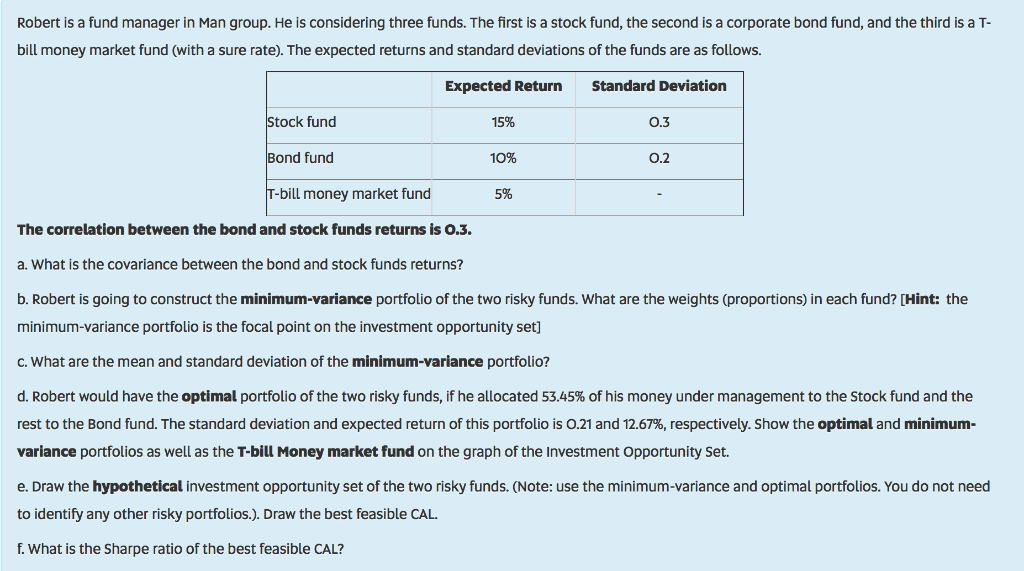

Robert is a fund manager in Man group. He is considering three funds. The first is a stock fund, the second is a corporate bond fund, and the third is a T- bill money market fund (with a sure rate). The expected returns and standard deviations of the funds are as follows. Expected Return Standard Deviation Stock fund 15% 0.3 Bond fund 10% 0.2 T-bill money market fund 5% The correlation between the bond and stock funds returns is 0.3. a. What is the covariance between the bond and stock funds returns? b. Robert is going to construct the minimum-variance portfolio of the two risky funds. What are the weights (proportions) in each fund? [Hint: the minimum-variance portfolio is the focal point on the investment opportunity set] C. What are the mean and standard deviation of the minimum-variance portfolio? d. Robert would have the optimal portfolio of the two risky funds, if he allocated 53.45% of his money under management to the Stock fund and the rest to the Bond fund. The standard deviation and expected return of this portfolio is 0.21 and 12.67%, respectively. Show the optimal and minimum- variance portfolios as well as the T-bill Money market fund on the graph of the Investment Opportunity Set. e. Draw the hypothetical investment opportunity set of the two risky funds. (Note: use the minimum-variance and optimal portfolios. You do not need to identify any other risky portfolios.). Draw the best feasible CAL. f. What is the Sharpe ratio of the best feasible CAL? Robert is a fund manager in Man group. He is considering three funds. The first is a stock fund, the second is a corporate bond fund, and the third is a T- bill money market fund (with a sure rate). The expected returns and standard deviations of the funds are as follows. Expected Return Standard Deviation Stock fund 15% 0.3 Bond fund 10% 0.2 T-bill money market fund 5% The correlation between the bond and stock funds returns is 0.3. a. What is the covariance between the bond and stock funds returns? b. Robert is going to construct the minimum-variance portfolio of the two risky funds. What are the weights (proportions) in each fund? [Hint: the minimum-variance portfolio is the focal point on the investment opportunity set] C. What are the mean and standard deviation of the minimum-variance portfolio? d. Robert would have the optimal portfolio of the two risky funds, if he allocated 53.45% of his money under management to the Stock fund and the rest to the Bond fund. The standard deviation and expected return of this portfolio is 0.21 and 12.67%, respectively. Show the optimal and minimum- variance portfolios as well as the T-bill Money market fund on the graph of the Investment Opportunity Set. e. Draw the hypothetical investment opportunity set of the two risky funds. (Note: use the minimum-variance and optimal portfolios. You do not need to identify any other risky portfolios.). Draw the best feasible CAL. f. What is the Sharpe ratio of the best feasible CAL