% of the excess over $510,300. 4: Reference Married, Filing Joint and Surviving Spouse If taxable income is: The tax is: Not over $19,400 ....... . 10% of taxable income. Over $19,400 but not over $78,950 $1,940.00 + 12% of the excess over $19,400. Over $78,950 but not over $168,400 $9,086.00 + 22% of the excess over $78,950. Over $168,400 but not over $321,450 $28,765.00 + 24% of the excess over $168,400. Over $321,450 but not over $408,200 $65,497.00 + 32% of the excess over $321,450. Over $408,200 but not over $612,350 $93,257.00 + 35% of the excess over $408,200. Over $612,350 $82,354.75 + 37% of the excess over $612,350. 5: Reference Child's tax rate brackets: 10% tax rate: Portion of taxable income not over ETI plus $2,600 24% tax rate: Portion of taxable income over ETI plus $2,600 but not over ETI plus $9,300 35% tax rate: Portion of taxable come over ETI plus $9,300 but not over ETI plus $12,750 37% tax rate: Portion of taxable income over ETI plus $12,750